veremchuka

Thinks s/he gets paid by the post

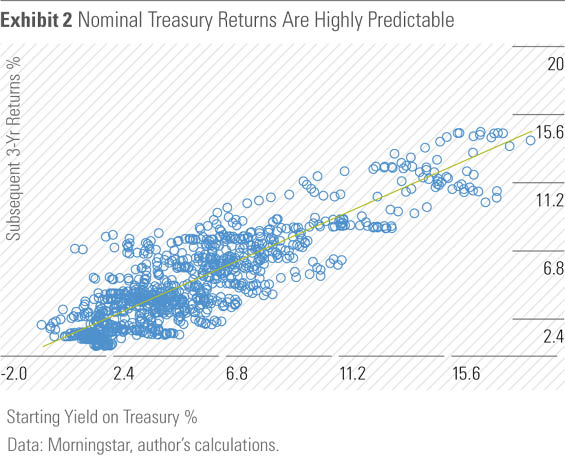

I found this article surprising. I have no idea who the author is, I found the link at The Finance Buff . Here's the link to the article Bond Fund vs CD In the Next Five Years

This was of interest to me because I hold the Vanguard Short-Term Investment-Grade Fund Admiral Shares and the Vanguard Intermediate Term Investment Grade Fund Admiral Shares in my rollover IRA. In addition to that, I have all of my 401k in the Stable Value fund whose yield is about 3.15% this year and this fund I'd compare to the CD except the nav can appreciate a bit but it does not lose nav like a bond fund.

So from reading this I think I'm making a mistake holding the ITIG fund whose average duration is 5.3 years yield of 2.96% as it strikes me as being almost the same as the Vanguard Total Bond Market Index Fund Admiral Shares 5.4 duration and yield of 2.2%. I want to get my AA up from 50/50 to 60/40 but with equities so high and the powerful year end effect I'm wondering when. I was going to use money in the Stable Value to do this but now I think it should come from the ITIG fund.

I'm not asking what to do just pointing out what this article says and how it effects me and perhaps you.

ETA: After reading the article neither bond fund is very good compared to the CD! I focused on the IT fund but we all know the interest rates won't go up 2.7% immediately for the ST fund! Retirees live in interesting times re their fixed income investments! My Stable Value really looks to be a better choice than either bond fund I hold.

This was of interest to me because I hold the Vanguard Short-Term Investment-Grade Fund Admiral Shares and the Vanguard Intermediate Term Investment Grade Fund Admiral Shares in my rollover IRA. In addition to that, I have all of my 401k in the Stable Value fund whose yield is about 3.15% this year and this fund I'd compare to the CD except the nav can appreciate a bit but it does not lose nav like a bond fund.

So from reading this I think I'm making a mistake holding the ITIG fund whose average duration is 5.3 years yield of 2.96% as it strikes me as being almost the same as the Vanguard Total Bond Market Index Fund Admiral Shares 5.4 duration and yield of 2.2%. I want to get my AA up from 50/50 to 60/40 but with equities so high and the powerful year end effect I'm wondering when. I was going to use money in the Stable Value to do this but now I think it should come from the ITIG fund.

I'm not asking what to do just pointing out what this article says and how it effects me and perhaps you.

ETA: After reading the article neither bond fund is very good compared to the CD! I focused on the IT fund but we all know the interest rates won't go up 2.7% immediately for the ST fund! Retirees live in interesting times re their fixed income investments! My Stable Value really looks to be a better choice than either bond fund I hold.

Last edited: