TimSF

Recycles dryer sheets

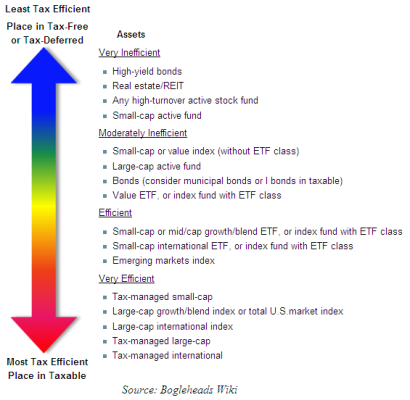

I purchased Wellington and Wellesley fund shares for the first time last October and was a bit surprised at year-end at the tax hit in these funds for 2013.

How do I estimate the anticipated "income" in these funds for 2014? I am concerned that a significant amount of unrecognized "income" in these funds might push me over the ACA subsidy cliff. I am even considering ditching these funds for something with a more tax-efficient focus.

Your thoughts are most welcome.

How do I estimate the anticipated "income" in these funds for 2014? I am concerned that a significant amount of unrecognized "income" in these funds might push me over the ACA subsidy cliff. I am even considering ditching these funds for something with a more tax-efficient focus.

Your thoughts are most welcome.