|

Trying to understand capital gains

10-08-2017, 11:33 AM

10-08-2017, 11:33 AM

|

#1

|

|

Full time employment: Posting here.

Join Date: May 2010

Posts: 659

|

Trying to understand capital gains

Hi All

Married filing jointly I know under $75,300k income equals zero capital gains tax and above $75,300k would trigger 15% capital gains tax.

If you had capital gains income (no other income) above $75,300 are you taxed at 15% for all of the capital gains or only the portion above the $75,300?

phil

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

10-08-2017, 12:13 PM

|

#2

|

|

Moderator

Join Date: Oct 2010

Posts: 10,720

|

It's not a "cliff" that you fall over, so no, you only pay tax on the portion over the threshold.

In tax software, I put in a $96,100 capital gain. When netting out the 12,600 standard deduction and 8,100 exclusion, that left $75,400 and the tax was $15.

|

|

|

|

|

10-08-2017, 08:25 PM

|

#4

|

|

Full time employment: Posting here.

Join Date: May 2010

Posts: 659

|

Thanks for that. I presumed it would be something like that but could not see if stated clearly.

|

|

|

|

|

10-09-2017, 07:36 AM

|

#5

|

|

Thinks s/he gets paid by the post

Join Date: Jul 2013

Posts: 1,883

|

Quote: Quote:

Originally Posted by captain3d

Thanks for that. I presumed it would be something like that but could not see if stated clearly.

|

Cliffs such as the one you were concerned about are pretty rare in the tax code, but some do exist. Subsidies for the ACA are one:

https://www.healthinsurance.org/obam...subsidy-cliff/

|

|

|

|

|

10-09-2017, 09:01 AM

|

#6

|

|

Recycles dryer sheets

Join Date: Jan 2015

Location: Dublin

Posts: 88

|

Quote:

Originally Posted by captain3d

Hi All

Married filing jointly I know under $75,300k income equals zero capital gains tax and above $75,300k would trigger 15% capital gains tax.

If you had capital gains income (no other income) above $75,300 are you taxed at 15% for all of the capital gains or only the portion above the $75,300?

phil

|

Thanks for asking this question and thanks to those who answered. I had the identical question and this information is very helpful at the moment!

|

|

|

|

|

10-09-2017, 10:22 AM

|

#7

|

|

Full time employment: Posting here.

Join Date: Dec 2012

Posts: 656

|

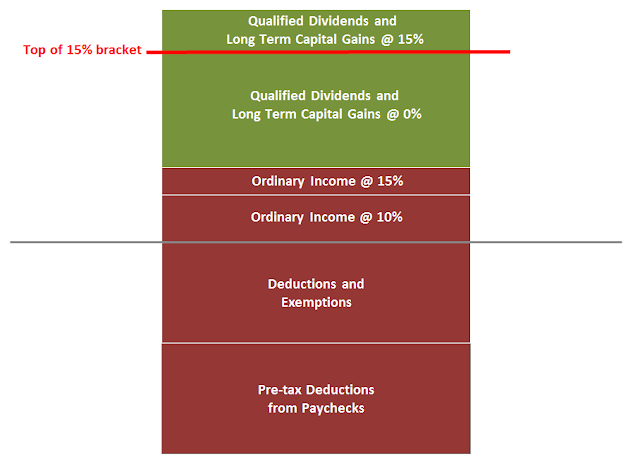

Credit to tfb at the Boglehead Forum

|

|

|

|

|

10-09-2017, 11:59 AM

|

#8

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,345

|

One thing to keep in mind is that once you cross the 15% tax bracket, even if you have a lot of preferenced income (qualified dividends and LTCG) if you add some ordinary income your marginal rate can be 30% even if you are not taking ACA subsidies. What happens is the incremental ordinary income is taxed at 15%, plus it bumps the same amount ot LTCG that was previously taxed at 0% into being taxed at 15% as well.

So for example, say a married couple has $40,000 or ordinary income and $56,700 of preferenced income. Their TI would be $75,900 after $12,700 standard deduction and $8,100 of exemptions and their tax would be $1,948.

They then add a $100 ordinary income.... their tax on ordinary income increases by 15% since they are in the 15% tax bracket... but the $100 of capital gains that is above the top of the 15% tax bracket also gets taxed at 15% so that $100 of odinary income results in $30 additional tax.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

10-09-2017, 02:21 PM

|

#9

|

|

Thinks s/he gets paid by the post

Join Date: Aug 2017

Location: Champaign

Posts: 4,722

|

We are discussing 2017 income and ACA deductions. The ACA requires you to make income and any other life change in the application for 2018. I'm assuming the subsidies will be there for 2018. We are currently figuring out the possible future from this site. Hopefully, in the next 2 weeks we'll have a better idea what plans will be there and what income level we are in.

https://www.healthcare.gov/see-plans/

__________________

"Do not go where the path may lead, go instead where there is no path and leave a trail."

Ralph Waldo Emerson

|

|

|

|

|

10-09-2017, 02:57 PM

|

#10

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

Quote:

Originally Posted by Rianne

We are discussing 2017 income and ACA deductions. The ACA requires you to make income and any other life change in the application for 2018. I'm assuming the subsidies will be there for 2018. We are currently figuring out the possible future from this site. Hopefully, in the next 2 weeks we'll have a better idea what plans will be there and what income level we are in.

https://www.healthcare.gov/see-plans/ |

Kind of. If you want to get the subsidy in advance, you need to get your 2017 income in line. But you can still get the 2018 subsidy back as a tax credit after you file 2018 taxes. I did this for 2016. Form 8962.

If you also want cost sharing subsidies, I think you may have to qualify in advance, but I'm not close to 250% so I really haven't looked at this.

|

|

|

|

|

10-10-2017, 09:54 AM

|

#11

|

|

Confused about dryer sheets

Join Date: Feb 2013

Location: Naperville, relo to Fort Collins...

Posts: 8

|

I don't want to derail this thread, but I have a similar question. If it become a distraction I will post in a separate thread.

Let's say I decide to retire sometime in March 2018. I do not need the cash, so I elect to contribute most of my 2018 salary to my 401(k). My employer allows 90%.

When I retire in March I would have only $2-3 K in actual take-home money but $20-24 K in additional money in my 401(k). I will also have quite a bit of LTCG in 2018. Is all of my income added to the capital gains calculation, or only the "take-home money"?

|

|

|

|

|

10-10-2017, 10:00 AM

|

#12

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jun 2007

Posts: 13,227

|

Quote:

Originally Posted by Yogi Bear

I don't want to derail this thread, but I have a similar question. If it become a distraction I will post in a separate thread.

Let's say I decide to retire sometime in March 2018. I do not need the cash, so I elect to contribute most of my 2018 salary to my 401(k). My employer allows 90%.

When I retire in March I would have only $2-3 K in actual take-home money but $20-24 K in additional money in my 401(k). I will also have quite a bit of LTCG in 2018. Is all of my income added to the capital gains calculation, or only the "take-home money"?

|

The 401K money is not included as it is deferred income.

|

|

|

|

|

10-10-2017, 10:02 AM

|

#13

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2014

Location: Spending the Kids Inheritance and living in Chicago

Posts: 17,085

|

Quote:

Originally Posted by Yogi Bear

I don't want to derail this thread, but I have a similar question. If it become a distraction I will post in a separate thread.

Let's say I decide to retire sometime in March 2018. I do not need the cash, so I elect to contribute most of my 2018 salary to my 401(k). My employer allows 90%.

When I retire in March I would have only $2-3 K in actual take-home money but $20-24 K in additional money in my 401(k). I will also have quite a bit of LTCG in 2018. Is all of my income added to the capital gains calculation, or only the "take-home money"?

|

For you your income would be the gross amount you take home (includes taxes paid for example).

So your take home would end up on the tax return as the $2-3 K + your dividends + LTCG

You could easily end up not paying any tax

If you do your own taxes with software, then just copy last years file to a new name, and load it into your tax return software, since most stuff is constant, reduce your salary amount and add 20K LTCG and see what happens.

|

|

|

|

|

10-10-2017, 03:51 PM

|

#14

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,345

|

Quote:

Originally Posted by Yogi Bear

I don't want to derail this thread, but I have a similar question. If it become a distraction I will post in a separate thread.

Let's say I decide to retire sometime in March 2018. I do not need the cash, so I elect to contribute most of my 2018 salary to my 401(k). My employer allows 90%.

When I retire in March I would have only $2-3 K in actual take-home money but $20-24 K in additional money in my 401(k). I will also have quite a bit of LTCG in 2018. Is all of my income added to the capital gains calculation, or only the "take-home money"?

|

I did exactly what you propose to do except my employer allowed 100%.

Let's say that your gross pay for the 2 1/2 months is $27k and you defer $24k... your taxable earnings for 2018 woudl be the difference of $3k.

Or put another way, your taxable earnings would be your gross earnings less 401k contributions, just like it always is.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

10-12-2017, 10:33 AM

|

#15

|

|

Full time employment: Posting here.

Join Date: Aug 2015

Posts: 987

|

Figured it out.

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|