Gone4Good

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- Sep 9, 2005

- Messages

- 5,381

CPI is not rigged.

TIPS are safe.

TIPS are safe.

I tell you my world view is very different from the original poster's view. Maybe he shouldn't use me as a model - LOL!

But I own equities to hedge against long-term inflation and I make sure I have a healthy foreign exposure in both my stock and bond allocations to hedge against US dollar decline.

Audrey

DW and I were also very worried about investing in the market, and had a lot of cash just sitting in CD's earning a whopping 3%. We were very nervous that inflation was going to eat our nest egg. A once in a lifetime opportunity (for us anyway) came by when a beach house came on the market for an absolute screaming deal price. We decided to get rid of the cash and buy our future retirement home in a place we called heaven. My parents will be moving into the beach house and be live in caretakers, so when we retire we will sell our current house (25 years from now) and move in. I know realestate is risky today, but 25 years from now, I have full confidence our money will be hedged against inflation.

Our beach house venture should be paid in full within 4 years. Current house is paid in full. We are still in the market with our fully funded 401k's, but that is all I am willing to risk.

This is pretty much what we did 25 years ago and it DID work out very well for us. We didn't have parents to live in the place for us, but we did have a good rental agent who looked out for us (for a price, of course).

Clearly, real estate can be a good way to invest some of your funds - especially if it's in a place you eventually want to live. Best of luck!!

From this statement it sounds like you feel that the misalignment of your politics and their politics is bad for your portfolio. You might want to look at times when your politics were reflected in the past administration. Was your politics correlated with past good equity and/or bond returns? If there was a good correlation then just invest in equities and/or bonds when your political opinions are reflected in the current government and be out of the markets (and in CD's or something low risk) otherwise....(snip)...

Is anyone else in the same situation? I used to be so confident with my investing skills, but with the new administration I feel like all bets are off. ...

I tell you my world view is very different from the original poster's view. Maybe he shouldn't use me as a model - LOL!

But I own equities to hedge against long-term inflation and I make sure I have a healthy foreign exposure in both my stock and bond allocations to hedge against US dollar decline.

Audrey

Fidelity Strategic Income FSICX holds foreign govt, foreign corporate, and emerging market debt in its portfolio. It's a wild ride though!!!Audrey -

What has been your foreign bond investment vehicle?

I too am not optimistic about the next several years (nothing to do with politics). I always said if I could get my portfolio back close to where it was at the end of 2007, I would reallocate my assets. Well I got there recently so on Monday morning I cashed out of apple and google with plans of increasing the bond side of my portfolio.

Wouldn't you know it? Apple and Google went on a tear this week and as of closing today, I left about 50K on the table.

I have a healthy foreign exposure in both my stock and bond allocations to hedge against US dollar decline.

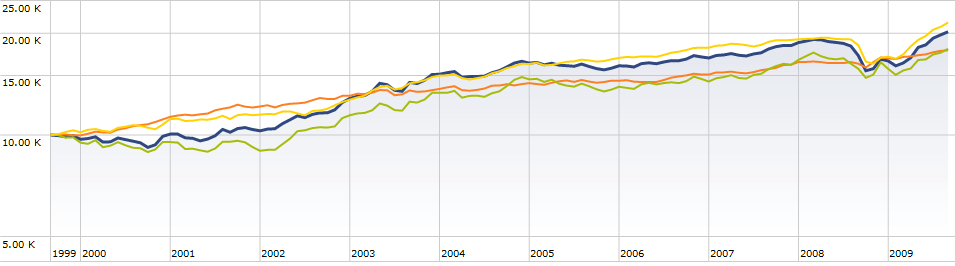

So you are saying that the US dollar has significantly declined over that time period - 1999 to present - but that those bond funds did not outperform US bond index funds? That is disappointing! I'll have to take a closer look.One thing I noticed in both the Loomis Global Bond fund (which I own) and T. Rowe Price's international bond fund is that they haven't generated excess returns due to the declining dollar over the last 10 years. While their volatility tracks with that of the dollar, their long-run returns are very similar to a plain old bond index. Neither one hedges currency exposure.

I've looked at this several times and always end up wondering if all you get with a foreign bond fund is added volatility.

So you are saying that the US dollar has significantly declined over that time period - 1999 to present - but that those bond funds did not outperform US bond index funds? That is disappointing! I'll have to take a closer look.

We have no confidence that the market will not take a nose dive going forward.

100% TIPS? Lets see, these financials instruments were created by the government. As such, there is obviously 0% probability of the rules being changed and or future "adjustments" to CPI calculation basis. Talk about all eggs in one basket...

Hmmm - what does the graph say about no dividends or coupons?

Here's one "expert" who thinks stocks have no place in a retirement portfolio.

Ha