C

Cut-Throat

Guest

The Quicken retirement planner, with its 'what if' scenarios can help eliminate fears of portfoilo failure very nicely.

For example: - I have mine set up for a conservative 3% return over inflation. If the worst (or close to it) would happen (say stocks lose 50% of their value the day you retired) and I am invested 50% in stocks my portfoilo would take a 25% hit. Even if stocks still only gained 3% in the future my overal plan would still work, without changing spending habits or worrying about timing the market.(Not to mention that stocks would probably do much better after a hit like that).

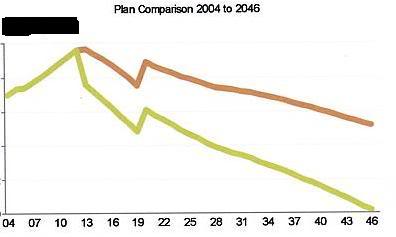

The graph draws 2 lines showing your current plan with a brown line and the what if scenario is a different colored line in yellow.

FIRECALC does the same thing but applies historical prices to your portfolio rather than ones you set. The Quicken planner is just a lot simpler.

For example: - I have mine set up for a conservative 3% return over inflation. If the worst (or close to it) would happen (say stocks lose 50% of their value the day you retired) and I am invested 50% in stocks my portfoilo would take a 25% hit. Even if stocks still only gained 3% in the future my overal plan would still work, without changing spending habits or worrying about timing the market.(Not to mention that stocks would probably do much better after a hit like that).

The graph draws 2 lines showing your current plan with a brown line and the what if scenario is a different colored line in yellow.

FIRECALC does the same thing but applies historical prices to your portfolio rather than ones you set. The Quicken planner is just a lot simpler.