twaddle

Thinks s/he gets paid by the post

- Joined

- Jun 16, 2006

- Messages

- 1,703

Pssst - Wellesley! 4.31% current yield as of Friday.rolleyes number.

Pssst - Wellesley! 4.31% current yield as of Friday.rolleyes number.Try a chart of the value of money invested instead of playing games. Do remember to add the dividends.

Except for the depression and the sideways 60's, no protracted loss of value.

There are always uncertainties, but planning for the absolute worst and living your entire life that way might suck more than working until you're 70. Be adaptable. Expect to improvise. Limit your liabilities without reducing your quality of life. Have a backup reduction budget and a bare-bones one. Dont take on excessive risk without clear benefits that make the risk acceptable.

It aint rocket science.

I handle it by using a straight X% withdrawal rate rather than the inflation adjusted initial 4% rate as used in the original SWR.

This means that I take more out when the market has been good, but it also means that the portfolio is not being depleted at a high percentage rate when performing poorly. Such an approach means you have to be willing to take a pay cut now and then in the interest of preserving the portfolio. I guess this bothers some people, but it doesn't bother me at all.

I never felt comfortable with taking an initial fixed rate + inflation adjustment each year disregarding market performance. This technique was developed for folks who needed a constant "salary" each year mimicking the financial "predictability" of their working years. I would rather react quickly once entering years of poor portfolio performance.

And instead of doing some kind of artificial annual "inflation adjustment", I prefer to let my portfolio grow enough to supposedly beat inflation over the long run and thus keep up with increasing costs of living by whatever my porfolio performance provides.

It's insane to debate whether a portfolio can survive under a series of consecutive market declines. It's almost like talking about whether you can survive if a huge asteroid struck the earth or the global economy entered a prolong, say 100 years, depression. We just have to be pragmatic about the world. Can we really identify or prepare for all the worst-case scenarios?

This thread is about exploring the paths of net worth in ordinary already experienced times.

Perhaps it might be insane, to use your word, to expect the future to be markedly better than the past?

Ha.

Perhaps it might be insane, to use your word, to expect the future to be markedly better than the past?

Anyone ever look at the "dark ages" in Firecalc (1929, 1972, etc) and re-run assuming 1/4 to 1/2 of the equities in the mix are International ?

Better speak to one of the others on this request.Give me faith, Ha. Tell me we'll have another 20 years of P/E expansion, will ya?

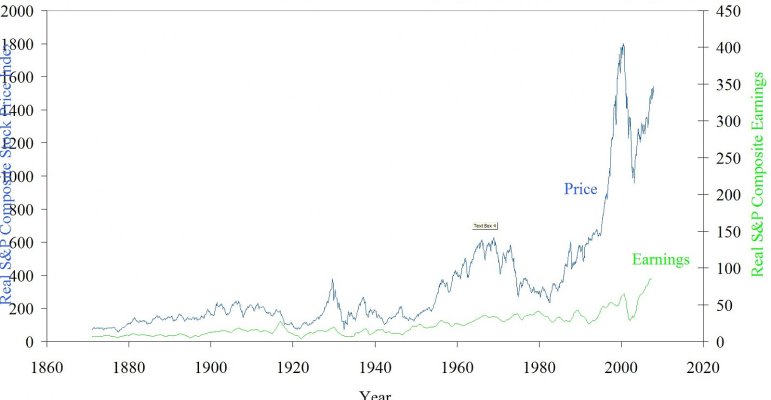

And guys, if your showing long term charts you need to do it with semilog on the y-axis or it just doesn't give the right picture for growth rates.

I was relieved to find that I could withdraw up to $100K without going over an SWR of 3%.

Depends on whether you're trying to show long-term growth or bull runs and bear declines. There's no "one scale fits all."

Don't forget that if you simply stick your money under your mattress, you can safely withdraw 3.33% (not adjusted for inflation) over 30 years.

That doesn't mean your mattress is a great asset class, but that's what we should use as a baseline.

I think the opposite is more doable. If you are living on your total income, and spending for non essentials, then tightening the belt is possible. If you have always LBYM, then there is no stretch room.

I feel fairly confortable with a 4% SWR, even knowing that I could end up with nothing at the end. But I will enjoy the luxury to have a few backups (in case things go south) to keep me sleeping at night:

Social Security benefits which I never include in my projections.

A substantial inheritance which I will probably receive after FIREing, so again not included in my projections.

Home equity, which can be tapped via reverse mortgage if needed, is not included in my calculations.

A retirement budget consisting of 50% fixed expenses and 50% discretionary expenses. So if the market really plunges our expenses could be cut in half temporarily.

A proven ability to live cheaply and be happy with it.