Midpack

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

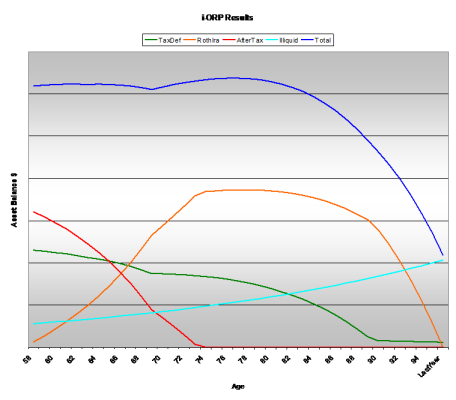

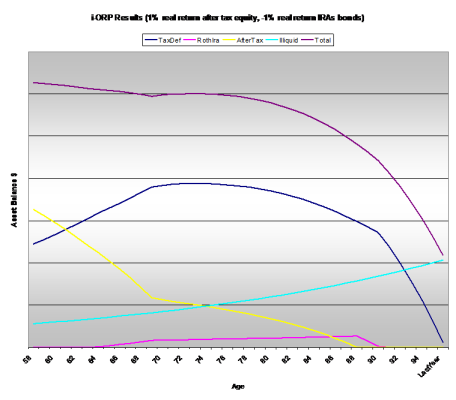

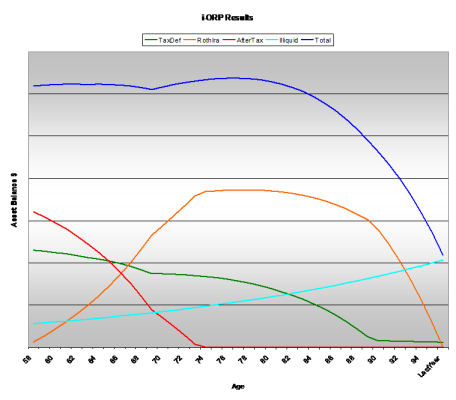

I'm trying to get my head around how to plan for minimizing taxes during withdrawal. I've run i-orp and while it's a little difficult to interpret the results (to me), I think I understand. In the spirit of second opinions, anyone know of another tax/withdrawal optimizer that can deal with taxable, tax deferred and Roth's (currently $0 for us), Soc Sec, etc.? I realize no one can predict future tax rates or investment (sequence of) returns.

Free/donation based is good, but paid apps would be fine if it's value added...

Free/donation based is good, but paid apps would be fine if it's value added...

), but presumably ORP concludes we'd be better off in the long run. So that's what I'll study next...

), but presumably ORP concludes we'd be better off in the long run. So that's what I'll study next...