haha

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

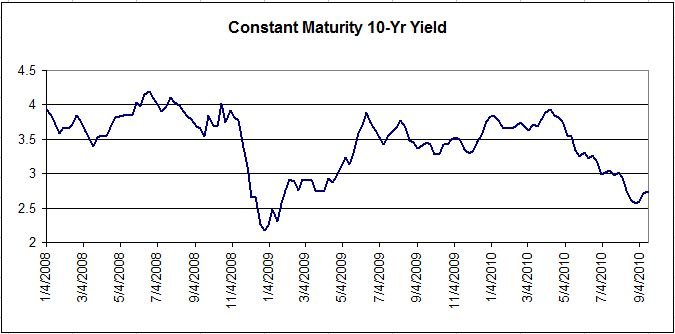

America’s Insolvency Is No Myth - - Krugman's Latest Pretense

By: Laurence Kotlikoff

I wish I were as sure of anything as Paul Krugman is of everything. But it’s his unfounded moral superiority that really goads.

In his July 2nd NY Times column, Myths of Austerity, Krugman writes “When I was young and naïve, I believed that important people took positions based on careful considerations of the options. Now I know better. Much of what Serious People believe rests on prejudice, not analysis.”

I agree with this last sentence, but I’d substitute “Paul Krugman” for “Serious People.”

What I and other economists expected, when Krugman was chosen to write for the Times, was impartial, fact-based analysis, showcasing economics’ ability to shed real light on critical issues of the day. We also expected him to act like a professional economist and represent fairly alternative policy positions before drawing his conclusion.

From my point of view . . . | ESPlanner Inc.

Ha

By: Laurence Kotlikoff

I wish I were as sure of anything as Paul Krugman is of everything. But it’s his unfounded moral superiority that really goads.

In his July 2nd NY Times column, Myths of Austerity, Krugman writes “When I was young and naïve, I believed that important people took positions based on careful considerations of the options. Now I know better. Much of what Serious People believe rests on prejudice, not analysis.”

I agree with this last sentence, but I’d substitute “Paul Krugman” for “Serious People.”

What I and other economists expected, when Krugman was chosen to write for the Times, was impartial, fact-based analysis, showcasing economics’ ability to shed real light on critical issues of the day. We also expected him to act like a professional economist and represent fairly alternative policy positions before drawing his conclusion.

From my point of view . . . | ESPlanner Inc.

Ha

")