|

|

11-22-2017, 01:03 PM

11-22-2017, 01:03 PM

|

#1

|

|

Thinks s/he gets paid by the post

Join Date: Dec 2016

Location: DC area

Posts: 2,496

|

Liquidating a 10-bagger

My very last individual stock is Lowes, which I bought 20 years ago at an average price of $7.85 per share, so my position is 90% capital gains and 10% principal  . 2018 will be my first full year of ER, and will be my first draw on my portfolio, so I'm trying to decide the best tax-efficient withdrawal strategy from my taxable accounts. I think selling Lowes is it - it alone will essentially fund my year's spending requirements.

My taxable accounts look like:

11% Lowes with 90% CGs

54% Large Cap Vanguard MFs with 50% CGs (PRIMECAP and Tax Managed Cap Appreciation)

21% Tilt Vanguard MFs with ~17% CGs (Emerging Markets and Small Value)

14% I-bonds (emergency fund)

Other background and considerations:

- Short to medium term I intend to sell off the large cap MFs, taking advantage of the 50% return of principal to lower AGI/MAGI to qualify for ACA subsidies and headspace for Roth conversions.

- But, for 2018 I'm staying on COBRA, it is a better plan and cheaper than unsubsidized ACA, so I have a window for a high MAGI next year.

- I plan to sell early next year, hopefully most all of it will be in the 0% CG bracket, if I sell this year it will all be in the 15% bracket (and may cause some other unpleasant tax phase-outs).

- I don't have any losing positions in my taxable accounts, so no offsetting capital losses (used those up last year).

- I might get some consulting work next year that could push some of the CGs to 15% bracket (and also affect ACA subsidies), but I can't complain too much about more money.

- My AA is 55/45, and I'm planning age-in-equities from there (that's a whole 'nother discussion). About 75% of my portfolio is in tax advantaged accounts, so I can rebalance there as needed to offset taxable stock sales.

This is all a change from where I was a month ago, planning to sell some of the 50% CG MFs (maybe even this year) and try for ACA subsidy. But the potential for consulting income and quality of the COBRA plan (though expensive) changed that.

My question is, am I missing anything that should impact this decision?

__________________

FI and Semi-ER March 24, 2017

Consulting to stay engaged

"All models are wrong, some are useful." - George Box

There is always a well-known solution to every human problem: neat, plausible, and wrong. - H.L. Mencken

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

11-22-2017, 01:39 PM

|

#2

|

|

Thinks s/he gets paid by the post

Join Date: May 2005

Location: Portland

Posts: 1,713

|

Nothing to add to help. Just an observation into my mind. When you are saying MF I am thinking about something other than mutual funds

Too much time around construction guys

|

|

|

|

|

11-22-2017, 01:44 PM

|

#3

|

|

Full time employment: Posting here.

Join Date: Feb 2011

Posts: 852

|

If you plan to do any charitable giving, giving them shares of Lowe's instead of money would be advantageous to you.

|

|

|

|

|

11-22-2017, 01:57 PM

|

#4

|

|

Thinks s/he gets paid by the post

Join Date: Dec 2016

Location: DC area

Posts: 2,496

|

Quote: Quote:

Originally Posted by Scrapr

Nothing to add to help. Just an observation into my mind. When you are saying MF I am thinking about something other than mutual funds

Too much time around construction guys

|

Ha! 33 years here in the construction industry. Didn't catch that cause those guys only talk, not write...

__________________

FI and Semi-ER March 24, 2017

Consulting to stay engaged

"All models are wrong, some are useful." - George Box

There is always a well-known solution to every human problem: neat, plausible, and wrong. - H.L. Mencken

|

|

|

|

|

11-22-2017, 02:24 PM

|

#5

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,896

|

Just be careful to not so sell much that those gains put you above the 15% bracket. Though the gains aren't taxable up that point, they do count as income for determining your tax bracket (I think they get zeroed out after the taxable income line).

-ERD50

|

|

|

|

|

11-22-2017, 02:39 PM

|

#6

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Quote:

Originally Posted by ERD50

Just be careful to not so sell much that those gains put you above the 15% bracket. Though the gains aren't taxable up that point, they do count as income for determining your tax bracket (I think they get zeroed out after the taxable income line).

-ERD50

|

That sounds pretty misleading. The first sentence is correct. But CGs don't count in determining your tax bracket. They cannot push regular income into jumping out of 15% into being taxed at 25%, which is what it sounds like you are saying.

What it is, when income + Qdivs +LTCGs exceed a certain number, which today happens to be the top of the 15% bracket (bottom of 25% bracket), any Qdivs and LTCGs over that get taxed at 15%. In the new tax proposal, I'm pretty sure that barrier is actually different from the top of the new 12% bracket (bottom of 25% bracket). So adding CGs really has nothing to do with the brackets themselves, it's that number at which when combined with the other income, they start being taxed.

I have no idea what you mean about that comment about them getting zeroed out after the taxable income line.

|

|

|

|

|

11-22-2017, 02:46 PM

|

#7

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2014

Location: The Great Wide Open

Posts: 3,804

|

Another thing is to capture capital gains under the 15% bracket. You can immediately repurchase any security to lock in a gain at the 15% level, then start the process all over again. You may end up with a losing position with the new position, but you were still up over the long term, which you may use to offset later. Also, if the second purchase continues to increase, the latest gain would be less painful on future tax returns.

|

|

|

|

|

11-22-2017, 03:03 PM

|

#8

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,896

|

Quote:

Originally Posted by RunningBum

That sounds pretty misleading. The first sentence is correct. But CGs don't count in determining your tax bracket. They cannot push regular income into jumping out of 15% into being taxed at 25%, which is what it sounds like you are saying.

What it is, when income + Qdivs +LTCGs exceed a certain number, which today happens to be the top of the 15% bracket (bottom of 25% bracket), any Qdivs and LTCGs over that get taxed at 15%. In the new tax proposal, I'm pretty sure that barrier is actually different from the top of the new 12% bracket (bottom of 25% bracket). So adding CGs really has nothing to do with the brackets themselves, it's that number at which when combined with the other income, they start being taxed.

I have no idea what you mean about that comment about them getting zeroed out after the taxable income line.

|

I'll need to plug some numbers in a tax program to validate what I wrote, maybe some of that is misleading/wrong, but I think the main point is valid - if you sell too much, and create too much LTCG, the gains will be taxed at 15% rather than zero.

I thought it also pushed up other income as well, but I'll check on that later.

So you are saying that if top of the 15% bracket was $75,000, and you had $50K LTCG and another $60K income, that none of that $60K income would be taxed above 15%? I was thinking that $35K ($60K+$50K-$75K) would be in the 25% bracket.

-ERD50

|

|

|

|

|

11-22-2017, 03:03 PM

|

#9

|

|

Thinks s/he gets paid by the post

Join Date: Dec 2016

Location: DC area

Posts: 2,496

|

Quote:

Originally Posted by ERD50

Just be careful to not so sell much that those gains put you above the 15% bracket. Though the gains aren't taxable up that point, they do count as income for determining your tax bracket (I think they get zeroed out after the taxable income line).

-ERD50

|

To you and RunningBum - on my to do list is to better understand the interactions of high CGs with ordinary income in the tax code. While working the CGs were always minor compared to W-2 income, so they were what they were.

__________________

FI and Semi-ER March 24, 2017

Consulting to stay engaged

"All models are wrong, some are useful." - George Box

There is always a well-known solution to every human problem: neat, plausible, and wrong. - H.L. Mencken

|

|

|

|

|

11-22-2017, 03:07 PM

|

#10

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,376

|

Quote:

Originally Posted by ERD50

I'll need to plug some numbers in a tax program to validate what I wrote, maybe some of that is misleading/wrong, but I think the main point is valid - if you sell too much, and create too much LTCG, the gains will be taxed at 15% rather than zero.

I thought it also pushed up other income as well, but I'll check on that later.

So you are saying that if top of the 15% bracket was $75,000, and you had $50K LTCG and another $60K income, that none of that $60K income would be taxed above 15%? I was thinking that $35K ($60K+$50K-$75K) would be in the 25% bracket.

-ERD50

|

No.

If the top of the 15% tax bracket was $75k and you had $50k LTCG and $60k of ordinary income, the $60k of ordinary income would be taxed as if you had no other income... then the first $15k of LTCG would be at 0% (up to a total income of $75k) and the remaining $35k of LTCG would be at 15%.

I'm assuming that deductions and exemptions are already applied in the $60k for simplicity.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

11-22-2017, 03:09 PM

|

#11

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Quote:

Originally Posted by ERD50

I'll need to plug some numbers in a tax program to validate what I wrote, maybe some of that is misleading/wrong, but I think the main point is valid - if you sell too much, and create too much LTCG, the gains will be taxed at 15% rather than zero.

I thought it also pushed up other income as well, but I'll check on that later.

So you are saying that if top of the 15% bracket was $75,000, and you had $50K LTCG and another $60K income, that none of that $60K income would be taxed above 15%? I was thinking that $35K ($60K+$50K-$75K) would be in the 25% bracket.

-ERD50

|

Assuming we are ignoring deductions and exemptions for simplicity.

None of that 60K would be taxed above 15%. 15K of the CGs would be at 0%, and 35K would be taxed at 15%.

|

|

|

|

|

11-22-2017, 03:12 PM

|

#12

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Quote:

Originally Posted by USGrant1962

To you and RunningBum - on my to do list is to better understand the interactions of high CGs with ordinary income in the tax code. While working the CGs were always minor compared to W-2 income, so they were what they were.

|

What I did to understand it was to run different scenarios through Turbo Tax, and look at how it affected the Qualified Dividends and Capital Gains Worksheet, which is what you actually use to calculate taxes when you have divs and CGs. Warning, it's confusing, because it's pretty busy and some people do better with a graphic I've seen, but can't put my hands on right now. Maybe someone else can find it and show it.

|

|

|

|

|

11-22-2017, 03:14 PM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,376

|

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

11-22-2017, 03:22 PM

|

#14

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

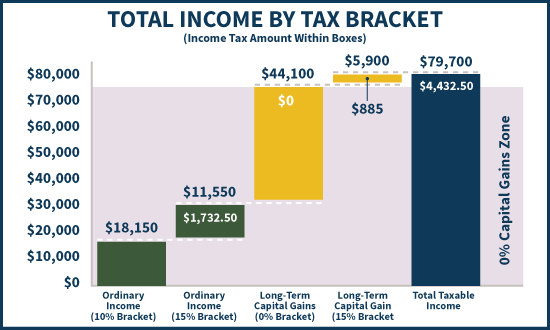

Right. As the green regular income box grows, it pushes more of the yellow LTCGs and QDivs box into being taxed at 15%. Once the green box fills and overflows the 15% bracket, all LTCGs and QDivs are taxed at 15% (or higher if you get way up there in income).

|

|

|

|

|

11-22-2017, 04:49 PM

|

#15

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,896

|

OK, so I plugged it a tax estimator:

www.hrblock.com/tax-calculator/

For MFJ, top of 15% bracket is $96,700 ($75,900 Taxable Income after subtract $12,700 Standard Deduction and $8,100 Pers Exempt). "Income " below is regular earned income type.

$96,700 Income = $10,453 taxes (FYI - a 10.81% effective rate)

Add $10K of income and the added $10K is taxed at the 25% marginal rate as expected.

With $96,700 Income and an added $10K LTCG, the added $10K is taxed at the 15% LTCG rate. OK.

$96.7K of LTCG with $0 income is taxed at 0% and $0.

Add $10K of income and the $10K delta is taxed at 15% marginal rate (so it's 'really' $10K of the LTCG being taxed, even though the increase was from 'income').

I see the numbers, it's still a little tricky for me to consolidate each scenario into words, but I think the key is that if you have regular income at the top of the 15% bracket, added LTCG do not "push" the income into the 25% bracket, it is the LTCG which get "pushed" from 0% to 15% bracket. Whew, did I get that expressed correctly?

-ERD50

|

|

|

|

|

11-22-2017, 04:57 PM

|

#16

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,228

|

Yes, I think you've got it.

Note that if you had 1/2 regular income and 1/2 LTCG (out of 96.7K), and added $10K of income, you should see a 30% increase in tax. That's because you're taxed 15% on that extra $10K of income, plus you've pushed $10K of LTCGs into being taxed at 15%.

|

|

|

|

|

11-22-2017, 05:43 PM

|

#17

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,376

|

Exactly.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

11-22-2017, 06:30 PM

|

#18

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,896

|

Quote:

Originally Posted by RunningBum

Yes, I think you've got it.

Note that if you had 1/2 regular income and 1/2 LTCG (out of 96.7K), and added $10K of income, you should see a 30% increase in tax. That's because you're taxed 15% on that extra $10K of income, plus you've pushed $10K of LTCGs into being taxed at 15%.

|

Thanks, and yes, I actually did see that 30% rate when I was playing different scenarios. I think there might be a bigger push for tax reform if the average person understood just how wacky taxes are, but people don't "see" this stuff. Just plug in numbers, or pay someone, and it spits out a number. But once you make something complex, and then add complexities on top, it all becomes geometrically complex - like figuring t-IRA versus ROTH, ROTH conversions, 0% LTCG, etc, etc.

-ERD50

|

|

|

|

|

11-22-2017, 08:00 PM

|

#19

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2006

Location: Rio Grande Valley

Posts: 38,153

|

Quote:

Originally Posted by ERD50

I thought it also pushed up other income as well, but I'll check on that later.

So you are saying that if top of the 15% bracket was $75,000, and you had $50K LTCG and another $60K income, that none of that $60K income would be taxed above 15%? I was thinking that $35K ($60K+$50K-$75K) would be in the 25% bracket.

-ERD50

|

No. Ordinary income and long term capital gains are split apart and taxed separately except for the threshold on 0% cap gains. In your example (ignoring deductions, exemptions etc. and current tax brackets which are a bit higher), $60K of the ordinary income is taxed at 15%, $15K of capital gains is taxed at 0%, $35K of cap gains is taxed at 15%.

__________________

Retired since summer 1999.

|

|

|

|

|

11-22-2017, 09:54 PM

|

#20

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,376

|

Quote:

Originally Posted by audreyh1

No. Ordinary income and long term capital gains are split apart and taxed separately except for the threshold on 0% cap gains. In your example (ignoring deductions, exemptions etc. and current tax brackets which are a bit higher), $60K of the ordinary income is taxed at 15%, $15K of capital gains is taxed at 0%, $35K of cap gains is taxed at 15%.

|

I'll add one refinement... the first $18,550 of ordinary income would be taxed at 10% and then the remainder at 15%.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode