The reason is simple the Central Bank is purchasing the debt and returns the interest it receives back to the government. This means the debt is held at actually no cost. By purchasing 95% of the debt each year, the stated goal is to buy enough to hold 10 year treasuries under .1 %. The debt purchase is merely the funding of a negative national account under the government. A side benefit is that they are also buying 95% of the debt that is rolling over, lowering interest costs to contain budget deficits that would otherwise rise. As the Japanese defict spending is not causing an acceleration of monetary supply at the present time (money in circulation is not showing increased velocity), the Central Bank's purchase effectively causes nothing as the increases as the monetary impact of the central government spending is not causing inflation. This appears to mainly be due to the aging of Japanese society.

Once inflation begins however, the Japanese government have no means to control the mechanism and the years of effective cancellation of debt will be over. The time this will occur is totally and completely unpredictable however when it occurs, the fallacy of the former process will be clear to see.

As an example,

If you were to issue a mortgage to yourself and take the proceeds and buy a house, as long as the homeowner takes your currency and the currency used to purchase the house continues to rotate through the economy as being seen of value there is no problem. It could circulate throughout history and if it is acknowledged as holding value it does. You will not foreclose on yourself so there is no risk of default and the currency is always "backed". But there is no backstop once the market decides your currency does not have sufficient value to hold and the holders spend to rid themselves of it.

Thank you for that clear explanation.

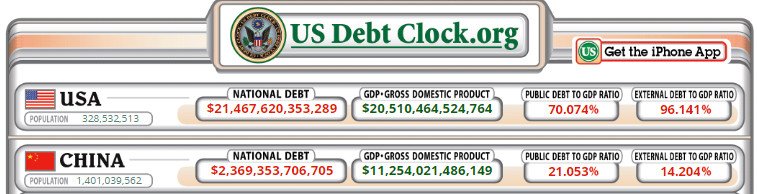

The overwhelming amount of information on the World Debt Clock really boils down to the perceived value of the "dollar" of whatever type. A matter of confidence.

Borrowing to stimulate an economy or to pay for governmental needs not covered by income or taxes, obviously stimulates a government economy... but only as long as the debt is backed by confidence in the borrower. The amount of debt is only as important as the world confidence in the ability to repay.

While the relative amount of debt as a percentage of a country's GDP appears to be the determining factor of monetary strength, perception of strength comes from current and historical value... much in the same way as our personal credit rating limits our ability to borrow. Taking this analogy one step further, a current credit rating, might drop from 800 to 500 quite suddenly should a number of personal bankruptcies come to light. An individual may still be able to borrow, but at increasingly high interest rates.

Loss of confidence can be fast or slow. Interest rates may be one indicator of a "dollar" strength, but in the case of international monetary balance, the exchange of owned debt is more subtle. Thus, as an example, if Russia were to sell some of their Chinese debt, the temporal effect on the international marketplace would probably be slower than if China were to sell American debt. An extremely delicate balance... not just between two parties, but effecting everyone, everywhere.

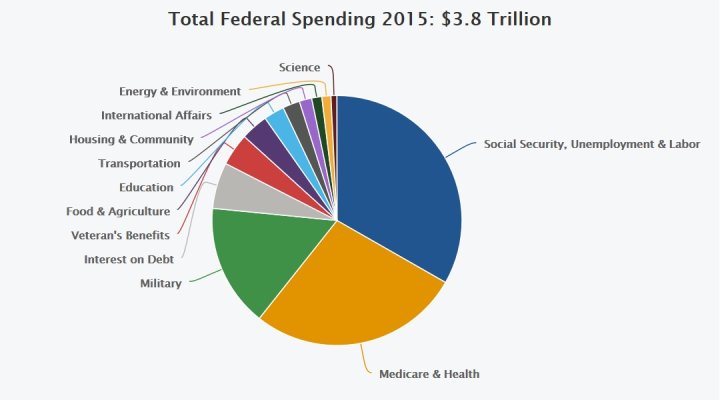

The national debt has grown by more than $10 trillion in just 10 years to $21 trillion dollars, with a current projection to add another $3 trillion dollars in the next four years.

Debt may be the major long term concern for early retirees. Who sets limits?