|

|

12-08-2018, 12:46 PM

12-08-2018, 12:46 PM

|

#21

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2007

Posts: 3,229

|

Being just $100 over could cost some a lot more than just the extra $27 in taxes. I do ROTH conversions but try and take it as close as possible to the ACA MAGI limit without going over so that I get a subsidy. I've cut it real close the last couple years but could always recharacterized if needed, if I go $100 over this year it will cost me $10.5K.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

12-08-2018, 12:48 PM

|

#22

|

|

Recycles dryer sheets

Join Date: Jun 2018

Location: Delmarva

Posts: 221

|

Quote: Quote:

Originally Posted by pb4uski

Wanna bet on that?

Well you must have a bad version of TurboTax... I'm using the What-If worksheet in TurboTax 2017 but using 2018 rates... MFJ with $50,000 of LTCG and $51,200 of Roth conversions... total income is $101,200 and taxable income is $77,200 (top of 0% LTCG bracket)... tax is $2,886.

The 0% LTCG threshold is $77,200, not $77,400... $77,400 is the top of the 12% tax bracket.... but that error shouldn't make a difference in the analysis.

Now add $100 to Roth conversions... total income is $101,300 and taxable income is $77,300 and tax is $2,913... $27 more... just like I said.

I'm guessing that you added $1,000 of capital gains rather than $1,000 of Roth conversions... if that is what you did then you would get an additional $150 in tax... no increased ordinary tax and 15% on the increased LTCG.

|

Hmm, so if I don't get the answer you think, my TurboTax (current 2018 Premier, not a What-if on last year's version like you used) must be wrong.

OK, you're right about the $77,200 vs. $77,400 -- mea culpa. Though interestingly, TT showed no tax due at $77,400. And I didn't add $1,000 of capital gains, but rather a $1,000 tIRA withdrawal, as I said.

So ... I reran the sample return with your exact parameters (though I characterized as tIRA withdrawals, not Roth conversions, though that shouldn't make a difference). And the answer I got was ... $12. My guess (without sleuthing the calculations in the Qualified Dividend and Capital Gains worksheet) is that that the incremental amount ends up being taxed at either the LTCG or ordinary income rate, whichever is lower.

Congrats, you appear to have uncovered an error in last year's TurboTax what-if worksheet. Be sure to let them know.

All snarkiness aside, can't you see my point? Each dollar of taxable income is taxed at one rate or the other, never both (except when you get into NIIT, etc.).

__________________

"I can't complain, but sometimes I still do." - Joe Walsh, Life's Been Good

|

|

|

|

|

12-08-2018, 01:05 PM

|

#23

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2013

Location: Coronado

Posts: 3,707

|

Quote:

Originally Posted by Crabby Mike

OK, you're right about the $77,200 vs. $77,400 -- mea culpa. Though interestingly, TT showed no tax due at $77,400. And I didn't add $1,000 of capital gains, but rather a $1,000 tIRA withdrawal, as I said.

|

If you have $77.2K of LTCGs and $1K tIRA withdrawal, then it's correct that you owe no tax. If you file MFJ, you can go all the way up to $24K tIRA withdrawal in that scenario because you are just offsetting the standard deduction. Try putting in $24,100 of tIRA withdrawal and I think you'll see that you owe something like $27 in tax on that extra $100. (It might be off by a few cents because that amount will come from the tax tables instead of a calculation.)

|

|

|

|

12-08-2018, 01:07 PM

|

#24

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2012

Location: Texas

Posts: 3,024

|

Crabby, it's time to punt.

__________________

Retired at 52 in July 2013. On to better things...

AA: 85/15 WR: 2.7% SI: 2 pensions, SS later

|

|

|

|

|

12-08-2018, 01:08 PM

|

#25

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2002

Posts: 1,587

|

Quote:

Originally Posted by Crabby Mike

Hmm, so if I don't get the answer you think, my TurboTax (current 2018 Premier, not a What-if on last year's version like you used) must be wrong.

OK, you're right about the $77,200 vs. $77,400 -- mea culpa. Though interestingly, TT showed no tax due at $77,400. And I didn't add $1,000 of capital gains, but rather a $1,000 tIRA withdrawal, as I said.

So ... I reran the sample return with your exact parameters (though I characterized as tIRA withdrawals, not Roth conversions, though that shouldn't make a difference). And the answer I got was ... $12. My guess (without sleuthing the calculations in the Qualified Dividend and Capital Gains worksheet) is that that the incremental amount ends up being taxed at either the LTCG or ordinary income rate, whichever is lower.

Congrats, you appear to have uncovered an error in last year's TurboTax what-if worksheet. Be sure to let them know.

All snarkiness aside, can't you see my point? Each dollar of taxable income is taxed at one rate or the other, never both (except when you get into NIIT, etc.). |

Well, I don't know what your doing wrong with your test scenario, but I happened to just complete my 2018 tax year estimate with TurboTax, fully updated. So went in and added $1000 in interest income, and my tax liability went up exactly $270, just as I expected. It will increase at a 27% rate until such time as all CG/QDI is converted to the 15% rate and then any further increases will be at the 22% rate.

|

|

|

|

|

12-08-2018, 01:09 PM

|

#26

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,375

|

Quote:

Originally Posted by Crabby Mike

Hmm, so if I don't get the answer you think, my TurboTax (current 2018 Premier, not a What-if on last year's version like you used) must be wrong.

OK, you're right about the $77,200 vs. $77,400 -- mea culpa. Though interestingly, TT showed no tax due at $77,400. And I didn't add $1,000 of capital gains, but rather a $1,000 tIRA withdrawal, as I said.

So ... I reran the sample return with your exact parameters (though I characterized as tIRA withdrawals, not Roth conversions, though that shouldn't make a difference). And the answer I got was ... $12. My guess (without sleuthing the calculations in the Qualified Dividend and Capital Gains worksheet) is that that the incremental amount ends up being taxed at either the LTCG or ordinary income rate, whichever is lower.

Congrats, you appear to have uncovered an error in last year's TurboTax what-if worksheet. Be sure to let them know.

All snarkiness aside, can't you see my point? Each dollar of taxable income is taxed at one rate or the other, never both (except when you get into NIIT, etc.). |

Actually, I think it is more likely that I uncovered either an error in the 2018 TT software or an error that you made... probably the latter... and in this case it is taxed at both until all LTCG is pushed out of the 0% LTCG tax bracket.

Your point is wrong.... what happens is that the extra $100 of ordinary income is taxed at 12% and it also pushes $100 of LTCG from the 0% LTCG tax bracket to the 15% LTCG tax bracket... the total impact being 27%.

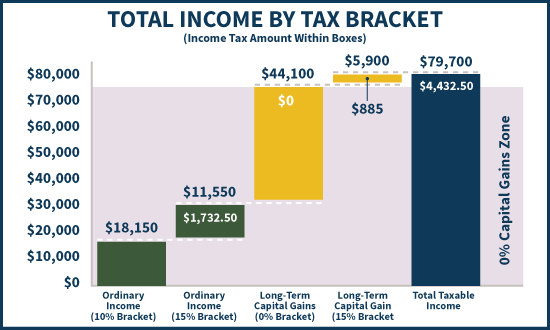

| | Base case | | | Base case + $100 | | | LTCG | 50,000 | | | 50,000 | | | Roth conversions | 51,200 | | | 51,300 | | | Deductions | -24,000 | | | -24,000 | | | Taxable income | 77,200 | | | 77,300 | | | | | | | | | | Ordinary income | | | | | | | 10% bracket | 19,050 | 1,905 | | 19,050 | 1,905 | | 12% bracket | 8,150 | 978 | | 8,250 | 990 | | Preferenced income | | | | | | | 0% bracket | 50,000 | 0 | | 49,900 | 0 | | 15% bracket | | 0 | | 100 | 15 | | Taxable income | 77,200 | 2,883 | | 77,300 | 2,910 | | | | | | | | | | | | | | 27 |

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-08-2018, 01:45 PM

|

#27

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2006

Location: Boise

Posts: 7,882

|

Can I join in the CrabbyMike guessing game?

My guess is that CrabbyMike is entering ~$77,400 of AGI (2018 Form 1040 Line 7), not taxable income (2018 Form 1040 Line 10).

__________________

"At times the world can seem an unfriendly and sinister place, but believe us when we say there is much more good in it than bad. All you have to do is look hard enough, and what might seem to be a series of unfortunate events, may in fact be the first steps of a journey." Violet Baudelaire.

|

|

|

|

|

12-08-2018, 01:56 PM

|

#28

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,375

|

Nah, I don't think that is what he is doing but I concede I don't understand how he is getting the results that he is getting.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-08-2018, 02:07 PM

|

#29

|

|

Recycles dryer sheets

Join Date: Jun 2018

Location: Delmarva

Posts: 221

|

Well, I can tell you that Crabby Mike is doing exactly what he says he's doing!

Hey folks, I'm prepared to be wrong here (I've had lots of practice), but I put in what I said and got the answer I got, and it makes logical sense to me for the reason I gave. I don't have time to dig further now, but will look at it later, and either eat crow or not. Aren't there any CPAs here that could explain it better? If not, I'll call mine on Monday.

__________________

"I can't complain, but sometimes I still do." - Joe Walsh, Life's Been Good

|

|

|

|

|

12-08-2018, 02:08 PM

|

#30

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2013

Location: Coronado

Posts: 3,707

|

So actually, there is a bug in TTax 2018 Premier. They have not yet implemented the Qualified Dividend/Capital Gains worksheet. In the attached screenshots, you can see that it still has the old text and the value that is entered on line 8 is incorrect. It should be $77,200, not $77,400.

The What-If worksheet in TTax 2017 is correct.

Page 41 of the draft IRS instructions for the new 1040 does have the draft of the new worksheet: https://www.irs.gov/pub/irs-dft/i1040gi--dft.pdf

|

|

|

|

|

12-08-2018, 03:20 PM

|

#31

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,375

|

Quote:

Originally Posted by Crabby Mike

.... Aren't there any CPAs here that could explain it better? If not, I'll call mine on Monday.

|

Yeah, I'll give you three guesses and the first two don't count.

To be fair though, while I am a retired CPA I was not a tax practitioner... I was on the consulting side. But call your on Monday and he will tell you that we are giving you the straight scoop since you obviously don't believe us. You can send him the table in post #26.

I hope that he doesn't charge you too much.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-08-2018, 03:27 PM

|

#32

|

|

Recycles dryer sheets

Join Date: Jun 2018

Location: Delmarva

Posts: 221

|

I believe Cathy63 found the answer to why pb4uski and I were getting different results with the same inputs. It looks like TurboTax does indeed have the wrong LTCG bracket in the worksheet (ignore the old numbers in the text, it's the $77,400 that's the problem). So in the narrow window between $77,200 and $77,400, TT is giving an incremental rate of 12% (because it mistakenly thinks there's no CG tax there}. Once you get beyond that error window, it does indeed produce a 27% rate.

While I still don't think that makes logical sense, I concede that it's how the tax code works. I should never have assumed that those two would go together!

Thanks to all for straightening me out (and hopefully TT will correct this error soon)!

__________________

"I can't complain, but sometimes I still do." - Joe Walsh, Life's Been Good

|

|

|

|

|

12-08-2018, 03:48 PM

|

#33

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,375

|

Crabby, this article may enhance your understanding... just keep in mind that the article is based on the old tax law, but the principles are the same. Pay particular attention to Example 3.

https://www.kitces.com/blog/understa...p-up-in-basis/

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

12-08-2018, 06:19 PM

|

#34

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

crabby, it made sense to me after I studied the QDiv/CG worksheet and played with different numbers, to see how new income that is taxed at 12% also pushes divs/CGs being taxed at 15%, for an effective 27% rate. The reason is, you don't get unlimited 0% divs/CGs. Once regular income + divs/CGs put you over that 77,x00 amount, they start getting taxed.

|

|

|

|

|

12-09-2018, 07:40 AM

|

#35

|

|

Thinks s/he gets paid by the post

Join Date: Jan 2006

Posts: 4,172

|

Quote:

Originally Posted by cathy63

So actually, there is a bug in TTax 2018 Premier. They have not yet implemented the Qualified Dividend/Capital Gains worksheet. In the attached screenshots, you can see that it still has the old text and the value that is entered on line 8 is incorrect. It should be $77,200, not $77,400.

The What-If worksheet in TTax 2017 is correct.

Page 41 of the draft IRS instructions for the new 1040 does have the draft of the new worksheet: https://www.irs.gov/pub/irs-dft/i1040gi--dft.pdf |

do you mean they haven't yet implemented the 2018 QDIV/CG wksht?

but they still have the 2017 wksht there , right? So what is the effect if that is the case? I would think you would be a little bit off but still closer to pb4uski's result. Remember this is CM's initial statement: " I added $1,000 IRA withdrawal (ordinary income), and the tax was $150. "

Adding 1,000 should have overwhelmed that small $200 in tax bracket error.

|

|

|

|

|

12-09-2018, 09:41 AM

|

#36

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2013

Location: Coronado

Posts: 3,707

|

Quote:

Originally Posted by kaneohe

do you mean they haven't yet implemented the 2018 QDIV/CG wksht?

but they still have the 2017 wksht there , right? So what is the effect if that is the case? I would think you would be a little bit off but still closer to pb4uski's result. Remember this is CM's initial statement: " I added $1,000 IRA withdrawal (ordinary income), and the tax was $150. "

Adding 1,000 should have overwhelmed that small $200 in tax bracket error.

|

I don't know what numbers Mike used in the original example as he just said it was a mix, but in his later test, he confirmed that he does see the 27% when he starts with income just above $77.4K. We'd have to see the original file to figure out exactly what went wrong. It might even have been something like having to use the Schedule D tax worksheet instead of the QDiv/CG worksheet, and I have no idea what shape that one is in.

Also, pb4uski's tax numbers from his spreadsheet are estimates, not exact values. He's calculating the tax owed with a formula, which is certainly the easiest way and makes the most sense for his purposes; but for ordinary income under $100K you have to use the tax tables on an actual return. TTax does use the tables, so it's numbers are not going to match the spreadsheet even outside this little $200 range. The exact tax owed in pb4uski's first example is $2880 ($3 less than the calc) and in the second example it's $2913 ($3 more than the calc).

|

|

|

|

|

12-09-2018, 08:49 PM

|

#37

|

|

Recycles dryer sheets

Join Date: Jun 2018

Location: Delmarva

Posts: 221

|

Well, I've moved on to other things, and didn't save the file, but I assume that the reason I was seeing 15% instead of 27% was TT's $200 error, since the next $100 that pb4uski was adding fell within that. I have since done an override to fix that value in my own estimates, at least until TT fixes it. I can't say why I got the same result when I added $1,000 though. I'm still playing with the QDIV/CG worksheet, and have set up a spreadsheet to mimic its calculations to facilitate that. As Cathy says, my formulas are a couple $$ off from the table values, but that doesn't bother me.

I was going to say that my excuse for not knowing about this issue was that my income has never been near the CG bracket boundaries, but I'm now wrestling with a similar situation nowhere near them. I won't hijack this thread, but I may start a new one if I can't sort it out on my own.

__________________

"I can't complain, but sometimes I still do." - Joe Walsh, Life's Been Good

|

|

|

|

|

12-11-2018, 01:20 PM

|

#38

|

|

Full time employment: Posting here.

Join Date: Jul 2013

Posts: 953

|

If a person is doing ROTH conversions, and needed to 'recharacterize', couldn't you just make a regular contribution to a tIRA? (So long as you are under 70). That contribution can be made early in 2019 and still apply to Tax Year 2018. You have to have earned income (which the Roth conversion creates), and be less than 70.

I might be missing something else. I assume that folks would not normally make a contribution to an IRA if they are also doing ROTH conversions, but I could be wrong.

__________________

Well it's all right, we're heading to the end of the line...

|

|

|

|

|

12-11-2018, 01:29 PM

|

#39

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Quote:

Originally Posted by Clone

If a person is doing ROTH conversions, and needed to 'recharacterize', couldn't you just make a regular contribution to a tIRA? (So long as you are under 70). That contribution can be made early in 2019 and still apply to Tax Year 2018. You have to have earned income (which the Roth conversion creates), and be less than 70.

I might be missing something else. I assume that folks would not normally make a contribution to an IRA if they are also doing ROTH conversions, but I could be wrong.

|

I don't think the part that I bolded is true. See https://www.irs.gov/credits-deductio.../earned-income

Without that, most of us don't have earned income to be able to make a contribution.

|

|

|

|

|

12-11-2018, 01:36 PM

|

#40

|

|

Full time employment: Posting here.

Join Date: Jul 2013

Posts: 953

|

OK, that makes sense. I was confused with the ACA income (which you can generate with IRA withdrawals or conversions) and earned income. My own tax situation continues to have earned income, such that we have the option of making a late IRA contribution. I do not need to manage to an income number, and so probably just need to sneak back into the shadows.

__________________

Well it's all right, we're heading to the end of the line...

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode