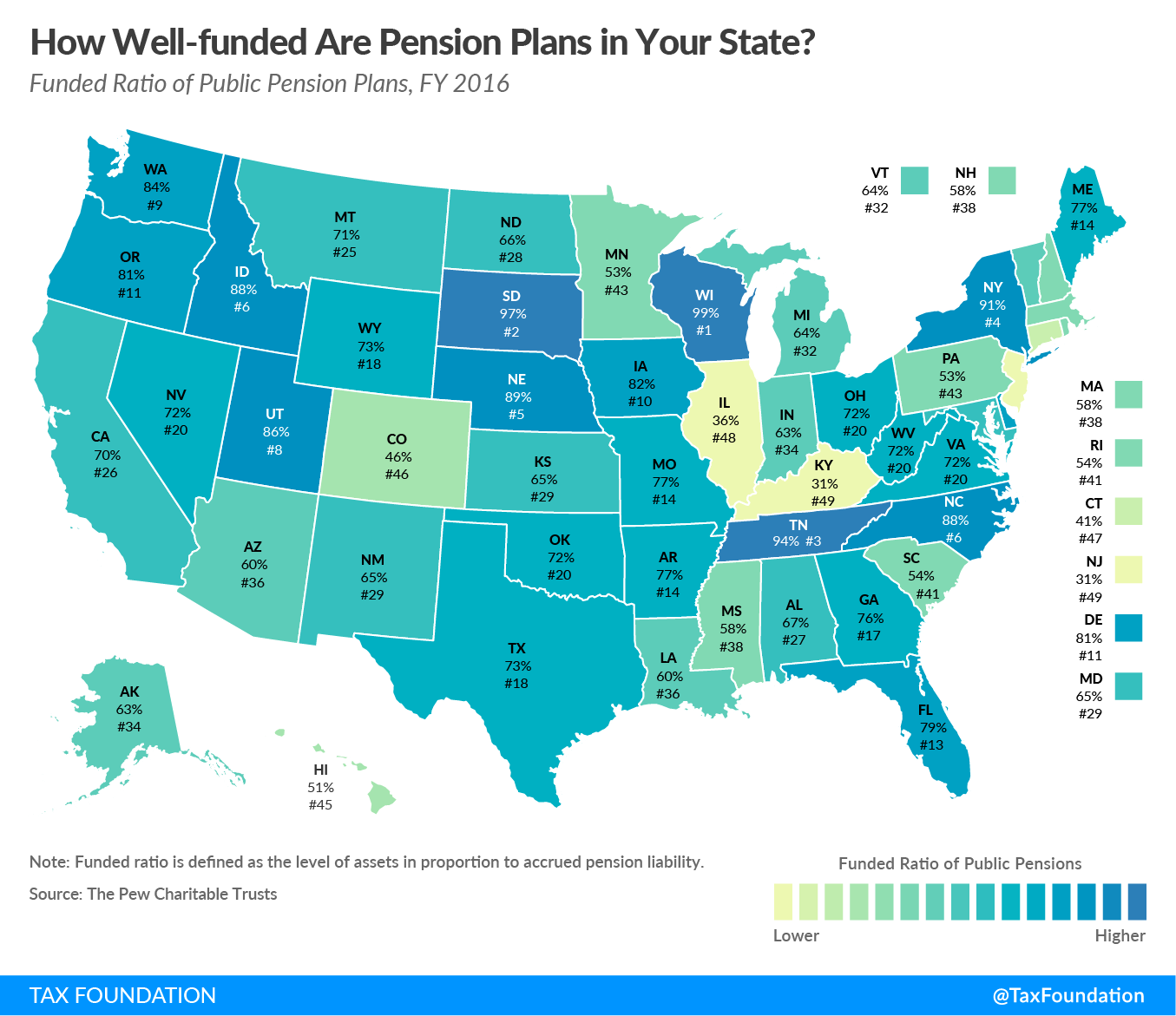

It's not getting better as pensions take on more risk to make up for their shortfalls:

https://wirepoints.org/chicagoans-pensioners-beware-a-stock-market-shock/

I figure most of the affected ER people here are watching closely but this will surprise many retirees.

https://wirepoints.org/chicagoans-pensioners-beware-a-stock-market-shock/

I figure most of the affected ER people here are watching closely but this will surprise many retirees.