|

|

How Bond Funds Rolling Down the Yield Curve Help Defend Against Rising Rates

12-07-2017, 06:34 PM

12-07-2017, 06:34 PM

|

#1

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,139

|

How Bond Funds Rolling Down the Yield Curve Help Defend Against Rising Rates

Somehow I missed this gem of an article from Kitces comparing the total return holding a bond to maturity versus a reinvesting constant maturity bond (acting like a bond fund) during rising rates.

When Kitces wrote this two years ago, the 5 year treasury was at 1.75%, and the Fed hadn't started raising raising rates. The 5 year treasury has made it to a little over 2.1% now, and the Fed has raised interest rates 0.25% three times and is expected to do a fourth raise this month. The yield curve has flattened, so short-term rates have increased quite a bit more than intermediate rates, and long-term rates have dropped.

Quote: Quote:

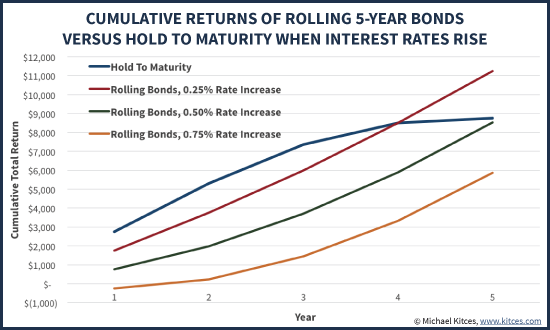

So how much of an interest rate increase does it take for the two to offset? As the graphics show below, even if rates increase an average of 0.25%/year – returning to 3% yield on the 5-year Treasury by the end of the decade – the investor still has a better cumulative return by rolling the bonds. In this case, the price decline from rising rates effectively offsets the price increase from rolling down the yield curve, but the investor still gets to keep reinvesting at higher yields, producing more total return. At a 0.50%/year rate increase – pushing the 5-year to 4.25% by the end of the decade – the scenarios come out the same, as the small annual price losses that are recognized by rolling the bonds in rising rates are offset by the higher yields obtained by reinvesting into new bonds. If rates rise at a more ‘extreme’ rate, by 0.75%/year – putting the 5-year Treasury at a whopping 5.50% by the end of the decade, a yield it hasn’t seen since the year 2000(!) – the investor still has a positive total return, at just a slight loss to the buy-and-hold investor.

Cumulative Returns Of Rolling 5-Year Bonds Vs Holding To Maturity As Interest Rates Rise [X% per year over five years] Cumulative Returns Of Rolling 5-Year Bonds Vs Holding To Maturity As Interest Rates Rise [X% per year over five years]

As the results show, there is a point at which rising rates will make it unfavorable to hold a bond fund over just sitting on individual bonds until maturity. However, the required magnitude of rate increases must be quite significant – even a scenario where rates rise fast enough in the next 5 years to offset all the rate decreases of the past 15 years (back to 2000!) still only results in a slight loss of total return compared to just buying and holding the bonds!

|

A lot more good stuff in the article: https://www.kitces.com/blog/how-bond...nterest-rates/

__________________

Retired since summer 1999.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

12-07-2017, 08:21 PM

|

#2

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2003

Posts: 18,085

|

Hmmm, for me the importance of buying bullet funds is driven by the extension risk ("negative convexity") posed by the MBS holdings of many broad bond funds. This is a risk I am unwilling to take at this point in the rate cycle, so I want a certain maturity for the bonds in my funds.

__________________

"All animals are equal, but some animals are more equal than others."

- George Orwell

Ezekiel 23:20

|

|

|

|

|

12-07-2017, 08:42 PM

|

#3

|

|

Thinks s/he gets paid by the post

Join Date: Dec 2016

Location: DC area

Posts: 2,493

|

Quote:

Originally Posted by audreyh1

Somehow I missed this gem of an article from Kitces

|

Good stuff. Seriously, if Kitces put his stuff in a book I would buy it. It looks like he has a couple of books aimed at the FA industry, but nothing on all his great investment/retirement work.

__________________

FI and Semi-ER March 24, 2017

Consulting to stay engaged

"All models are wrong, some are useful." - George Box

There is always a well-known solution to every human problem: neat, plausible, and wrong. - H.L. Mencken

|

|

|

|

|

12-08-2017, 08:03 PM

|

#4

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,139

|

Quote:

Originally Posted by brewer12345

Hmmm, for me the importance of buying bullet funds is driven by the extension risk ("negative convexity") posed by the MBS holdings of many broad bond funds. This is a risk I am unwilling to take at this point in the rate cycle, so I want a certain maturity for the bonds in my funds.

|

That's true - core/index bond funds that hold a lot of mortgage-backed securities will see some lengthening of duration and thus a bigger hit from rising interest rates. Modeling that stuff is above my pay grade. Bond index benchmark AGG is 38% asset backed bonds.

The Fed will be unloading (well, not repurchasing) a lot of MBS too.

__________________

Retired since summer 1999.

|

|

|

|

|

12-09-2017, 12:19 PM

|

#5

|

|

Recycles dryer sheets

Join Date: Jul 2013

Posts: 317

|

Not wanting to veer off course but I have a question or two. Please humor me, as I don't really understand the bond side very well.

1. Would an intermediate term fund with little to no MBS be preferable to Vanguard's Total Bond fund?

2. Under what, if any conditions would a long term Bond fund be a wise choice?

I'm at about 60/40 with all bonds in Total Bond fund. Stocks are all over the place but moving to TSM fund.

I'm in withdrawl mode and taking capital gains as need while staying in a good position for ACA.

Thanks,

Murf

|

|

|

|

|

12-09-2017, 01:24 PM

|

#6

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2003

Posts: 18,085

|

Murf, total bond indices hold a chunk (Audrey references 38%) of MBS and similar things. The problem I have with MBS in this environment is that they are usually backed by 3 year fixed mortgages. Bond managers estimate (guess) what the real payback period will be. It definitely will be shorter than 30 years and longer than 1, but nobody knows for sure what it will be because the underlying borrowers have the right to pay it back at par any time they like. A lot of holders of this paper got stung as rates fell because they bought, say, a 5% bond figuring it would be around for maybe 7 years and perhaps paid a premium to par. Rates dropped, everybody in the pool refinanced, and they got back par a year or two later having to reinvest at lower rates and suffer a permanent loss of the premium they paid. As rates potentially rise, the 3.5% bond you think will be paid off in 5 years could extend to 10 or 15 if we get back to a world of 5% 30 year fixed mortgages. Why? Because who in their right mind would refi a 3.5% mortgage to a 5% mortgage? So just as rates rise and you would like to be rolling down the maturity schedule so you can reinvest at the now-higher rate, your effective maturity goes farther out.

When does MBS beat straight maturity (AKA bullet) bonds? When rates stay more or less the same for a long time. That way you get aid a premium for the extension/early repayment risk yet you don't get stung.

__________________

"All animals are equal, but some animals are more equal than others."

- George Orwell

Ezekiel 23:20

|

|

|

|

|

12-09-2017, 02:03 PM

|

#7

|

|

Recycles dryer sheets

Join Date: Jul 2013

Posts: 317

|

Thanks Brewer. So with rates likely to rise, would a switch from Total Bond fund with 38% MBS to Intermediate Index with 0% MBS be warranted?

Thanks,

Murf

|

|

|

|

|

12-09-2017, 03:43 PM

|

#8

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2003

Posts: 18,085

|

Quote:

Originally Posted by Murf2

Thanks Brewer. So with rates likely to rise, would a switch from Total Bond fund with 38% MBS to Intermediate Index with 0% MBS be warranted?

Thanks,

Murf

|

Depends on how quickly they rise, how far, and whether it even happens. Personally, I am uncomfortable with the risk profile of MBS, so I am willing to substitute CDs, corporate investment grade bonds and treasuries for the MBS. Likely I am giving up a bit of yield in the process and accepting some additional commercial credit risk as part of the bargain. You have to decide what your outlook is for the future and how much risk you wish to take.

__________________

"All animals are equal, but some animals are more equal than others."

- George Orwell

Ezekiel 23:20

|

|

|

|

|

12-09-2017, 05:39 PM

|

#9

|

|

gone traveling

Join Date: Dec 2016

Posts: 733

|

Though not as technically astute as Brewer. In general rising rates are bad for bonds. My FA, told me the "managers" were mitigating the risk in the bonds, and we didn't need to get out 3 years ago. Needless to say he lost us nearly 8% of the 50/50 balanced portfolio over 3 years, after you take out the income produced from the portfolio.

Should be kicking myself but closest I can get is

I'm currently going to cash and a 3 month CD.

|

|

|

|

|

12-09-2017, 07:07 PM

|

#10

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,139

|

Quote:

Originally Posted by Luck_Club

Though not as technically astute as Brewer. In general rising rates are bad for bonds. My FA, told me the "managers" were mitigating the risk in the bonds, and we didn't need to get out 3 years ago. Needless to say he lost us nearly 8% of the 50/50 balanced portfolio over 3 years, after you take out the income produced from the portfolio.

Should be kicking myself but closest I can get is

I'm currently going to cash and a 3 month CD. |

Losing 8% in a 50/50 portfolio over the last three years had nothing to do with rising rates. Bond funds did just fine over the past three years. Intermediate funds as a group gained around 7% total return during the past three years, and a few did much better - 8-10%. Intermediate bond funds were flat during 2015, but then made up for it over the next two years.

__________________

Retired since summer 1999.

|

|

|

|

|

12-09-2017, 11:29 PM

|

#11

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2014

Location: Spending the Kids Inheritance and living in Chicago

Posts: 17,086

|

Quote:

Originally Posted by audreyh1

Losing 8% in a 50/50 portfolio over the last three years had nothing to do with rising rates. Bond funds did just fine over the past three years. Intermediate funds as a group gained around 7% total return during the past three years, and a few did much better - 8-10%. Intermediate bond funds were flat during 2015, but then made up for it over the next two years.

|

As I slowly increase my non-stock allocation by lowering my VERY high stock allocation (~93%) what would you recommend ?

Currently I have some

BND (easy to buy, and stays fairly constant).

Some BSJM & BSJJ (high rate corp bonds etf's that are term limited).

Some Preferred shares which pay out 5.5% to 7.5%

But I don't really know what else to buy, so I default to BND, as I don't understand even how to buy treasury TIPs.

|

|

|

|

|

12-10-2017, 12:38 AM

|

#12

|

|

Recycles dryer sheets

Join Date: Nov 2017

Posts: 275

|

Quote:

Originally Posted by Luck_Club

Though not as technically astute as Brewer. In general rising rates are bad for bonds. My FA, told me the "managers" were mitigating the risk in the bonds, and we didn't need to get out 3 years ago. Needless to say he lost us nearly 8% of the 50/50 balanced portfolio over 3 years, after you take out the income produced from the portfolio.

Should be kicking myself but closest I can get is

I'm currently going to cash and a 3 month CD. |

"Where are the customers' yachts?"

Not wanting to derail the thread, but something is drastically wrong with this picture.

|

|

|

|

|

12-10-2017, 06:18 AM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,139

|

Quote:

Originally Posted by 43210

"Where are the customers' yachts?"

Not wanting to derail the thread, but something is drastically wrong with this picture.

|

I didnt catch the part about performance after taking out the income from the portfolio. I wonder how much that income was and whether it includes cap gains distributions?

Anyway, performance after removing income makes a difference, slough losing 8% over the past three years still seems like much. Without knowing how much was removed from the portfolio its impossible to gage.

__________________

Retired since summer 1999.

|

|

|

|

|

12-10-2017, 06:56 AM

|

#14

|

|

gone traveling

Join Date: Dec 2016

Posts: 733

|

Quote:

Originally Posted by audreyh1

I didnt catch the part about performance after taking out the income from the portfolio. I wonder how much that income was and whether it includes cap gains distributions?

Anyway, performance after removing income makes a difference, slough losing 8% over the past three years still seems like much. Without knowing how much was removed from the portfolio its impossible to gage.

|

The more I review the more angry I become.

Using example numbers:

Portfolio in 2013 = $1,000,000

Withdraws over the 3 years =$139,568

Portfolio Value today =$916,312

Total income generated over the past 3 years = $134,761

The disgusting part is the portfolio was so confusing, that I only finally got a true picture of what was going on when the adviser provided a performance report to me last week. Prior to that I was constantly asking him about reducing risk in the bond portion. He would say don't worry rising rate risk is being managed.... The other difficult part was all I got was monthly reports, and be the moves between the 9 accounts I couldn't easily ascertain how bad it was, and I'm pretty good at figuring crap out. I knew we had lost some money, but didn't realize how much.

I'm moving the money, and parking in cash for at least 3 months to get my head straight, but will eventually go back into a managed account probably at fidelity. The reasons for needing the managed account is to show reasonable prudence as a trustee of my Uncle's assets while he is incapacitated.

|

|

|

|

|

12-10-2017, 08:16 AM

|

#15

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,345

|

Ugly. CD return with higher risk. What is your desired/target AA?

Quote:

Investment Performance Calculator

This calculator shows you how your portfolio is doing. Just give it your investment's beginning and ending balance for a given time period, and any additions and withdrawals (including dividends not kept in the account) along the way.

Inputs

| Starting Balance: | $1,000,000.00 | | Ending Balance: | $916,312.00 | | Months elapsed: | 36 | | Total Additions: | $0.00 | | Total Withdrawals & Dividends: | $139,568.00 |

Results

| Annualized Return Rate: | 1.96% |

|

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-10-2017, 08:49 AM

|

#16

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: May 2006

Location: west coast, hi there!

Posts: 8,809

|

This is a good example of a thread hijack. What do the recent posts have to do with bond fund dynamics like yield curve roll?

|

|

|

|

|

12-10-2017, 08:52 AM

|

#17

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Feb 2006

Location: Washington, DC

Posts: 11,327

|

Quote:

Originally Posted by Lsbcal

This is a good example of a thread hijack. What do the recent posts have to do with bond fund dynamics like yield curve roll?

|

+1 I was about to ask what does this FA stuff have to do with bonds funds.

__________________

Idleness is fatal only to the mediocre -- Albert Camus

|

|

|

|

|

12-10-2017, 09:16 AM

|

#18

|

|

gone traveling

Join Date: Dec 2016

Posts: 733

|

Didn't mean to hijack the thread. It was my comment to how rising rates directly resulted in a huge real loss, that prompted more questions about the specifics.

So even with "Professional Money Managers" mitigating the risks, the laws of economics still apply.

Sorry for  .

|

|

|

|

|

12-10-2017, 09:26 AM

|

#19

|

|

gone traveling

Join Date: Dec 2016

Posts: 733

|

Quote:

Originally Posted by pb4uski

Ugly. CD return with higher risk. What is your desired/target AA?

|

You got that right! Lots of risk not much return. Why I went to cash, despite advising against such a move by the adviser.

|

|

|

|

|

12-10-2017, 09:47 AM

|

#20

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2017

Location: City

Posts: 10,349

|

Quote:

Originally Posted by audreyh1

... gem of an article from Kitces ...

|

Thanks for this. Very educational as I am trying to learn more about bond funds.

But his conclusion:

"In the end, though, the bottom line is simply to recognize that the decision to purchase individual bonds that will be held until maturity, rather than using a bond fund that manages to a consistent duration, can actually result in inferior returns with an upward sloping yield curve ... "

is unproven I think, because he is implicitly assuming that the bond fund has no fees. I am also not sure that this is proven for all "upward sloping" yield curves, specifically those that are flatter than his examples.

Comments?

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|