|

|

11-02-2016, 08:07 AM

11-02-2016, 08:07 AM

|

#41

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2010

Location: Kerrville,Tx

Posts: 3,361

|

Quote: Quote:

Originally Posted by urn2bfree

I'm confused.

Suppose I make enough in qualified dividends to be sitting at the very top of the 15% bracket ($75,300 or whatever it is in that year). I am paying Zero federal taxes and state tax rate will vary.

So my question is just considering federal taxes.

Now what happens if I make $1 more as ordinary income or non qualified dividend?

I pay $0.25? Right? Because now I am in the 25% bracket. But it pushes $1 of the dividends over the edge and so it falls into 15% tax. So I pay another $0.15 in taxes? Total FEDERAL tax bill is now $0.40? So the last dollar having created a tax bill of $0.40 was taxed at 40%? (And is that the case of every dollar thereafter up to the next bracket?). So while I am taxed at the very low overall rate of essentially zero (0.4/75301). Every dollar I try to make above my dividends or cap gains has to be thought of as $0.60?

Do I have that right?

Sent from my iPad using Early Retirement Forum

|

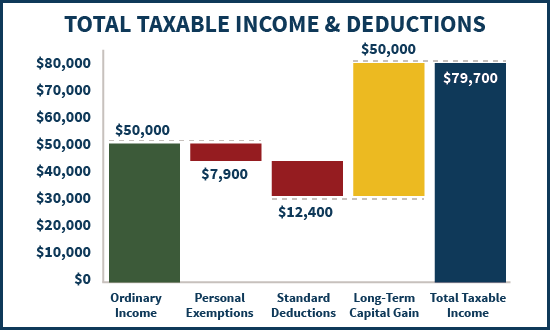

Actually note that if the last dollar was dividends it does not affect the tax bracket. (look at the qualified dividends and capital gains worksheet). You find that you take your gross income and subtract the amount of qualifed dividends and capital gains from it before figuring your tax. So in the case cited the amount used in the tax table would not include the last qualified dividend amount.

In essence

Total income-qualifed dividends-capital gains= income used in tax table or bracket. The qualified dividends are taxed at their 15 (or 20% if very high income) rate. At the bottom of the form you add the tax table amount and the 15% rate on the qualified dividends and capital gains to get your tax due.

So the answer is 15% because the qualified dividends don't affect the tax bracket.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

11-02-2016, 08:35 AM

|

#42

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

I never truly understood this until I tried different numbers in that Qualified Dividends and Capital Gains Worksheet in a simple TurboTax run.

Start with your income (less deductions and exemptions) plus divs & CGs below the 15% limit. Divs & CGs are not taxed, and the last part of income is taxed at 15%. So every new $1 of income under the bar for that sum is taxed at 15%. A new $1 of CGs/divs is not taxed as long as you stay under the bar.

Now push that sum just above. The last part of income is still taxed at 15%, but now any part you push above 15% makes that much in CGs & divs taxed at 15% too. Now every new $1 of income is effectively taxed at 30%. A new $1 of CGs/divs is taxed at 15%.

Then push just income over the 15% top. You've now pushed every bit of divs & CGs into being taxed at 15%. Every new $1 of income is now taxed at 25%, but there's no additional impact to divs & CGs because they are all already taxed. A new $1 of CGs/divs is taxed at 15%.

This holds true until you get into the very high income level where CGs are taxed more. I don't worry about that one so you can figure it out for yourself if it applies.

|

|

|

|

|

11-02-2016, 08:43 AM

|

#43

|

|

Thinks s/he gets paid by the post

Join Date: Dec 2014

Posts: 2,511

|

Quote:

Originally Posted by meierlde

Actually note that if the last dollar was dividends it does not affect the tax bracket. (look at the qualified dividends and capital gains worksheet). You find that you take your gross income and subtract the amount of qualifed dividends and capital gains from it before figuring your tax. So in the case cited the amount used in the tax table would not include the last qualified dividend amount.

In essence

Total income-qualifed dividends-capital gains= income used in tax table or bracket. The qualified dividends are taxed at their 15 (or 20% if very high income) rate. At the bottom of the form you add the tax amount and the 15% rate on the qualified dividends and capital gains to get your tax due.

So the answer is 15% because the qualified dividends don't affect the tax bracket.

|

If you look at this thread and many others like it, people are looking for effective marginal rates, not IRS defined tax rates. For instance if one had ordinary income to the middle of the 15% IRS marginal bracket and the rest of the 15% bracket filled with Q-divys. If one adds 1 $ of ordinary income, the tax increases by 30 cents (or 30%). 15% is attributed to the added ordinary income in the 15% bracket and 15% by 1 $ of Q-divy being pushed above the 15% IRS marginal rate (resulting from the addition of 1 $ ordinary income). So the effective marginal rate is 30%, the ordinary income was taxed as 15% and caused a Q-divy to be taxed differently.

people are including PTC into the effective marginal rate.

The effective rate is likely more of a consideration when looking at roth conversions and other other adjustments or tax planning than just the IRS marginal rate.

|

|

|

|

|

11-02-2016, 01:07 PM

|

#44

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,361

|

^^^^^ this.

30% if your ordinary income is already in the 15% tax bracket and qualified income (divs or LTCG) fill up the rest of the 15% tax bracket. Add $1 and you get 15c of more ordinary tax and $1 over the 15% tax bracket that gets taxed at 15% CG/Qdiv rate for a total of 30c. That is why I do my tax return, determine how much over the 15% tax bracket I am and then recharacterize any excess... I'm not paying 30% when I can so easily avoid it!

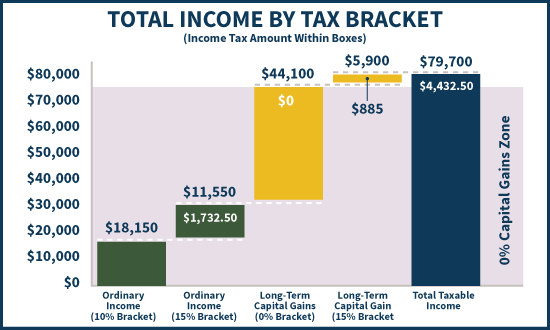

This is a pretty good explanation... especially the graphs.

So if you add $100 of ordinary income it increases 15% rate ordinary income from $11,550 to $11,650 and the tax increases from $1,732.50 to $1,747.50. That $100 of additional ordinary income increases capital gains subject to 15% tax from $5,900 to $6,000... increasing the capital gains tax from $885 to $900. So the total tax bill increases from $4,432.50 to $4,462.50... an increase in tax of $30 on a $100 increase in ordinary income (like Roth conversions).

If the $100 increase is $100 of more capital gains or qualified dividends then the tax increase is only $15.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

11-02-2016, 03:47 PM

|

#45

|

|

Full time employment: Posting here.

Join Date: Jul 2013

Posts: 953

|

I tried to identify all of the factors that go into this, and quickly ran into a number of circular references. The last one I thought of was this:

If you are drawing SS and your age is less than XX, then you also lose $Y.YY for each additional $ of earned income.

So, as soon as we can agree on the proper time to begin drawing Social Security, then I believe we can optimize the answer to the OP's question!

|

|

|

|

|

11-02-2016, 03:57 PM

|

#46

|

|

Thinks s/he gets paid by the post

Join Date: Mar 2010

Location: Kerrville,Tx

Posts: 3,361

|

Note that another example is Medicare Part B (and D) premiums. For part B if your magi goes from 85000 to 85001 then your part B premiums go up by $ 586.80 for the year (the same applies for the higher break points, all be it with different amounts).

This is a point that is often discussed with welfare benefits where there are points where above 100% taxation applies (as it does in this case).

The tax code is full of things with dollar amount limits that cause such behavior.

|

|

|

|

|

11-02-2016, 05:40 PM

|

#47

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2006

Location: Boise

Posts: 7,882

|

My tax situation is so complicated this year that I did not trust myself to figure out all of the marginal additions and subtractions and adjustments and cliffs and stuff. I have salary income, traditional IRA contribution, Roth conversion, 1099 income, dividends, interest, capital gains subject to section 1202 exclusions, ACA subsidies and a partridge in a pear tree.

The only thing I could figure to do was to fire up 2015 Turbotax and put all of my real numbers into it, then start adding in another $1000 of IRA contribution and/or capital gains and/or Roth conversions and see what the effective marginal rate was on those deltas.

I also figure personally I am OK paying tax at 15% but not at 20%, so I fiddled with it until the numbers settled down.

In my case, what made sense was a full traditional IRA contribution, realizing all of the CGs I had, and then a reasonable sized Roth conversion. I overconverted so as my last dividends and interest and stuff comes in next month and as things settle down, I can recharacterize to get exactly where I want to be.

This is my first year that I can pick my AGI and I'm excited about the options but a little bewildered and disappointed by the complexity of the tax code. I look forward to seeing my actual tax return so I can figure out what actually happened - like, did I actually get any benefit from the saver's credit, or did I get the full child tax credit, etc.

__________________

"At times the world can seem an unfriendly and sinister place, but believe us when we say there is much more good in it than bad. All you have to do is look hard enough, and what might seem to be a series of unfortunate events, may in fact be the first steps of a journey." Violet Baudelaire.

|

|

|

|

|

11-06-2016, 08:00 PM

|

#48

|

|

Thinks s/he gets paid by the post

Join Date: Feb 2014

Location: Syracuse

Posts: 3,502

|

15 cents Federal income

4 cents State income

8 1/2 cents County/ State sales tax.

__________________

No, not rich. I am a poor man with money, which is not the same thing"

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|