Alex in Virginia

Recycles dryer sheets

- Joined

- Dec 23, 2012

- Messages

- 145

Hello, alll...

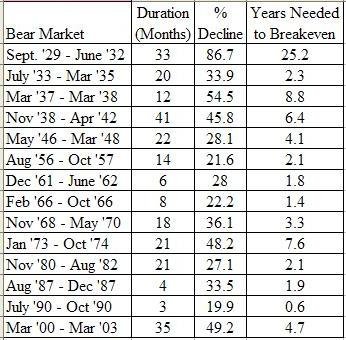

Can we agree that cashing out stocks at a loss in a bear market (or anytime?) to fund living expenses is not the best way to go? If we can agree, then how much cushion is enough cushion to get by a bear market without cashing in stocks?

I have set aside 3 years of living expenses in cash instruments (savings accounts & cds) and another 3 years in investment-grade (A-) bonds in a taxable account. The bonds are in a rolling ladder so that 1/3 each mature 4, 5 and 6 years from now (so that I can capture back the face value each year to cover those living expenses).

All of that I consider to be "separate" from my tax-deferred retirement funding portfolio.

Sound like enough? What is your bear market cushion like?

Thanks!

Alex in Virginia

Can we agree that cashing out stocks at a loss in a bear market (or anytime?) to fund living expenses is not the best way to go? If we can agree, then how much cushion is enough cushion to get by a bear market without cashing in stocks?

I have set aside 3 years of living expenses in cash instruments (savings accounts & cds) and another 3 years in investment-grade (A-) bonds in a taxable account. The bonds are in a rolling ladder so that 1/3 each mature 4, 5 and 6 years from now (so that I can capture back the face value each year to cover those living expenses).

All of that I consider to be "separate" from my tax-deferred retirement funding portfolio.

Sound like enough? What is your bear market cushion like?

Thanks!

Alex in Virginia

Last edited:

")