|

|

12-30-2014, 01:29 PM

12-30-2014, 01:29 PM

|

#1

|

|

Gone but not forgotten

Join Date: Jul 2012

Location: Peru

Posts: 6,335

|

Inflation

The subject of inflation can be confusing when planning for the future. During the earning years, not as obvious as it can be during the retirement years.

Generally speaking, as prices go up, wages also rise.

Food for thought:

Inflation for $100 in these arbitrary 20 year brackets.

1930-1950 $144

1950-1970 $161

1970-1990 $337

1990-2010 $167

1994-2014 $159

Consider how that might affect retirement.

If... investment returns go up or lag the inflation rate.

If... pension or Social Security is inflation indexed or not.

In retrospect, our retirement in 1990 has seen relatively low inflation compared to someone who retired on fixed assets in 1970.

It would be interesting to see the average portfolio growth during the same periods.

The numbers are apropos of no theory or conclusion, but a picture of how different rates of inflation could affect a 20 year retirement... especially one that relies on fixed assets and conservative investing.

Here's a chart of the inflation rate by year. Note the high rates between 1974 and 1984.

http://www.multpl.com/inflation/table

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

12-30-2014, 01:40 PM

|

#2

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2014

Location: Williston, FL

Posts: 3,925

|

Great points.

I think one thing that might happen, and be almost catastrophic, is that wages go up via statutory minimum wage increases, but the CPI does not.

Without getting political, if the minimum wage is $15 per hour, plus additional benefits, it might make a small pension and investment withdrawal worth significantly less.

Let's say your total retirement income (pension, SS, investment withdrawal) is $30K a year. You would have the equivalent salary of a minimum wage worker with a $15 hr wage. And the lifestyle. Similar to having ~$16K in retirement income today, at $8 an hr.

If minimum wage increases do not impact the CPI, or prices, your spending would be the same, but you would be no better off than a minimum wage worker. Everyone's lifestyle increases, but yours goes down.

I am not sure if it could happen, but no one thought stagflation could happen either. Terrible economy, and raising prices. Maybe a deflationary environment could do it? Prices lower, CPI flat, and minimum wage workers making more.

__________________

FIRE no later than 7/5/2016 at 56 (done), securing '16 401K match (done), getting '15 401K match (done), LTI Bonus (done), Perf bonus (done), maxing out 401K (done), picking up 1,000 hours to get another year of pension (done), July 1st benefits (vacation day, healthcare) (done), July 4th holiday. 0 days left. (done) OFFICIALLY RETIRED 7/5/2016!!

|

|

|

|

|

12-30-2014, 10:09 PM

|

#3

|

|

Recycles dryer sheets

Join Date: Jan 2013

Posts: 73

|

Quote: Quote:

Originally Posted by Senator

[...]

Without getting political, if the minimum wage is $15 per hour, plus additional benefits, it might make a small pension and investment withdrawal worth significantly less.

[...]

If minimum wage increases do not impact the CPI, or prices, your spending would be the same, but you would be no better off than a minimum wage worker. Everyone's lifestyle increases, but yours goes down.[...]

|

There's a fallacy here, in my opinion.

You are absolutely correct in arguing that the hypothetical retiree would be no better off than a minimum wage earner, but given your premise that CPI doesn't change, that doesn't mean that the retiree is worse off than before the minimum wage increase.

Since the purchasing power of those $30,000 hasn't changed, the retiree can still purchase the same goods and services as before. The only way in which the retiree is worse off is when they compare themselves to others.

This seems to be a common failure - people pay (IMO) too much attention to what's happening to other people and lose sight of their own situation. Who cares if some CEO is making $100million in compensation this year - if I get my 5% raise, I'm still better off, even if I'm not making anywhere close to the CEO's salary.

The way in which the minimum-wage increase might negatively affect the retiree is precisely through inflation, I'd say. Raising a significant number of peoples' income could trigger inflation through two mechanisms: 1. By increasing the costs of minimum wage payers, forcing them to increase prices and 2. By increasing demand (through the minimum-wage earners that now earn more money) for goods/services faster than productivity increases, leading to price inflation.

Any CPI increase would represent a "headwind" the retiree's investment returns need to battle.

|

|

|

|

|

12-31-2014, 06:03 AM

|

#4

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2014

Location: Williston, FL

Posts: 3,925

|

Quote:

Originally Posted by ulrichw

You are absolutely correct in arguing that the hypothetical retiree would be no better off than a minimum wage earner, but given your premise that CPI doesn't change, that doesn't mean that the retiree is worse off than before the minimum wage increase.

|

I agree with your counter points, but what if you are living in a low cost of living area, and it becomes a high cost of living area? The COLA, which is based on a national cost of living analysis, doesn't change. Yet your expenses go up considerably more than the COLA.

So, the retirees 30K doesn't go near as far. Property taxes might have went up 20% (as mine have in the past), rents go up, etc.

So, a retiree could be all set financially one year, and slowly decline by 4-5%+ every year. Of course, they could move.

__________________

FIRE no later than 7/5/2016 at 56 (done), securing '16 401K match (done), getting '15 401K match (done), LTI Bonus (done), Perf bonus (done), maxing out 401K (done), picking up 1,000 hours to get another year of pension (done), July 1st benefits (vacation day, healthcare) (done), July 4th holiday. 0 days left. (done) OFFICIALLY RETIRED 7/5/2016!!

|

|

|

|

|

12-31-2014, 07:02 AM

|

#5

|

|

Moderator

Join Date: Feb 2010

Location: Flyover country

Posts: 25,357

|

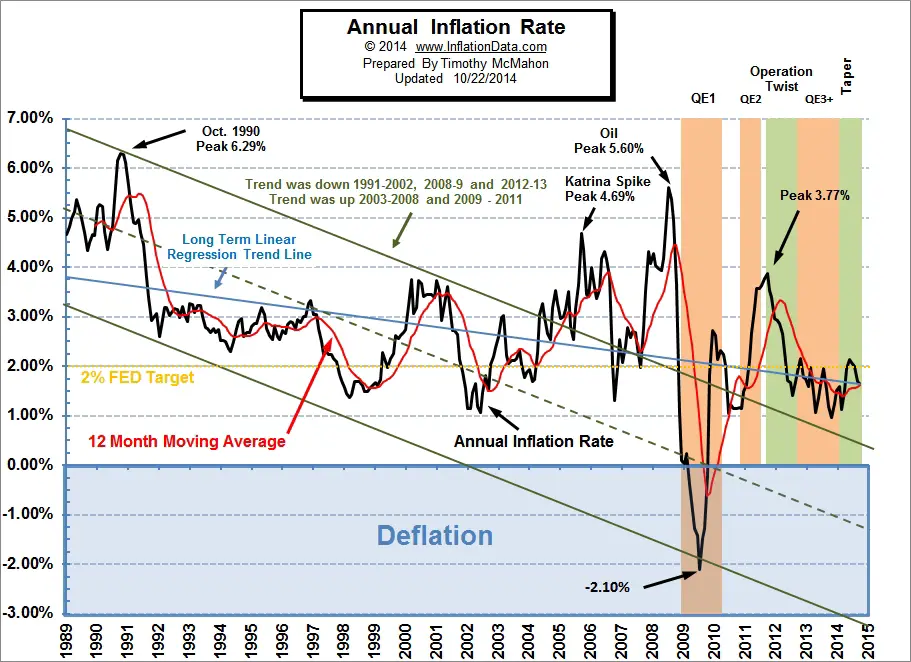

There is a nice chart here for the last quarter century:

Annual Inflation Rate Chart

|

|

|

|

|

12-31-2014, 07:09 AM

|

#6

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2014

Location: Williston, FL

Posts: 3,925

|

Quote:

Originally Posted by braumeister

There is a nice chart here for the last quarter century

|

No doubt, that is the national, i.e. macro, inflation. The concept of micro, or local inflation, is relatively undocumented.

Looking at the SF Bay area, one could see where people would be priced out of the market and have to move. The same with NYC.

I am not 100% sure how to protect yourself from this as a retiree, other than to have a shorter time period to retire in. That, by definition, is against most ER thoughts...

__________________

FIRE no later than 7/5/2016 at 56 (done), securing '16 401K match (done), getting '15 401K match (done), LTI Bonus (done), Perf bonus (done), maxing out 401K (done), picking up 1,000 hours to get another year of pension (done), July 1st benefits (vacation day, healthcare) (done), July 4th holiday. 0 days left. (done) OFFICIALLY RETIRED 7/5/2016!!

|

|

|

|

|

12-31-2014, 07:12 AM

|

#7

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2008

Location: NC

Posts: 21,303

|

Wouldn't it be more useful to look at real returns instead of inflation alone? There is some correlation between returns and inflation by definition.

Looks like real growth in stock prices have been reasonably reliable, and substantially more so on total return.

Frankly I care far more about real returns, than inflation alone.

The OP may actually be (re)making the case for every investor, including retirees, to keep some exposure to equities.

With the possible exception of very old retirees (like my 92 yo parents), those without at least 20-30% equity holdings are (far) more susceptible to portfolio failure due to inflation.

__________________

No one agrees with other people's opinions; they merely agree with their own opinions -- expressed by somebody else. Sydney Tremayne

Retired Jun 2011 at age 57

Target AA: 50% equity funds / 45% bonds / 5% cash

Target WR: Approx 1.5% Approx 20% SI (secure income, SS only)

|

|

|

|

12-31-2014, 07:32 AM

|

#8

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,143

|

Amazingly, considering cumulative inflation has been about 40% since we retired in 1999, our average annual spending has not increased with CPI, but rather stayed more of less the same.

Annual inflation for the 12 months ending in November 2014 was 1.32%. We are in one of the lowest ever inflation periods and its still trending down.

I only care that our investments keep up with inflation. So far so good, although for a while they were well behind. 2013 we finally caught back up with where we started in real terms.

__________________

Retired since summer 1999.

|

|

|

|

|

12-31-2014, 09:01 AM

|

#9

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2011

Posts: 8,417

|

A few years ago I found a chart (cannot find it now) on prices from the 1970 era. In general, most things cost about 4 times more than they did in 1970-74.

Exceptions were appliances (TVs have been $300 since the 50's) and clothes which seem to be cheaper now. Cars are a lot more expensive percentage-wise.

Salaries do not seem to follow the 4X observation. In 1970 a mid-level mechanical engineer would make $10K; now, I"m guessing its more like 10 times that.

__________________

Living well is the best revenge!

Retired @ 52 in 2005

|

|

|

|

|

12-31-2014, 09:03 AM

|

#10

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2011

Posts: 8,417

|

But don't equities provide a certain hedge against inflation? Don't they generally become more expensive (valuable) as inflation increases their price?

__________________

Living well is the best revenge!

Retired @ 52 in 2005

|

|

|

|

|

12-31-2014, 09:10 AM

|

#11

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,143

|

Quote:

Originally Posted by marko

But don't equities provide a certain hedge against inflation? Don't they generally become more expensive (valuable) as inflation increases their price?

|

Yes, for many of us that's the reason we invest in equities, in spite of their volatility.

__________________

Retired since summer 1999.

|

|

|

|

|

12-31-2014, 09:26 AM

|

#12

|

|

Moderator

Join Date: Feb 2010

Location: Flyover country

Posts: 25,357

|

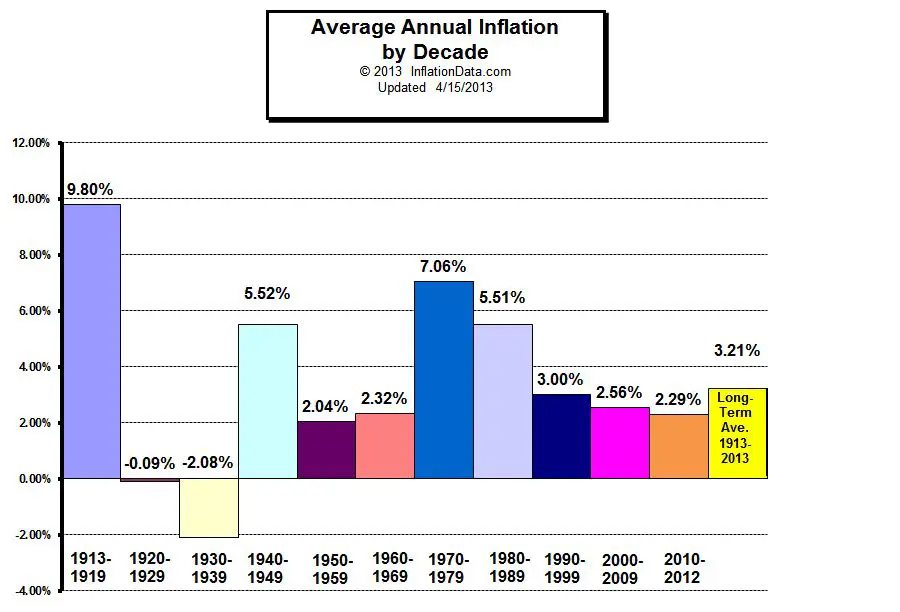

Another good chart that goes back farther:

|

|

|

|

|

12-31-2014, 01:27 PM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,143

|

Here is one that goes back even farther, but it's average annual inflation by decade.

__________________

Retired since summer 1999.

|

|

|

|

|

12-31-2014, 02:53 PM

|

#14

|

|

Gone but not forgotten

Join Date: Jul 2012

Location: Peru

Posts: 6,335

|

Quote:

Originally Posted by audreyh1

Here is one that goes back even farther, but it's average annual inflation by decade.

|

This is where the effect of inflation gets a bit complicated.

Looking at your chart, in the ten year period 1970-1979 = 7.06%.... from 1980 to 1989, 5.51%.

From the OP... that same period saw the buying power of $100 in 1970, rise to cost $337 during that same period.

Yes, of course, because of compounding. Would not investments made during that time also rise? Yes.

Our situation, our choice... was to stay ultra-conservative, with FDIC insured CD's, IBonds, and a fixed % income annuity. We are looking at a (likely) max of 10 more years, and could not afford a 2007-2009 market slide.

To put it in terms of real dollars... from a cost of living standpoint, and using the 1970-1990 inflation rate, the annual cost of living in 2014 of (example): $50,000/yr would rise to $168,500/yr in 2034.

This is not to argue that there is any real difference between the calculations in terms of the math, but that the circumstances used making a decision, should be considered.

And then, there is the human factor. A good friend who retired in 2008, saw his nest egg drop from $1.6 million to less than $800 thousand. Whilst he has since recovered, it is not an experience that he would want to repeat, and one that reaffirmed my own caution.

|

|

|

|

|

12-31-2014, 03:52 PM

|

#15

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2008

Location: Leeward Oahu

Posts: 17,914

|

I have very little faith in published inflation numbers. While I understand that there is some art as well as science in the determination, I also think it very much depends on what you buy and where you live. Then there are the "special" inflation numbers - you know, the ones where they take out food and fuel. What's up with that? (That's a rhetorical question, just in case...) My personal inflation level - on stuff I actually buy - has typically been much higher than any of the published indexes. I don't get to take advantage of the incredible slide in, for instance, electronics costs. But stuff I use every day (canned goods, for instance) have inflated locally as much as 50% in the past 5 years. I realize that's partly due to fuel costs for transportation.

I have several inflation strategies and back-ups in my bag of ER tricks. Still most trips to the store makes me wonder if they will be adequate to counter any serious inflation surge. I think such a surge will come - maybe not soon - but in my life expectancy of 20+ years. You can't print the tons of dollars we've been printing without eventually paying the price in inflation. Heard all the arguments about why that isn't happening (and even why it won't happen.) I just remember the shock of stagflation and it's frightening indeed for those of us without the ability to generate income. Still, I've got my back-ups to rely upon. Hope I don't need them and hope they are adequate if I do. YMMV

__________________

Ko'olau's Law -

Anything which can be used can be misused. Anything which can be misused will be.

|

|

|

|

|

01-01-2015, 04:33 AM

|

#16

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,191

|

Quote:

Originally Posted by audreyh1

Amazingly, considering cumulative inflation has been about 40% since we retired in 1999, our average annual spending has not increased with CPI, but rather stayed more of less the same.

Annual inflation for the 12 months ending in November 2014 was 1.32%. We are in one of the lowest ever inflation periods and its still trending down.

I only care that our investments keep up with inflation. So far so good, although for a while they were well behind. 2013 we finally caught back up with where we started in real terms.

|

you are spot on.

what folks forget is as we age spending tends to drop off big time once we get past the early doing and going stage of retirement.

spending falls off a cliff for most and does not ramp up alot until early 80's when healthcare,gifting and charitable giving tend to p/u.

that reduction offset so much in price increases that the reality was retirees tend to need alot less inflation protection then calculators plan for.

if you own a home or have a fixed rate mortgage you have even less inflation adjusting needed.

alot will depend on the amount of descretionary spending money you have. obviously if everything is a need there is little to have naturally cut back.

|

|

|

|

|

01-01-2015, 06:35 AM

|

#17

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2014

Location: Williston, FL

Posts: 3,925

|

Inflation will be a long time coming before it gets too high. A recent article highlights the strength of the US Dollar.

Since most of our goods are imported, the dollar strength will have a tendency to dampen price increases. Despite whatever money has been borrowed/printed by the US Treasury, our dollar has become even stronger. If you are an exporter, bad news. If you are an importer, which most Americans are, it is great news.

Hedging against inflation with hard assets (stocks, rental properties, Gold??, etc.) is one way. As long as inflation stays tame, and it appears it will do so for another year at least, look for the stock market to continue it's trip to the moon. Any quarter point increase by the Fed will not make any difference to the stock market returns. It may even make a case for deflation.

__________________

FIRE no later than 7/5/2016 at 56 (done), securing '16 401K match (done), getting '15 401K match (done), LTI Bonus (done), Perf bonus (done), maxing out 401K (done), picking up 1,000 hours to get another year of pension (done), July 1st benefits (vacation day, healthcare) (done), July 4th holiday. 0 days left. (done) OFFICIALLY RETIRED 7/5/2016!!

|

|

|

|

|

01-01-2015, 07:53 AM

|

#18

|

|

Moderator

Join Date: Oct 2010

Posts: 10,723

|

Quote:

Originally Posted by Koolau

I have very little faith in published inflation numbers. While I understand that there is some art as well as science in the determination, I also think it very much depends on what you buy and where you live. .....

|

Wouldn't it be cool if there were some kind of AI that would track what you, personally, spend your money on, long term, and give you a "personal inflation" value based on then things you have actually spend your money on? Those organizations that calculate the inflation figures make assumptions, like, if the price of beef goes up, you'll buy chicken. But what if you stick with beef? Your personal inflation would be higher than the general calculation. Maybe you burn a lot of gas, maybe very little. As more and more prices are posted online, there could be a "wayback machine" kind of price vacuum that saves prices. Then the user would enter their list of stuff they buy and the proportions spent on each, and it would be able to tell them what their personal inflation rate has been, historically. Then I can see edge cases where some people see huge inflation (a heavy user of things that shot up in price) and others that see no inflation or even deflation (a heavy user of things that get cheaper, like computing devices, electronics, etc).

|

|

|

|

|

01-01-2015, 08:14 AM

|

#19

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: May 2009

Posts: 9,343

|

Based on my memory which may be faulty, but the blips in inflation in my lifetime have been strongly correlated with the cost of a barrel of oil. I really cannot remember a time where inflation was above my worry line that oil wasn't involved with. Well, let's keep healthcare costs out of my generalization...

Sent from my iPad using Tapatalk

|

|

|

|

|

01-01-2015, 08:22 AM

|

#20

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2005

Posts: 6,191

|

housing and energy consume the biggest dollars of a median family income in theory and the cpi is weighted that way.

the cpi may be very different than your personal rate of inflation which involves specific products you personally buy , the cost , the increase ,how many times you buy them and the quality of those products. better quality products tend to see more inflation.

so now oil is low but for me healthcare costs are taking a major jump.

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|