pb4uski

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

12.58%.

AA is 60% equities (12% international, 48% domestic)/40% bonds

I'm content.

AA is 60% equities (12% international, 48% domestic)/40% bonds

I'm content.

Up 13.6%, allocation is 70/30

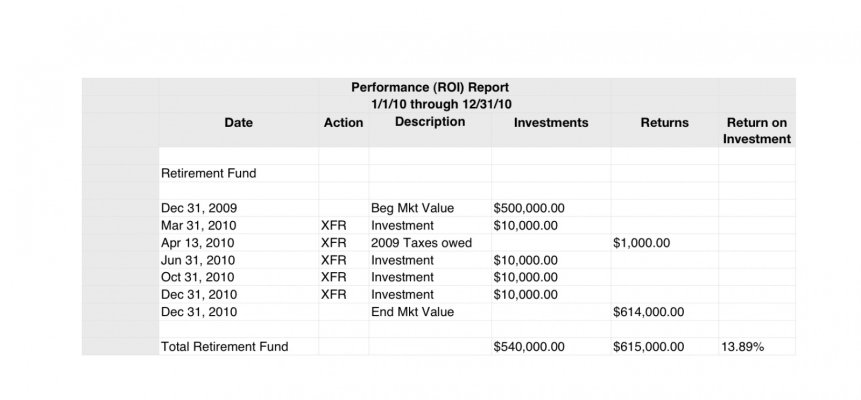

Since folks are using the formulas I posted, I thought I would go ahead and give you a full blown example that handles both withdrawals and additions during the year. Again - this is a rough approximation, but IMO a reasonable one.

So the total formula is basically

%ROI = [(starting value + additions during the year)/(final value + withdrawals during the year) - 1] x 100

Audrey

Oops! - sorry - I had the numerator and denominator inverted. I fixed it above. Thanks for catching it quickly while I could still edit.audrey,

are you sure this formula is correct? the final value was 1st in another formula now it is the starting value that is 1st. i plugged in some make believe numbers and i got a negative result when i expected a positive.

How important? If you are first starting out and your portfolio balance is small compared to your contributions - sure. But if your contributions and withdrawals are not large compared to the portfolio (a few percent), then their influence is small and this formula should be "good enough" for comparative purposes.But that formula doesn't take the timing of the investments/withdrawals into account, right? That can be very important, yes?

then their influence is small and this formula should be "good enough" for comparative purposes.

Well, let's not get too carried away with computing return to several digits.

I am now fretting that when the market opens again, it may just easily wipe out 1 percent of my stash in a single day. And then, like in the past, when an entire week's trading was down every single day, the pain was just unbearable.

But that formula doesn't take the timing of the investments/withdrawals into account, right? That can be very important, yes?

In any case, I must be doing something wrong, since I got 10.33% and my allocation started the year at 54% stock (ended at 58%). The stock stuff is in things like Total Stock and the bond stuff in Total Bond and GNMA. Why are you guys getting higher returns?