|

2B Capitulates -- Here's a Good Annuity

09-08-2007, 04:23 PM

09-08-2007, 04:23 PM

|

#1

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2006

Location: Houston

Posts: 4,337

|

2B Capitulates -- Here's a Good Annuity

__________________

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane -- Marcus Aurelius

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

09-08-2007, 05:12 PM

|

#2

|

|

Moderator Emeritus

Join Date: Jan 2007

Location: New Orleans

Posts: 47,498

|

Quote: Quote:

Originally Posted by 2B

|

Yep.  Assuming that SS doesn't just totally crater in the meantime.

__________________

Already we are boldly launched upon the deep; but soon we shall be lost in its unshored, harbourless immensities. - - H. Melville, 1851.

Happily retired since 2009, at age 61. Best years of my life by far!

|

|

|

|

09-08-2007, 05:49 PM

|

#3

|

|

Full time employment: Posting here.

Join Date: Nov 2006

Posts: 548

|

OR they stay solvent, but change the rules...

|

|

|

|

|

09-09-2007, 07:13 AM

|

#4

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2006

Location: Houston

Posts: 4,337

|

Unlike the insurance companies that sell annuities, the Feds print the money. It may debase the value but there will be money there. Changing rules are always a possibility; but even with every one agreeing the system needs to be fixed, any attempt is met with strong resistance. I suspect we'll see only minor tweeks during our lifetimes.

The key bit of info from the article is what I have been saying about annuities all along. The products available today have too much longevity built into them. To make the annuities available today worth buying, you have to outlive your mortality table by about 10 years. Only a very small percentage of the population will do that.

__________________

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane -- Marcus Aurelius

|

|

|

|

|

09-09-2007, 08:16 AM

|

#5

|

|

Recycles dryer sheets

Join Date: Aug 2007

Location: Midwest

Posts: 109

|

Quote:

|

To make the annuities available today worth buying, you have to outlive your mortality table by about 10 years. Only a very small percentage of the population will do that.

|

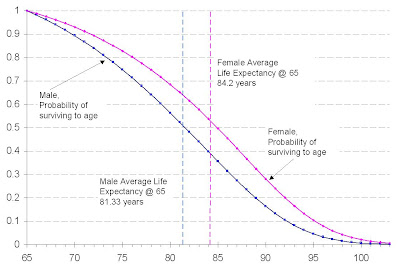

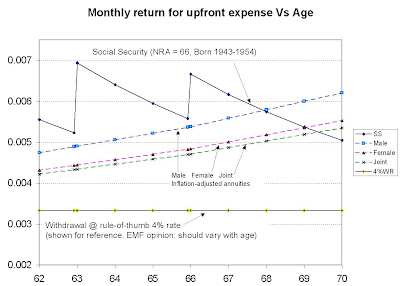

Here's a chart I worked up of survival probabilities at a future age for a 65-year-old from data at the SSA website.

It shows the probability of living more than 10 years past average life expectancy to be about 15%. You'd have to decide for yourself whether that is significant.

And another chart I worked up comparing SS to immediate annuities.

If the text is too small to read, more explanations here. Depending on your sex and marital status, delaying SS beats an immediate annuity. But immediate annuities compare favorably to a 4% SWR.

Social Security is more like a deferred annuity, with your heirs getting nothing if you die before starting benefits.

|

|

|

|

|

09-09-2007, 09:37 AM

|

#6

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2006

Location: Houston

Posts: 4,337

|

Quote:

Originally Posted by EngineeringMyFinances

Depending on your sex and marital status, delaying SS beats an immediate annuity. But immediate annuities compare favorably to a 4% SWR.

Social Security is more like a deferred annuity, with your heirs getting nothing if you die before starting benefits.

|

The key difference with the "4% SWR" is that it is very conservative. Following FIRECalc usually results in a substantial estate at the end or the opportunity to dramatically increase spending. With an immediate annuity, the best you get is what you bought. You'll leave no estate and your future payments depend on the continued solvency of the company you bought it from.

__________________

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane -- Marcus Aurelius

|

|

|

|

|

09-09-2007, 10:03 AM

|

#7

|

|

Moderator Emeritus

Join Date: Jan 2007

Location: New Orleans

Posts: 47,498

|

Quote:

Originally Posted by 2B

To make the annuities available today worth buying, you have to outlive your mortality table by about 10 years.

|

It seems to me that you are defining "worth buying" as being the same as "yielding the most possible total money received over a lifetime".

To me, the first $1000 that I receive each month is worth more than the second $1000, which is worth more than the third $1000, and so on.

The value of lifetime fixed or inflation adjusted fixed annuities (to me, in comparison with more volatile investments) is increased by the fact that the money stream is even and predictable.

Quote:

Originally Posted by 2B

The key difference with the "4% SWR" is that it is very conservative. Following FIRECalc usually results in a substantial estate at the end or the opportunity to dramatically increase spending. With an immediate annuity, the best you get is what you bought. You'll leave no estate and your future payments depend on the continued solvency of the company you bought it from.

|

Not everyone gives a hoot about leaving an estate. Death has a way equalizing things. And ask former Enron investors about what can happen with equities when a company swallows its a**! Annuities aren't all alone in that risk. Do you really think a 4% SWR is so very conservative? I have been using 3.5% in my computations for a 40 year retirement, and only use 4% when I am trying to "force" things to work out the way I would like. But then, I also dream about 5% with enough in CD's to withdraw 0% for up to 10 years of market doldrums.

__________________

Already we are boldly launched upon the deep; but soon we shall be lost in its unshored, harbourless immensities. - - H. Melville, 1851.

Happily retired since 2009, at age 61. Best years of my life by far!

|

|

|

|

|

09-09-2007, 10:06 AM

|

#8

|

|

Full time employment: Posting here.

Join Date: Nov 2006

Posts: 548

|

Golf clap to EMF for that work.

Nice presentation, Thanks -- Great Blog, too!

|

|

|

|

|

09-09-2007, 10:07 AM

|

#9

|

|

Recycles dryer sheets

Join Date: Aug 2007

Location: Midwest

Posts: 109

|

Depends on your definition of "very conservative". A 65-year-old female from the chart above has a 10% chance of living 30 years, and a 4% SWR has a 5% chance of failure at 30 years. So she'd have a 0.5% chance of reaching the age of 95 with no money. And a higher chance of outliving her money, because her portfolio could last a bit longer but she could live even longer. And if she retired at an age younger than 65, she has an even greater chance of living for 30 years.

A 5% annual withdrawal rate would be about .0042 on my 2nd chart (which is withdrawal rate per month). Portfolio failure rate 30 years in would be much greater than 5%. But immediate annuities compare favorably even at a 5% withdrawal rate.

Yes, there's the risk that the annuity insurer could go broke. But there will always be risk. The US economy could go down the tubes. Personally, I may consider part of my retirement in an immediate annuity, but would be reluctant to put all my eggs in one basket. My employer's pension offers a lump sum or the option to annuitize with a payment higher than that available at Vanguard even for a mail. When the time comes, I 'll look at it closer and probably will take the monthly payments.

|

|

|

|

|

09-09-2007, 10:20 AM

|

#10

|

|

Moderator Emeritus

Join Date: Jan 2007

Location: New Orleans

Posts: 47,498

|

Quote:

Originally Posted by EngineeringMyFinances

Personally, I may consider part of my retirement in an immediate annuity, but would be reluctant to put all my eggs in one basket. My employer's pension offers a lump sum or the option to annuitize with a payment higher than that available at Vanguard even for a mail. When the time comes, I 'll look at it closer and probably will take the monthly payments.

|

I can get a fixed, immediate annuity with part or all of my TSP (=401K). I am thinking about doing that with maybe 25%-33% of it. Right now, that annuity would pay 8.58% at age 62, or 6.288% if inflation protected (to an extent). I would probably get the latter. It's not a great rate, but since my pension and SS are both tiny I am thinking about it. Even more than that, I am also thinking about delaying getting my SS, at least to age 66. I want that first $2K/month to be locked in! Beyond that, it is all play money.

__________________

Already we are boldly launched upon the deep; but soon we shall be lost in its unshored, harbourless immensities. - - H. Melville, 1851.

Happily retired since 2009, at age 61. Best years of my life by far!

|

|

|

|

|

09-09-2007, 02:09 PM

|

#11

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2006

Location: Houston

Posts: 4,337

|

Quote:

Originally Posted by Want2retire

It seems to me that you are defining "worth buying" as being the same as "yielding the most possible total money received over a lifetime".

Do you really think a 4% SWR is so very conservative? I have been using 3.5% in my computations for a 40 year retirement, and only use 4% when I am trying to "force" things to work out the way I would like. But then, I also dream about 5% with enough in CD's to withdraw 0% for up to 10 years of market doldrums.

|

You're right about my definition of "worth buying." The goal is the largest cash flow stream from a fixed investment.

My annuity comparison is with laddered high grade corporate bonds. I then eat my principal and interest as the bonds mature over 30 years. That says that if I live longer that annuity may not have been too bad but then my expenses will be limited to the assisted living or nursing facility I'll probably be in by then. If I assume that inflation is 3% over that period and get an average return of about 6% (fairly conservative based on what I'm seeing in the bond market), I can duplicate your 6.288% return for about 85% of what the annuity costs. I can put that 15% into long term investments that will let me restart the program if I'm still alive in 30 years. All the while, I'll still have the assets available if I want to do something different.

I currently have about 7 years of living expenses in money markets, CDs and bonds. When I finish rebalancing, I'll have 10.

I understand that it sounds so nice to have that check in the mail every month from the friendly insurance company but there are a lot of fees buried in the purchase price. I also do not feel comfortable with me being an unsecured creditor should they go belly up. I feel much safer with a diversified portfolio and a rational asset allocation strategy.

__________________

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane -- Marcus Aurelius

|

|

|

|

|

09-10-2007, 08:02 AM

|

#12

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Aug 2006

Posts: 12,483

|

Just a helpful hint.........some of the LARGEST buildings in the MOST EXPENSIVE real estate in the US are owned by insurance companies.......

__________________

Consult with your own advisor or representative. My thoughts should not be construed as investment advice. Past performance is no guarantee of future results (love that one).......:)

This Thread is USELESS without pics.........:)

|

|

|

|

|

09-10-2007, 08:05 AM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Aug 2006

Posts: 12,483

|

__________________

Consult with your own advisor or representative. My thoughts should not be construed as investment advice. Past performance is no guarantee of future results (love that one).......:)

This Thread is USELESS without pics.........:)

|

|

|

|

|

09-10-2007, 09:04 AM

|

#14

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Feb 2005

Location: Central MS/Orange Beach, AL

Posts: 9,071

|

Quote:

Originally Posted by 2B

You're right about my definition of "worth buying." The goal is the largest cash flow stream from a fixed investment.

My annuity comparison is with laddered high grade corporate bonds. I then eat my principal and interest as the bonds mature over 30 years. That says that if I live longer that annuity may not have been too bad but then my expenses will be limited to the assisted living or nursing facility I'll probably be in by then. If I assume that inflation is 3% over that period and get an average return of about 6% (fairly conservative based on what I'm seeing in the bond market), I can duplicate your 6.288% return for about 85% of what the annuity costs. I can put that 15% into long term investments that will let me restart the program if I'm still alive in 30 years. All the while, I'll still have the assets available if I want to do something different.

I currently have about 7 years of living expenses in money markets, CDs and bonds. When I finish rebalancing, I'll have 10.

I understand that it sounds so nice to have that check in the mail every month from the friendly insurance company but there are a lot of fees buried in the purchase price. I also do not feel comfortable with me being an unsecured creditor should they go belly up. I feel much safer with a diversified portfolio and a rational asset allocation strategy.

|

Interesting view. I have roughly the same amount in cash/bonds. I'm thinking about delaying SS to at least 66 as want2retire, but I'm only 53 so who knows what SS will like 10-15 years from now.

I think one reason some are comfortable with an immediate annuity is because it's just an easy way to handle your cash flow needs. Small annuity + SS = monthly cash flow requirements. Some people that are 65 and over just want to keep it simple. Who knows how well our minds will hold up as we age. Might be a good way to insure we don't blow all our investments as we age. Not sure if I will buy one or not but it's a possibility.

2B, just curious.........what is your overall investment allocation?

__________________

Retired 3/31/2007@52

Investing style: Full time wuss.

|

|

|

|

|

09-10-2007, 09:22 AM

|

#15

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2006

Posts: 2,844

|

Quote:

Originally Posted by Dawg52

I think one reason some are comfortable with an immediate annuity is because it's just an easy way to handle your cash flow needs. Small annuity + SS = monthly cash flow requirements. Some people that are 65 and over just want to keep it simple. Who knows how well our minds will hold up as we age. Might be a good way to insure we don't blow all our investments as we age. Not sure if I will buy one or not but it's a possibility.

2B, just curious.........what is your overall investment allocation?

|

Dawg I think that is the basic arguement for an annuity. The number of elders I have seen that have taken lump sums and lost their investments through poor investments or gambled at the boats is sad. When one is young they may think quite a bit more clearly than when they are in their '80's. In looking for excitement as they age incredibly bad decisions are made.

__________________

But then what do I really know?

https://www.early-retirement.org/forums/f44/why-i-believe-we-are-about-to-embark-on-a-historic-bull-market-run-101268.html

|

|

|

|

|

09-10-2007, 03:04 PM

|

#16

|

|

Moderator Emeritus

Join Date: Jun 2007

Location: At The Cafe

Posts: 6,873

|

Quote:

Originally Posted by 2B

The key difference with the "4% SWR" is that it is very conservative. Following FIRECalc usually results in a substantial estate at the end or the opportunity to dramatically increase spending. With an immediate annuity, the best you get is what you bought. You'll leave no estate and your future payments depend on the continued solvency of the company you bought it from.

|

Yeah, continued solvency! Anyone else remember Executive Life which went belly up in the early '90s? My company discontinued a defined-benefit plan and set us up in Executive Life annuities, just before Executive Life failed. Small annuities like mine were given priority and sold to Aurora after I sweated it out for a year or so.

One really sad side-note to this was that a meeting to explain the new benefit plan was post-poned because the guy who sold us the Executive Life annunities had committed suicide.

I'm setting up a cash flow to come from Ginnie Maes; along with some stock funds, etc. to balance. My favorite advice on annunities is to wait until you are 75 or so and re-evaluate your situation; the older you are the better the deal? Since I think I come from a short-lived family, that might work for me. But than again, what you folks say here about older minds, is also something to think about; guess I could go with the plan to have my investment companies send me automatic checks.

|

|

|

|

|

09-10-2007, 03:47 PM

|

#17

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2006

Posts: 2,844

|

As I recall, the holders of annuities from Executive Life fared far better than the sellers of the annuities. After originally cutting payments by 30 percent on monthly payouts the annuities were eventually paid in full. The owners (i.e. sharreholders) went belly-up. Guess they needed a better pencil sharpner. The risk on annuities is far far less than the risk on the solvency of the issuer, although you do not want your issuer to go belly up that's for sure.

__________________

But then what do I really know?

https://www.early-retirement.org/forums/f44/why-i-believe-we-are-about-to-embark-on-a-historic-bull-market-run-101268.html

|

|

|

|

|

09-10-2007, 06:57 PM

|

#18

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2006

Location: Houston

Posts: 4,337

|

Quote:

Originally Posted by Dawg52

2B, just curious.........what is your overall investment allocation?

|

My end goal is as follows:

- 40% cash/bonds/CDs (currently a little over this)

- 20% foreign

- 10% small cap US

- 30% US Large/Value (currently a little over this)

I'm waiting for the current gyrations to stop so I can complete my rebalancing.

__________________

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane -- Marcus Aurelius

|

|

|

|

|

09-10-2007, 06:59 PM

|

#19

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2006

Location: Houston

Posts: 4,337

|

Quote:

Originally Posted by Running_Man

As I recall, the holders of annuities from Executive Life fared far better than the sellers of the annuities. After originally cutting payments by 30 percent on monthly payouts the annuities were eventually paid in full. The owners (i.e. sharreholders) went belly-up. Guess they needed a better pencil sharpner. The risk on annuities is far far less than the risk on the solvency of the issuer, although you do not want your issuer to go belly up that's for sure.

|

There have been isolated but similar incidents. Everyone didn't turn out so well. That's one of the reasons I'm careful about VAs. The companies that sell them frequently put them in subsidiary holding companies. If things fall apart, it's the sub that goes down and not the big mega insurance company.

__________________

The object of life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane -- Marcus Aurelius

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|