|

|

Hi! New and looking for advice on how much cash to hold

04-16-2019, 11:04 AM

04-16-2019, 11:04 AM

|

#1

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

Hi! New and looking for advice on how much cash to hold

I'm 47, husband is 49, and we are planning to retire in a little less than 4 years. We have over $2M saved in investments (mix of roth, traditional IRA, and 401K). We also have about $450k in cash/quick access money. Most of that is earning 2-3% in short term CD's and money market accounts.

We pay a financial advisor to manage our investments and he is keeping $125k in cash - "waiting for something that is a good buy." It's killing me every time I look at the returns YTD and see 0.5% on those accounts and 12-14% on the accounts that are invested. It is in a money market account earning 2% but we pay him 1%.

I feel we should take the $125k and invest it in something like VTI or VFINX. If the market does tank and there are some good buys, we have plenty more cash to use to invest.

Would love to get others opinions.

Thanks!

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

04-16-2019, 11:33 AM

|

#2

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2005

Location: Chicago

Posts: 13,186

|

Quote: Quote:

Originally Posted by mtbikelover

I'm 47, husband is 49, and we are planning to retire in a little less than 4 years. We have over $2M saved in investments (mix of roth, traditional IRA, and 401K). We also have about $450k in cash/quick access money. Most of that is earning 2-3% in short term CD's and money market accounts.

We pay a financial advisor to manage our investments and he is keeping $125k in cash - "waiting for something that is a good buy." It's killing me every time I look at the returns YTD and see 0.5% on those accounts and 12-14% on the accounts that are invested. It is in a money market account earning 2% but we pay him 1%.

I feel we should take the $125k and invest it in something like VTI or VFINX. If the market does tank and there are some good buys, we have plenty more cash to use to invest.

Would love to get others opinions.

Thanks!

|

What is your target AA and how would the purchase of $125k of VTI impact that?

__________________

"I wasn't born blue blood. I was born blue-collar." John Wort Hannam

|

|

|

|

|

04-16-2019, 11:47 AM

|

#3

|

|

Thinks s/he gets paid by the post

Join Date: Jun 2013

Posts: 1,019

|

Quote:

Originally Posted by youbet

What is your target AA and how would the purchase of $125k of VTI impact that?

|

Don't have enough details to answer the question, but IMO if you are informed enough to be asking this question, including proposing that you invest in index funds, you don't need to pay 1% to an advisor. You can be a DIY investor. Also, your desire to index is the opposite of the advisor's desire to time the market.

|

|

|

|

|

04-16-2019, 11:54 AM

|

#4

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

Quote:

Originally Posted by youbet

What is your target AA and how would the purchase of $125k of VTI impact that?

|

With $2.6M total, our AA is:

69% stocks

15% bonds

16% cash

We also have many other non stock investments including rental properties, whole life insurance policies, HSA, and company stock options. My company is private so I classify these stock options as "non stock" because there is no risk to them. It is their version of a pension plan.

My purpose in investing more of the cash is to have more cash when we retire so we don't have to pull much from the retirement accounts and thus stay in a low tax bracket so we can get cheap health insurance. Most of our retirement accounts are taxable as we make too much to do Roth contributions and I was clueless when I was young so didn't realize the benefit of Roth.

|

|

|

|

|

04-16-2019, 11:59 AM

|

#5

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by mtbikelover

... We pay a financial advisor to manage our investments and he is keeping $125k in cash - "waiting for something that is a good buy." ...

|

Ask him this: "If you are able to reliably identify good stock buys, why are you working as an FA?" "In fact, why are you working at all?"

His is a terminally stupid reason to justify that $125K cash position. You need a new advisor or, better, you should just run your own money. Your instincts are good.

Start with " The Bogleheads' Guide to Investing"and " The Coffehouse Investor."

https://www.amazon.com/Bogleheads-Gu.../dp/0470067365

https://www.coffeehouseinvestor.com/

|

|

|

|

|

04-16-2019, 12:01 PM

|

#6

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

Quote:

Originally Posted by Which Roger

Don't have enough details to answer the question, but IMO if you are informed enough to be asking this question, including proposing that you invest in index funds, you don't need to pay 1% to an advisor. You can be a DIY investor. Also, your desire to index is the opposite of the advisor's desire to time the market.

|

Being a DIY investor stressed my husband out too much. He was constantly watching the market and couldn't relax. The 1% is well worth it to us. Plus, we get an amazing Harry and David basket at Christmas :-)

|

|

|

|

|

04-16-2019, 12:12 PM

|

#7

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by mtbikelover

Being a DIY investor stressed my husband out too much. He was constantly watching the market and couldn't relax.

|

A passive portfolio, as is recommended in the two books I linked, requires almost no maintenance or worrying. My wife and I look at our portfolio once a year, between Christmas and New Years. Some years we even make a trade or two.

I watch the market every day just like I watch fish in an aquarium. Pretty fish, bumbling around, no rhyme or reason to it. More interesting than a lava lamp. I never look at or calculate our portfolio value.

Quote:

Originally Posted by mtbikelover

The 1% is well worth it to us. Plus, we get an amazing Harry and David basket at Christmas :-)

|

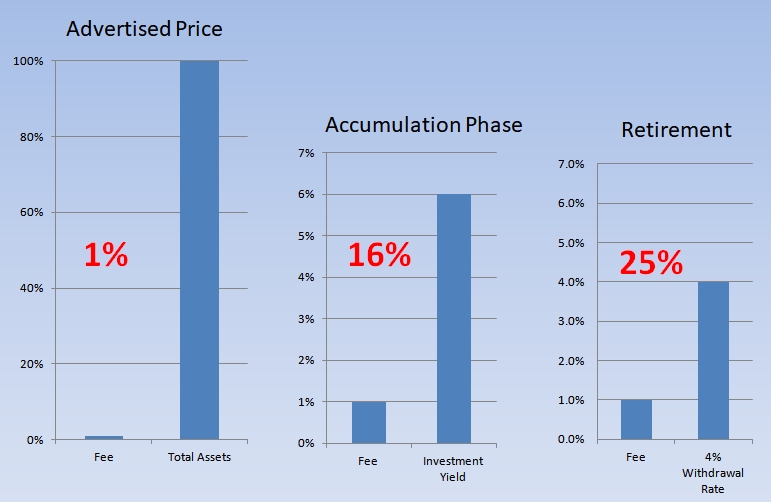

That's some pretty expensive fruit. Show DH this:

|

|

|

|

|

04-16-2019, 12:27 PM

|

#8

|

|

Full time employment: Posting here.

Join Date: Jul 2014

Posts: 930

|

I like to keep cash or cash like investments for at least 2 years of base living expenses. Yes, it earns little, but that's the price of insurance. I generally don't keep cash on hand waiting to invest, but then I'm largely a passive investor. If I get extra cash, I invest it consistent with my desired allocation

|

|

|

|

|

04-16-2019, 12:58 PM

|

#9

|

|

Thinks s/he gets paid by the post

Join Date: Jan 2018

Location: Elyria, OH

Posts: 1,937

|

Quote:

Originally Posted by mtbikelover

Being a DIY investor stressed my husband out too much. He was constantly watching the market and couldn't relax. The 1% is well worth it to us. Plus, we get an amazing Harry and David basket at Christmas :-)

|

So, despite what anyone here says to the contrary, you're going to continue to pay 1% to this FA, when you could easily put the cash in a MM mutual fund earning 2% and keep it all. Not to mention what that's doing to the rest of your portfolio.

|

|

|

|

|

04-16-2019, 01:09 PM

|

#10

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,373

|

You really have two issues here.

The first one was the essence of your OP and what to do with that $125k in cash. When he says that he is waiting for something good to buy... what does he mean? Individual equities? If so, just put it in VTI or similar and don't worry about it. (BTW, I'm not keen on individual equities to begin with and prefer index equities).

The second is why you need a FA even to begin with. Vanguard or Fidelity will provide a certain amount of advice for free.... or if you really need someone to hold your hand you could hire Vanguard for 0.30%... on $2.6m that is an annual savings of $18.2k... or two pretty nice dinners for a couple each week each year.... ie; not chump change.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

04-16-2019, 01:31 PM

|

#11

|

|

Moderator

Join Date: Nov 2015

Posts: 13,922

|

The 1% is only worth it if your FA is listening to you and looking at your whole picture. Does he know you have $450k cash? I won't push on the FA point much more, since you seem resigned to it and that's totally your call. But you do want an FA that listens to you. And you're already cash heavy in your non-FA stuff. He should be managing to your desired asset allocation and risk allowance.

As far as waiting for a good buy, that ship sailed recently. If he was really waiting, December was it. And what pray tell specifically is he looking at? Push him for specifics. If you want it invested, make him do it. He works for you. He's making $20k a year from you, make him earn it.

|

|

|

|

|

04-16-2019, 01:43 PM

|

#12

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,351

|

Quote:

Originally Posted by Aerides

... If you want it invested, make him do it. He works for you. He's making $20k a year from you, make him earn it.

|

I come at this a little differently:

1) The FA is saying stupid things, effectively saying he can time the market.

2) The OP is smart enough to recognize the stupidity.

Rather than turn the FA into a wildly expensive order clerk by self-directing the account, the OP should simply ditch him/her. From there either self-direct or at least cut the cost as @pb4uski suggests. I don't think you can go far wrong using Vanguard.

|

|

|

|

|

04-16-2019, 01:54 PM

|

#13

|

|

Moderator

Join Date: Nov 2015

Posts: 13,922

|

Quote:

Originally Posted by OldShooter

I come at this a little differently:

...

Rather than turn the FA into a wildly expensive order clerk by self-directing the account, the OP should simply ditch him/her. From there either self-direct or at least cut the cost as @pb4uski suggests. I don't think you can go far wrong using Vanguard.

|

I understand, but the OP ruled out dumping the FA in her post, so I'm working within her guidance (which is what the FA should do). If she wanted advice on dumping the FA and what to do next, that's a completely different thread, and a lot more fun.

Quote:

Originally Posted by mtbikelover

Being a DIY investor stressed my husband out too much. He was constantly watching the market and couldn't relax. The 1% is well worth it to us.

|

|

|

|

|

|

04-16-2019, 02:16 PM

|

#14

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

I hear you all on the FA but there are other reasons we use him which I didn't go into because I wasn't looking for advice on whether to have an FA or not.

First, my husband owns a business and needs to have someone manage his company's 401K. This FA handles that for him. So we have to pay someone to do that job anyway. The previous person he used was awful, too old, and did everything with paper and pencil and got my husband into things that were horrible investments just to pad his wallet. Anytime I asked a simple question (like maxing out his after tax contributions to his 401K and rolling that to a Roth as soon as we retire), the previous guy had no clue.

Second, this FA has also helped us with setting up custodial Roth IRA's for my two kids and they don't charge the 1% on that.

Third, we tried Fidelity. Numerous times. They were worthless. They could not give us any advice as they are not allowed to give stock advice.

Fourth, he has made some good investment decisions...things we never would have looked at. I have some stocks that are up 40% in the 14 months we have been with him. The portfolios that are invested are doing very well.

|

|

|

|

|

04-16-2019, 02:34 PM

|

#15

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

Quote:

Originally Posted by Aerides

The 1% is only worth it if your FA is listening to you and looking at your whole picture. Does he know you have $450k cash? I won't push on the FA point much more, since you seem resigned to it and that's totally your call. But you do want an FA that listens to you. And you're already cash heavy in your non-FA stuff. He should be managing to your desired asset allocation and risk allowance.

As far as waiting for a good buy, that ship sailed recently. If he was really waiting, December was it. And what pray tell specifically is he looking at? Push him for specifics. If you want it invested, make him do it. He works for you. He's making $20k a year from you, make him earn it.

|

We've told him we had cash but I don't think he realized how much. I did talk to him and told him that we would like all the cash he has invested and that if he ever thought there was something that was a really good buy to let us know and we would put more cash in. He said he would have it all invested today.

|

|

|

|

|

04-16-2019, 03:42 PM

|

#16

|

|

Thinks s/he gets paid by the post

Join Date: Jan 2018

Location: Elyria, OH

Posts: 1,937

|

Quote:

Originally Posted by mtbikelover

Third, we tried Fidelity. Numerous times. They were worthless. They could not give us any advice as they are not allowed to give stock advice.

|

I don't find Fidelity to be worthless at all, though I don't ask them for advice. It appears that you can get advice from them. For the benefit of others who haven't written them off yet:

https://www.fidelity.com/why-fidelity/planning-advice

|

|

|

|

|

04-16-2019, 04:03 PM

|

#17

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,892

|

Quote:

Originally Posted by mtbikelover

...

Third, we tried Fidelity. Numerous times. They were worthless. They could not give us any advice as they are not allowed to give stock advice. ...

|

That's a good thing. You don't need "stock advice". Just put your equity allocation into a broad-based index fund/ETF, and forget about it. It's the "stock advice" that is likely worthless (well, maybe 50% of the time).

Stop looking at the market, that doesn't make it go up. And when it goes down, looking doesn't tell you when it will stop. If you use an FA so you stop looking at the market, don't you want to look at the FA everyday? I'd be more worried about the FA than the market. That is just creating another piece to worry about.

You're making it too complicated.

Quote:

|

I did talk to him and told him that we would like all the cash he has invested and that if he ever thought there was something that was a really good buy to let us know and we would put more cash in. He said he would have it all invested today.

|

That sounds scary. He suddenly found a "good investment" today, because you told him to invest it? After waiting all this time?

-ERD50

|

|

|

|

04-16-2019, 04:05 PM

|

#18

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

Quote:

Originally Posted by gwraigty

|

We met with them 3x. All they did was plug all our info into their computer and tell us what our shortfall was. They could not advise us on investments and even said outright they weren’t allowed to do that. They couldn’t advise us on other investment options (like insurance). And they had no idea how to set up my husbands 401k. So they said they would get back to us. After 3 months of following up to see if they had figured it out, we gave up and found someone else.

|

|

|

|

|

04-16-2019, 04:12 PM

|

#19

|

|

Dryer sheet aficionado

Join Date: Apr 2019

Posts: 40

|

Quote:

Originally Posted by ERD50

That's a good thing. You don't need "stock advice". Just put your equity allocation into a broad-based index fund/ETF, and forget about it. It's the "stock advice" that is likely worthless (well, maybe 50% of the time).

Stop looking at the market, that doesn't make it go up. And when it goes down, looking doesn't tell you when it will stop. If you use an FA so you stop looking at the market, don't you want to look at the FA everyday? I'd be more worried about the FA than the market. That is just creating another piece to worry about.

You're making it too complicated.

That sounds scary. He suddenly found a "good investment" today, because you told him to invest it? After waiting all this time?

-ERD50

|

You made a lot of assumptions. I dont fret about the market. I simply didnt like having so much cash uninvested. And he invested it in index funds like I asked.

|

|

|

|

|

04-16-2019, 05:45 PM

|

#20

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,373

|

Quote:

Originally Posted by mtbikelover

.... They couldnt advise us on other investment options (like insurance). ....

|

Well... that is good because insurance is not a good investment... it's insurance.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode