CardsFan

Thinks s/he gets paid by the post

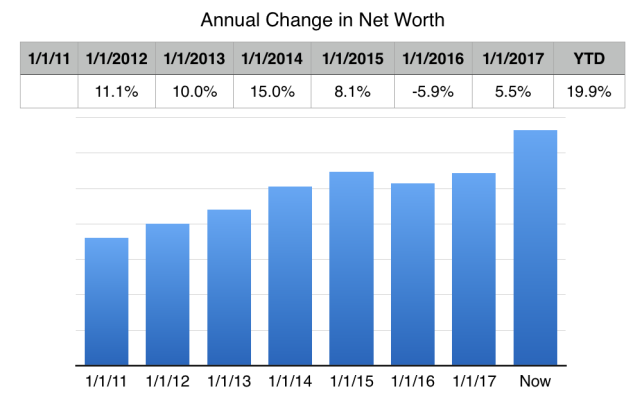

Year end is 14.6% (AA currently at 56/36/8)

")

Looks like everyone has had a great year with 15-20%+ returns. I'm curious, for those with bonds in their portfolio's, what returns did you see from them? Any bond or bond funds that stood above the rest?

For me, I have none, but do have $400K in a pension fund with 4.5% minimum return rate (adjustable to 1 year TBill + 1%, so 4.5% for quite some time to come). Just curious if I should move this to a bond fund for a bit higher rate.

Looks like everyone has had a great year with 15-20%+ returns. I'm curious, for those with bonds in their portfolio's, what returns did you see from them? Any bond or bond funds that stood above the rest?

For me, I have none, but do have $400K in a pension fund with 4.5% minimum return rate (adjustable to 1 year TBill + 1%, so 4.5% for quite some time to come). Just curious if I should move this to a bond fund for a bit higher rate.

Are you sure it is 1 year? My cash balance is 10 year +1%... but that still means minimum for now...

The values shown are daily data published by the Federal Reserve Board based on the average yield of a range of Treasury securities, all adjusted to the equivalent of a one-year maturity. The current 1 year treasury yield as of December 29, 2017 is 1.72%.

Are you sure it is 1 year? My cash balance is 10 year +1%... but that still means minimum for now...

+2........ 1 year TBill is 1.72% so +1% would be 2.72%, not 4.5%

Guess I can't be too unhappy with the 4.5% return.My bonds returned 3.15% in aggregate in 2017.

YTD DEC 2017 Investments Summary (target: 53 Equity / 42 Fixed / 5 Cash)YTD NOV 2017 Investments Summary (target: 53 Equity / 42 Fixed / 5 Cash)

401(k) Personalized Rate of Return is 24.57%.

- 11.83% YTD Weighted Performance overall for the whole pie.

From 01/01/2017 to 12/30/2017

Overall increase from previous month

- 12.71% American Funds American Balanced R6 Fund

- 28.99% American Funds New World R6 Fund

- 1.73% (not XIRR)