|

|

Market high: scary time to retire?

03-05-2013, 09:10 AM

03-05-2013, 09:10 AM

|

#1

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2012

Posts: 11,702

|

Market high: scary time to retire?

So w*rk is bogus, and I'm itchy. Everything says I can retire today. Then I look at my net worth and realize between savings and market return, I've had 50% appreciation in the last 4 years.

That's good. And that's scary.

I think it is leading to my OMY syndrome. If I can see 50% up in 4 years which crossed me over from non-FI into FI, who says I can't see 30% down in 4 years dropping me back to near non-FI scary-land.

This good market is playing games with my head.

I know some folks here retired in 2008, and it has worked out for them. Yet... Well... I don't know. This volatility and potential volatility is driving me insane.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

03-05-2013, 09:15 AM

|

#2

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2007

Posts: 7,746

|

It would bother me too, knowing that I retired into a market that has been on fire lately. Your 30% drop scenario is certainly a possibility and not that unlikely given historical drops (2 years of 16% drops each year would get you to a net 30% loss in the market).

The bright side is that Warren Buffet says equities are still a good place to put your money today for long term growth. He's about the only guy that I listen to when it comes to Mr. Market. Partly because he makes macro statements, not stock picking market timing statements.

__________________

Retired in 2013 at age 33. Keeping busy reading, blogging, relaxing, gaming, and enjoying the outdoors with my wife and 3 kids (8, 13, and 15).

|

|

|

|

|

03-05-2013, 09:17 AM

|

#3

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Oct 2005

Location: North Oregon Coast

Posts: 16,483

|

As long as the disconnect between the fortunes of Wall Street and Main Street can be sustained, equities will be fine. The market feels less and less a proxy for the U.S. economy for Middle America and more and more a proxy of overall global trends.

__________________

"Hey, for every ten dollars, that's another hour that I have to be in the work place. That's an hour of my life. And my life is a very finite thing. I have only 'x' number of hours left before I'm dead. So how do I want to use these hours of my life? Do I want to use them just spending it on more crap and more stuff, or do I want to start getting a handle on it and using my life more intelligently?" -- Joe Dominguez (1938 - 1997)

|

|

|

|

|

03-05-2013, 09:22 AM

|

#4

|

|

Recycles dryer sheets

Join Date: Jan 2013

Posts: 194

|

Since the market is pushing up against highs, why not sell enough stock to finance several years of retirement, so you can ride out any fall? After all, once you done what is necessary to win, why put the win at risk?

Check out something called the bucket system. I don't fully subscribe to it, but the general idea of having a bucket of safe money one can use to ride out a drop in the market is a good one.

|

|

|

|

|

03-05-2013, 09:22 AM

|

#5

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2005

Location: Crownsville

Posts: 3,746

|

I think I'd be afraid to retire right now, as well, if the recent run-up had just barely pushed me to the FI/RE threshold. Now, what you might want to do, is cash out a little profit at this point and set it aside. If the market keeps on bounding, re-assess your situation then, and see if you'd still be comfortable retiring. Or, if it falls off from here, take some of that cash and buy back in, when prices fall.

|

|

|

|

|

03-05-2013, 09:23 AM

|

#6

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2008

Location: NC

Posts: 21,303

|

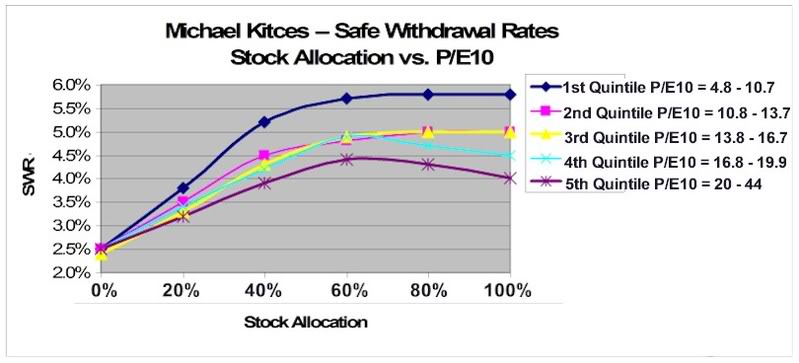

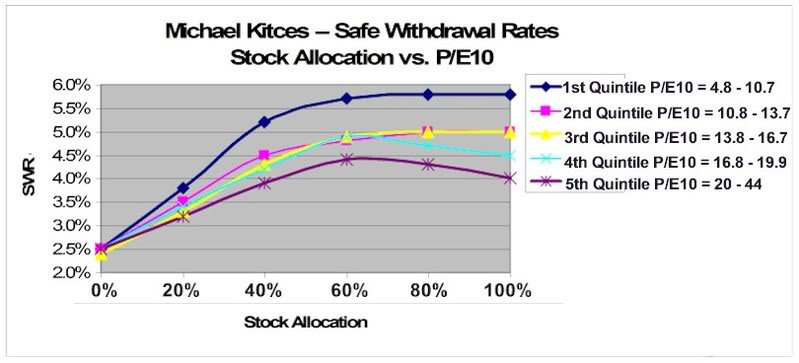

Of course most SWR studies (including FIRECALC) include market returns back to 1871 or at least 1929, which covers the Great Depression, two World Wars, dozens of recessions and several significant geopolitical events.

And right or wrong, many of us (self included) weren't/aren't comfortable pulling the retirement trigger until our success rate appears to be 100%, 150% or even as much as 200% (nest egg 2X the 100% success rate). It's your retirement...

But that said, some people like to look at PE10 when they retire and modify their WR's accordingly. It might make you feel better, and there is some logic to it...

Here's an old thread on the subject, the methology hasn't changed. http://www.early-retirement.org/foru...swr-38485.html

__________________

No one agrees with other people's opinions; they merely agree with their own opinions -- expressed by somebody else. Sydney Tremayne

Retired Jun 2011 at age 57

Target AA: 50% equity funds / 45% bonds / 5% cash

Target WR: Approx 1.5% Approx 20% SI (secure income, SS only)

|

|

|

|

|

03-05-2013, 09:24 AM

|

#7

|

|

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

Join Date: Jun 2002

Location: Texas: No Country for Old Men

Posts: 50,021

|

If you wait OMY and the market has a big downturn, will that make you feel better about pulling the plug? You could then wait for the market to recover, but wouldn't that put you right back where you are today?

__________________

Numbers is hard

|

|

|

|

|

03-05-2013, 09:25 AM

|

#8

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Feb 2013

Posts: 9,358

|

Could you afford to retire without counting on stock market returns? My retirement budget is based on living on SS and pensions and having enough money in the bank now to cover the bridge years. I just can't afford to lose a lot of money. I don't really have to make any additional money.

We have just made financial security and not having to have 8 - 5 jobs our main priority. We just cut back our lifestyle to make the numbers work without depending on any future stock market gains, including downsizing the house and moving to a lower cost of living area.

|

|

|

|

|

03-05-2013, 09:29 AM

|

#9

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2005

Location: Chicago

Posts: 13,186

|

Think about the sustainability of your income steam more than the absolute value of your assets.

I last worked in mid-2006. That gave me a couple of years to feel all "comfy" and secure with a retirement lifestyle before the crash. Then the sh*t hit the fan with the value of my assets falling over 30%. But my income stream dropped much less, more like 10% - 15%, so the party continued with only minor adjustments. A few years with a bit of stress and hand wringing later, the asset value more than recovered.

If you're going to be heavily dependent on cashing in assets for day to day living, I'd be concerned. If you look at your income stream and see that it will drop substantially less, as a percentage, than the equity market, grit your teeth and plow ahead!

Time is flying by!

__________________

"I wasn't born blue blood. I was born blue-collar." John Wort Hannam

|

|

|

|

|

03-05-2013, 09:30 AM

|

#10

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Oct 2005

Location: North Oregon Coast

Posts: 16,483

|

Quote: Quote:

Originally Posted by Midpack

|

Interestingly, it shows that regardless of valuation, a 60/40 AA (or about 65/35 here, I think) is just about the most "survivable" upon retirement. It certainly doesn't produce the largest *expected* nest egg when we kick the bucket, but that's a separate calculation (and motivation) from simply trying to avoid outliving your money.

__________________

"Hey, for every ten dollars, that's another hour that I have to be in the work place. That's an hour of my life. And my life is a very finite thing. I have only 'x' number of hours left before I'm dead. So how do I want to use these hours of my life? Do I want to use them just spending it on more crap and more stuff, or do I want to start getting a handle on it and using my life more intelligently?" -- Joe Dominguez (1938 - 1997)

|

|

|

|

|

03-05-2013, 09:33 AM

|

#11

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2012

Posts: 11,702

|

Quote:

Originally Posted by Andre1969

Now, what you might want to do, is cash out a little profit at this point and set it aside. If the market keeps on bounding, re-assess your situation then, and see if you'd still be comfortable retiring. Or, if it falls off from here, take some of that cash and buy back in, when prices fall.

|

Here's some irony. I was too heavily weighted in cash. (Duh-oh! Missed the market run up!) The market has actually brought my portfolio into more of the balance I want with equities. I still have a lot of cash, I don't want to generate any more.

Quote:

Originally Posted by REWahoo

If you wait OMY and the market has a big downturn, will that make you feel better about pulling the plug? You could then wait for the market to recover, but wouldn't that put you right back where you are today?

|

Good point.

|

|

|

|

|

03-05-2013, 09:34 AM

|

#12

|

|

Recycles dryer sheets

Join Date: Jan 2013

Posts: 194

|

Quote:

Originally Posted by Midpack

And right or wrong, many of us (self included) weren't/aren't comfortable pulling the retirement trigger until our success rate appears to be 100%, 150% or even as much as 200% (nest egg 2X the 100% success rate). It's your retirement...

|

If my investments were financing all or most of my retirement, I would agree with this. If I had other retirement assets such as a pension or a decently high SS payout, I think 90% certainty would be good enough. 100% certainty is not possible in reality, since we don't know that the assumptions we make using FireCalc are going to hold for 30+ years. In other words, stay flexible, observe and adjust.

In the end, do whatever allows you to sleep at night.

|

|

|

|

|

03-05-2013, 09:37 AM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2012

Posts: 11,702

|

Quote:

Originally Posted by ziggy29

Interestingly, it shows that regardless of valuation, a 60/40 AA (or about 65/35 here, I think) is just about the most "survivable" upon retirement. It certainly doesn't produce the largest *expected* nest egg when we kick the bucket, but that's a separate calculation (and motivation) from simply trying to avoid outliving your money.

|

I was at 40% equities a few years ago when I started thinking about this.

The market has gotten my over 50% along with investing savings primarily in equities during that time.

I'm using DAV strategies right now to push it to 60% or so. A market drop would actually mean buying more equities with DAV strategy.

I guess I just have to keep the faith and stay the course.

|

|

|

|

|

03-05-2013, 09:39 AM

|

#14

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2012

Posts: 11,702

|

Quote:

Originally Posted by Stanley

If my investments were financing all or most of my retirement, I would agree with this. If I had other retirement assets such as a pension or a decently high SS payout, I think 90% certainty would be good enough. 100% certainty is not possible in reality, since we don't know that the assumptions we make using FireCalc are going to hold for 30+ years. In other words, stay flexible, observe and adjust.

In the end, do whatever allows you to sleep at night.

|

Well, no pension. And I have to pay for H.I. Those provide ways to not sleep.

Then this morning on Squawk Box, the panel was making all sorts of noise about how we need to reduce SS benefits. More lack of sleep ahead.

|

|

|

|

|

03-05-2013, 09:44 AM

|

#15

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Oct 2005

Location: North Oregon Coast

Posts: 16,483

|

Quote:

Originally Posted by JoeWras

Then this morning on Squawk Box, the panel was making all sorts of noise about how we need to reduce SS benefits. More lack of sleep ahead.

|

Mostly from folks old enough to be exempted from sharing the pain, I suspect.

__________________

"Hey, for every ten dollars, that's another hour that I have to be in the work place. That's an hour of my life. And my life is a very finite thing. I have only 'x' number of hours left before I'm dead. So how do I want to use these hours of my life? Do I want to use them just spending it on more crap and more stuff, or do I want to start getting a handle on it and using my life more intelligently?" -- Joe Dominguez (1938 - 1997)

|

|

|

|

|

03-05-2013, 09:50 AM

|

#16

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2005

Location: Crownsville

Posts: 3,746

|

I just ran a scenario, playing out what would have happened if I had retired on December 31, 2007. The numbers I used were a starting portfolio of $1,320,000, and a withdrawal of $40,000 per year (not adjusted for inflation though, just doing a quick and dirty calculation). Basically, shooting for a 3% withdrawal rate.

My portfolio saw a loss of 42% in 2008, gained 44.7% in 2009, gained 19.8% in 2010, lost 0.12% in 2011, and gained 15.9% in 2012.

So, in this hypothetical scenario, I would've seen the following year-end balances:

12/31/07: $1,320,000 (start balance)

12/31/08: $742,400 (ouch!)

12/31/09: $1,016,373 (pretty nice recovery)

12/31/10: $1,169,695

12/31/11: $1,128,339

12/31/12: $1,261,385.

Truth be told, if I had hit my threshold at the end of 2007 and retired, I would've been sweating bullets as 2008 sort of petered out and then crashed towards the end. I ran this calculation assuming the whole $40K gets pulled out at the beginning of the year, so by the time late 2008 started rolling around, I probably would've been trying to cut expenses anywhere I could, and start looking to go back to w*o*r*k.

Instead of pulling out $40K at the beginning of 2009, I probably would have tried to scrimp and save, and make do with less. But, once we got to the end of 2009, and things were looking rosy again, I would've probably started kicking myself, if I had indeed gone back to w*o*r*k.

I guess this scenario also shows why it can be good to have several years of living expenses in something conservative. While I wouldn't think twice about pulling out that $40K, when I had $1320K, pulling out $40K the next year, when the balance is down to only $742K definitely does some long-term damage to future earnings.

I just ran the same scenario, assuming I pulled out $120,000 on 1/1/08, and then $0 for 1/1/09 and 1/1/10, but then going back to $40K for 1/1/11 and again for 1/1/12. Doing it this way, my 12/31/12 balance would be $1,304,014 instead of $1,261,385.

|

|

|

|

|

03-05-2013, 09:54 AM

|

#17

|

|

gone traveling

Join Date: Mar 2007

Posts: 559

|

Would it be less scary to retire if market was tanking like 2009.

if we could read the future -it would be nice. if you have the money to retire than i would retire.

my opinion is that if you live enough years in retirement you will see the market

have corrections several times-although hopefully not as bad as 2008-2010

|

|

|

|

|

03-05-2013, 10:05 AM

|

#18

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jan 2008

Location: NC

Posts: 21,303

|

Quote:

Originally Posted by Stanley

If my investments were financing all or most of my retirement, I would agree with this. If I had other retirement assets such as a pension or a decently high SS payout, I think 90% certainty would be good enough. 100% certainty is not possible in reality, since we don't know that the assumptions we make using FireCalc are going to hold for 30+ years. In other words, stay flexible, observe and adjust.

In the end, do whatever allows you to sleep at night.

|

Indeed, thanks for adding that...

__________________

No one agrees with other people's opinions; they merely agree with their own opinions -- expressed by somebody else. Sydney Tremayne

Retired Jun 2011 at age 57

Target AA: 50% equity funds / 45% bonds / 5% cash

Target WR: Approx 1.5% Approx 20% SI (secure income, SS only)

|

|

|

|

|

03-05-2013, 10:28 AM

|

#19

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Apr 2003

Location: Hooverville

Posts: 22,983

|

Quote:

Originally Posted by ziggy29

Mostly from folks old enough to be exempted from sharing the pain, I suspect.

|

If/when adjustments to SS net come about, age is going to be least important or perhaps a not at all important.

It is a political problem; who is it easy to whip up hatred for, the old or the affluent?

First comes taxation changes- very easy to sell. I have never paid less than 85% on my SS payments, but there are many threads on this board made up of well off people about keeping a low tax rate on SS payments. Next comes some sort of "adjusted AGI fiddling" and tax surcharges. Also an easy sell, because once again the losers will be the hated rich. Sometime changes will be made to SS and Medicare tax rates, though there is resistance to this because this might make the good folk in white hats- the low earners- pay more. The cap on what is taxed may be raised, and non-wage income also subjected to SS tax. Another good one, since those nasty richies who have the audacity to have "unearned income" will be the victims. And don't forget those nasty peole who made the mistake of going to work in private industry, and getting those obscenely huge 401K balances, they deserve punishment.

Along the way some fancy footwork may be required to kep carried interest and other perks of the truly rich exempt from SS taxation. But trust our hard working politicos. Since a nice slice of this wage gusher gets diverted directly to them, it will be preserved.

Ha

__________________

"As a general rule, the more dangerous or inappropriate a conversation, the more interesting it is."-Scott Adams

|

|

|

|

|

03-05-2013, 10:30 AM

|

#20

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Oct 2005

Location: North Oregon Coast

Posts: 16,483

|

Quote:

Originally Posted by haha

It is a political problem; who is it easy to whip up hatred for, the old or the affluent?

|

I think you are correct, but it's also an example of why all we can do is kick the can. Everyone is looking for other people to vilify, to blame, and for everyone *else* to endure spending/entitlement cuts and tax increases.

__________________

"Hey, for every ten dollars, that's another hour that I have to be in the work place. That's an hour of my life. And my life is a very finite thing. I have only 'x' number of hours left before I'm dead. So how do I want to use these hours of my life? Do I want to use them just spending it on more crap and more stuff, or do I want to start getting a handle on it and using my life more intelligently?" -- Joe Dominguez (1938 - 1997)

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode