steelyman

Moderator Emeritus

Hmmm. I don't think saving and investing are mutually exclusive. ")

In summary:When I think of this more I realize that it isnt just the individuals who drank the mutual fund industry cool aide. All those state government and institutional pension funds are guilty too. Of course the states had issues with raiding and underfunding of the funds. What I'm arguing for is a greater emphasis of prudence and less on growth. Many on here have got that balance right, but we are the "1%" of the saving/investing world. Even with education it generally comes from vested interests who will sell yo on the need for growth and along with that a high fee fund.

steelyman said:Hmmm. I don't think saving and investing are mutually exclusive.

M Paquette said:The folks I run across that talk about how risky investing is don't seem to be saving much.

Or like the Wall Street financier who jumped out of his window: "So far so good!"Is that like Thelma & Louise saying "We haven't crashed (yet) because we're still in mid-air over the canyon"?

The only challenge will be finding an audience willing to sit still long enough to be educated. I wish I had the answer to that one too.When I am not travelling so much (or when I am finally retired) I plan to find a volunteer opportunity to educate people on financial basics.

The only challenge will be finding an audience willing to sit still long enough to be educated. I wish I had the answer to that one too.

That's an excellent group to work with-- already motivated and ready to listen.DW volunteers at an organization helping young single mothers make it by getting them schooled up on job skills, helping them create resumes, teaching them how to behave on a job interview, etc. They will be my first target to teach things like how to read a lease, how to balance a checking account, how to read a loan or credit card agreement and not get skinned, how to shop for a low cost/free checking account.

this is my point! Most people go to one extreme or the other, spending or playing the stock market. Very few see saving as something worthwhile and it certainly isn't promoted by many in the personal finance world. Saving should be promote far more.

Ads by Google

Merrill Edge® Trading Get 30 Free Online Stock or ETF Trades Per Month From Merrill Edge. www.MerrillEdge.com

The Top 3 MLP's to Buy The average MLP yields 9.3%. This Free report reveals the best. InvestingDaily.com/MLPs

Best Free Stock Widgets Realtime quotes & charts for your site or blog. Fully interactive! widgets.FreeStockCharts.com

Buy and Hold Not Working? Pension Partners uses a buy and rotate strategy to generate returns pensionpartners.com

Buy Stocks for $4 No Account or Investment Minimums. ING DIRECT Investing - $50 Bonus. www.sharebuilder.com/ingdirect

That's an excellent group to work with-- already motivated and ready to listen.

I've noticed that my daughter is all too willing to join in the "have a spending plan & invest the rest" part of the talk, but her eyeballs start to glaze over at the differences between "mutual fund vs ETF" or "global vs international". She just wants to put it away in some sort of suitable asset allocation, let it compound, and go live her life. I doubt we'll be dissecting McMillan's options textbook anytime soon.

At this age, with that temperament, she'll probably do better than my testosterone-poisoned stock-picking days.

The only thing that works or might work is owning equities long term. Putting money in a bank for other than an emergency money is a losers game.Merry Festivus........and now to the airing of grievances.

I was at a party last night and a friend complained that they'd lost 25% on some emerging markets EFT. I asked how it figured in their AA and the answer was basically "what's AA" and "a friend said EMs were the place to be because of the returns". Most people get sucked into chasing returns and it's a loosing game. So I want to praise all those who just SAVE and don't fall for the Wall Street hype and run after returns. We have lost the idea of just putting money aside, we now want big returns as well. Before we go looking for returns we should LBYM and just save! The mutual funds have all convinced us that they are the best place to put out money, but in many circumstances they should be actively avoided because of fees and poor performance.

OK I'm done back to the egg nog

this is my point! Most people go to one extreme or the other, spending or playing the stock market. Very few see saving as something worthwhile and it certainly isn't promoted by many in the personal finance world. Saving should be promote far more.

Right now pure saving is a losing game. The risk-free rate of return is near zero. Inflation is higher than that.

So you must either take some risk or watch your purchasing power erode.

If the spenders buy tangible things that they will need in the future, then they may actually come out better than the pure savers in this environment (I doubt that there are many spenders actually like this, though).

I've noticed that my daughter is all too willing to join in the "have a spending plan & invest the rest" part of the talk, but her eyeballs start to glaze over at the differences between "mutual fund vs ETF" or "global vs international".

this is my point! Most people go to one extreme or the other, spending or playing the stock market. Very few see saving as something worthwhile and it certainly isn't promoted by many in the personal finance world. Saving should be promote far more.

I wouldn't advocate just putting money in the bank. .... People should be looking at long term CDs....

Nords,

My daughter, home for Christmas, showed me here 401K options, a list of about 10 funds with two different investment groups and one MM-type fund. I asked her how she decided on the five she picked: highest return. That was it. I asked her what the expenses were in the funds...blank look. After looking at each fund, with simple links shown directly on her 401K company website, we found the expenses for each fund. Most of the funds she was in had an expense ratio north of 3.5% AND, ...wait for it... a 5.5% load, either A, B, or C. Since she is the person that communicates directly with the "financial advisor" for her company, I suggested that she do some one-on-one with this guy about what she and the others were really paying and why. They might get a break of fees, but she sure better find out. It turns out the FA is a son of someone the CEO knows.

Her biggest concern before I looked at it was that the NAV had mostly gone down since she jumped in. I told her at her age, 24, lower NAV was her friend, but expenses were her biggest enemy and to look into it.

I will say that I was pleased that she had made the decision to invest after pulling together her emergency cash fund. Free matching money from employer is immediate growth. Like your daughter, investment research is not high on her priorities list.

Well, here I am, coming into my final year before retiring and coming out of the closet as a self proclaimed saver. I won't ever put another dime in the stock market.

........I wish everyone the best of luck with their investments, but for me, without the aid of anyone who's able to advise me since they can't manage my work place 401K/457 accounts, I will leave the investing to you. I'll never be able to understand what it would take to make my own decisions, so at least I'm glad the Wells Fargo Stable Return fund is an option I can trust not to steal me blind or lead me over a cliff like some sort of lemming.

For example, what range of equity:bond:cash asset allocation are you recommending? From the start of this thread, it's seemed like an answer in search of a question, I've thought some specifics might help your case. If it makes you more comfortable, I'm at 52:39:9, though I expect to reduce my cash position over time.My intent in starting this thread was not to recommend a saving only approach, but that it should be a bigger part of most portfolios.

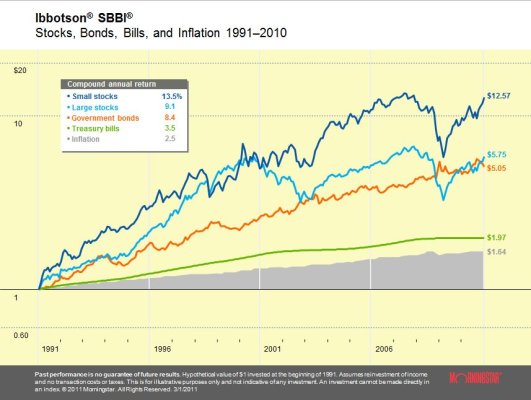

I am sure everyone here has seen this in some form or another. What the future might bring is unknown.

And it might be instructive to run FIRECALC with a 50:50 equity:bond asset allocation (or the default)

AND

then run the same scenario with a 100% cash allocation. [hold generated income constant, or adjust cash to hold probability of success constant].

The difference in income or probability of success will be markedly different.

In an age when reportedly most people don't/won't have enough to retire with a 60:40 AA, those who can realistically retire with 100% cash equivalents would have to be exceedingly rare.

I hope we're all successful whatever our investing approach.

For example, what range of equity:bond:cash asset allocation are you recommending? From the start of this thread, it's seemed like an answer in search of a question, I've thought some specifics might help your case. If it makes you more comfortable, I'm at 52:39:9, though I expect to reduce my cash position over time.

Is that equity:fixed-income:cash? We plan to reduce our cash position also as it is almost at 40%. Our YTD is pretty anemic because of the high cash position.I'm at 52:39:9, though I expect to reduce my cash position over time.

Fine, if long term history (ie chart above) is any indication that simply means you'll have to work much longer and/or accept much less income each year in retirement. You can quantify with FIRECALC. All part of the risk tolerance decision we each have to come to grips with...I'm not recommending any particular AA, just saying that saving is all too often ignored. After the "six month emergency fund" mantra it is completely left out of the equation. A fixed return component should be higher in everyone's thoughts when it comes to retirement savings.