Midpack

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

With about 40% of my AA in (short duration) bond funds, clearly I believe bonds are better than cash/CDs for at least a few years (2014-15 before it's time to find the exits), but on this reasonable people can certainly disagree (and have here).

But I sure hope the "yield famine" isn't as protracted as this economist suggests, but who knows. Sheeeeeeesh...

But I sure hope the "yield famine" isn't as protracted as this economist suggests, but who knows. Sheeeeeeesh...

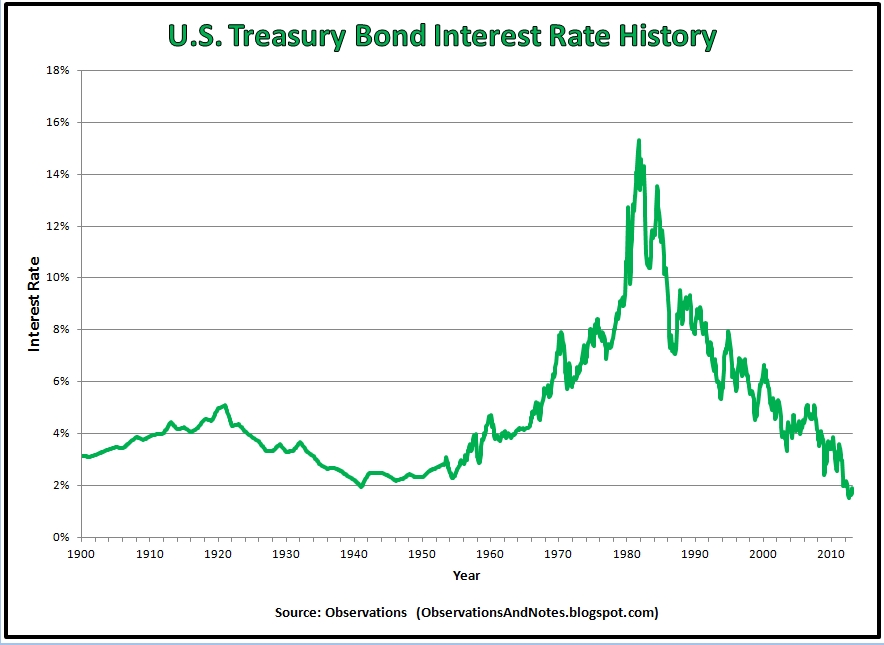

AssetBuilder - Lacy Hunt: The End of the Yield Famine Is Far Away - AssetBuilder Inc., Registered Investment AdvisorHow long can this low interest rate siege last?

Borrowers will love his answer to the question. Savers will be troubled. Flipping through one of his chart collections, Dr. Hunt comes to a chart that overlays the history of interest rate declines after major financial panics. If the future replays such past events, it takes about 14 years for interest rates to hit bottom. Since our last financial debacle was in 2008, that suggests interest rates may continue falling until 2022. Yes, savers, you read that right: 2022.

And when that happens, the same data shows that long-term government bond yields will bottom at about 2 percent, compared to their current rate of 2.9 percent. Even 20 years after financial disasters like 2008, interest rates are only about 2.5 percent.

Savers are facing a yield famine that could last beyond 2028. And borrowers who just refinanced their homes at 3.5 percent may have yet another opportunity to reduce their mortgage payment.