stepford

Thinks s/he gets paid by the post

More important than all this financial advice, with a name like mtbikelover what kind of bikes do you have and where do you like to ride?

More important than all this financial advice, with a name like mtbikelover what kind of bikes do you have and where do you like to ride?

When we move to Colorado for retirement, we will go to Moab and hit a lot of the mountain biking out there. I can’t wait!

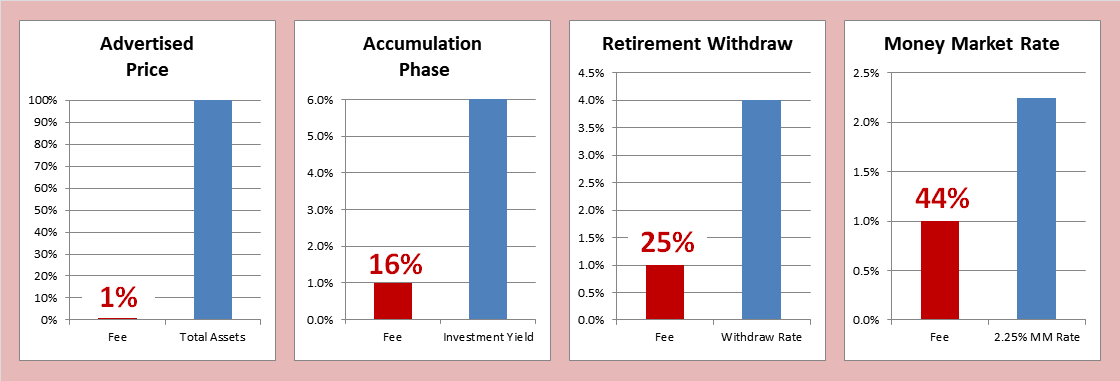

Obviously you have enough, and are comfortable with decisions like this.Well...I’m not that stupid to leave it somewhere it’s losing money. I thought I said in my original post but maybe not - it’s earning 1% AFTER the 1% fee. It’s in a Schwab MM account that pays 2-2.25%.

It's your money. You get to do whatever you choose with it.I feel we should take the $125k and invest it in something like VTI or VFINX. If the market does tank and there are some good buys, we have plenty more cash to use to invest.

Would love to get others opinions.

Haha! I ride an old Gary Fisher. It’s one of those things where I know I can afford a more up to date bike with all the bells and whistles but I love my Gary Fisher so much. It fits me perfectly and I don’t want to change. I’ve upgraded a few parts but kept it pretty much the same.

And since I live in Wisconsin, I just ride some great singletrack trails in the Southern Kettles. When we move to Colorado for retirement, we will go to Moab and hit a lot of the mountain biking out there. I can’t wait!

I’ve used the mtbikelover handle for many years. I first started biking in PA and WV but then work took me to Wisconsin. You are right...not mountains. But they still have some great trails with hills that are tough to climb and fast to go down with rocks, roots, tight turns, etc. So it works for now until we retire."

At 1,951 feet above sea level, Timm's Hill is the highest point in Wisconsin. At this scenic park you can climb the observation tower for a 30-mile view of the vast Northwoods. To the south you'll look down on placid Bass Lake 160 feet below."

A mountain bike lover in a state with no mountains. Oh well. But seriously there are some awesome trails in WI. I grew up in Northern WI on the shores of Lake Superior. Great scenery. Good luck on your journey to CO and ER.

Here's another view. With 69% already in equities, and retirement 4 years away, I'm not sure I would want to have more of my AA devoted to equities, especially with this frothy market. 70% equities and 30% fixed income, seems like a good AA to me. If some of that Fixed Income is currently invested in cash instruments yielding 2-3%, then the debate for me would be when should I transfer some of that cash to longer maturities, and now would not be the time.

")

You made a lot of assumptions. I don’t fret about the market. I simply didn’t like having so much cash uninvested. And he invested it in index funds like I asked.

@mtbikelover, I am not going to join the native drumbeaters trying to convince you to ditch your FA. You have made your position clear on that. I would, however, like to flag a few things that I'd suggest you watch for:

1) The FA seems to think the he/she can successfully pick stocks. This is most charitably characterized as naive. It is also hazardous to your financial health.

2) Is the FA charging you the 1% fee on cash and near cash? This is not defendable; the FA has no way to add a whit of value to these holdings. I am involved with one nonprofit where the FA charges no fee on cash and near-cash. I have heard of others where a discounted fee is charged. If you are paying full price you are being cheated.

3) You say "I have some stocks that are up 40% in the 14 months we have been with him." That's really no surprise. Market prices are so "noisy" that it is relatively easy to come up with some winners. What has been proven to be impossible is to come up with a $$ preponderance of winners by picking stocks. IOW, pay absolutely no attention to individual stocks in the portfolio; watch only the total return of the equity portfolio versus the total return of a broad benchmark like the Russell 3000 or the ACWI (All Country World Index). In fact, I have arranged for the FA I mentioned to report quarterly on the equity portfolio against the ACWI. To say that involved some kicking and screaming is an understatement. What most FAs want you to look at is the overall return of the portfolio. But it is impossible to measure the FA's performance using a composite number.

You're well informed and thoughtful. Just keep your eyes on the big picture and make sure the value you're receiving from this FA is worth the fees, including the likely market underperformance. (Like others here, I am skeptical of this, but none of us have a vote.)

It’s pre-trek. KaiTai. I think it’s 2000 or 2001.What fisher? Pre-trek? I have a 1995 Mt Tam. Super light and great geometry. Love it. XTR v brakes now and some other mods but still the same bike.

Misinformation here. Investing in IPOs is, statistically, a losing strategy. Probably (hopefully?) the OP's FA knows this. And, @kgtest, you should understand that the only IPOs that get offered to small retail investors are ones so stinky that the brokerage house's institutional clients and heavy hitter clients won't take the deal. So if you are not in the latter two categories, you better be careful. Like by keeping your money in your pocket.Oh, what was the FAs plan for cash? You mentioned a sale. Do you ever do IPO? Usually FA's get money by pushing specific products but not always. Pinterest and Zoom IPO tomorrow. I know some people getting in on that action. I'll update you later on how it turned out. They called this gambling, and I agree, I think I might gamble a bit too, but am really waiting for Slack to IPO. It's on my bucket list to buy on an IPO day that I feel will launch.

Agreed. Dont do the IPO. I tried today but wasnt willing to pay more than what other people apparently were. Ive never veen able to actuslly execute a limit order on an IPO day in that regard it is losing. I am really just curious where they decide to out the cash. It seems OP has little risk to just go VTI with the 125k and call it a day. Just buy the entiee market and rise and fall with the other boats jn the sea. That is my final answrr 125k on VTI.Misinformation here. Investing in IPOs is, statistically, a losing strategy. Probably (hopefully?) the OP's FA knows this. And, @kgtest, you should understand that the only IPOs that get offered to small retail investors are ones so stinky that the brokerage house's institutional clients and heavy hitter clients won't take the deal. So if you are not in the latter two categories, you better be careful. Like by keeping your money in your pocket.

FA's getting paid based on AUM are Registered Investment Advisors or Investment Advisor Representatives, IOW fiduciaries and are not paid for pushing products. The only "FAs" that get paid for pushing products are registered representatives who are held to the very weak "suitability" standard and who have no legal obligation to act in the clients' best interests. Unfortunately, anyone with $15 headroom on a credit card can go to VistaPrint and get "Financial Advisor" printed on some business cards.

Just to be clear, an IPO is priced and sold, usually to a favored few. Once it is sold out, then it is just like any other stock on the market. There is a bid price and an asked price and there is trading. The goal of the initial pricing is to hit a number that does not result in the stock going up substantially in the secondary market. This would mean that the underwriter has left money on the table.... I tried today but wasnt willing to pay more than what other people apparently were. Ive never veen able to actuslly execute a limit order on an IPO day in that regard it is losing. ...

Of course. Tiny retail customers like you and me will never be given access to anything decent in the national market. The underwriters will first offer the deals to their institutional and heavy-hitter clients. Only if that group refuses to buy/deems the deal too stinky, will the retail brokers start calling their small clients. Why would you want to write a few hundred tickets if you could write just one and in the process stroke & reward a big client?Roger that. No wonder ive basically stuck to indexing. So...how do I get access to the IPO like Slack. Do you need to be a who's who? ...