|

|

06-22-2014, 12:00 PM

06-22-2014, 12:00 PM

|

#21

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2008

Location: Leeward Oahu

Posts: 17,911

|

Suggest you demand a prospectus for the VA. If none is available, STOP. If available, read every word. Before you invest, UNDERSTAND every word. Be able to SELL a VA to your best friend before you buy one.

Sorry to be "harsh", but I've made every mistake in the book - no need for you to do the same. So, be aware of EXACTLY what you are buying and what it will cost you before you buy.

YMMV. Good luck.

__________________

Ko'olau's Law -

Anything which can be used can be misused. Anything which can be misused will be.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

06-22-2014, 12:33 PM

|

#22

|

|

Recycles dryer sheets

Join Date: Jul 2011

Posts: 57

|

Santa Clause, the Easter Bunny, and an honest annuity salesman walk into a bar...

|

|

|

|

|

06-22-2014, 01:37 PM

|

#23

|

|

Recycles dryer sheets

Join Date: Sep 2006

Location: clearwater

Posts: 439

|

Your AGI and taxable income will play a part in deciding how much of your IRA to withdraw. If your income is low now, make withdrawals from the IRA.

You have enough money to set up a low cost investment plan. You do not need an annuity.

|

|

|

|

|

06-22-2014, 02:23 PM

|

#24

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Apr 2003

Location: Hooverville

Posts: 22,983

|

I'll simplify it for you. Walk on by, and leave your money where it is.

Ha

__________________

"As a general rule, the more dangerous or inappropriate a conversation, the more interesting it is."-Scott Adams

|

|

|

|

|

06-22-2014, 07:45 PM

|

#25

|

|

Dryer sheet aficionado

Join Date: Aug 2011

Posts: 37

|

use cash or withdraw IRA

Quote: Quote:

Originally Posted by ERD50

This is key, IMO.

The poster has asked a specific question, and while the answers are helpful (dump the FA), it would be better to look at the big picture.

lacawac - We know you are now age 61, on SS disability and small pension, with $1M IRA and $300,000 in cash (earning almost nothing, and not fully FDIC insured). Further Q's:

1) What are your living expenses (including medical, housing)?

2) How much do you receive in SS? Pension? Is pension COLA'd?

3) Any big expenses to account for outside routine annual bills? A replacement car? Home repairs/upgrades?

4) How is the IRA invested?

5) Is there any reason to think your life expectancy would be shorter/longer than average?

With that info, people here can give some investment ideas and reasonable expectations for how much you could withdraw each year w/o depleting your portfolio during your lifetime. There are ways to draw from the IRA w/o incurring tax penalties, if needed.

-ERD50

|

thanks for your reply,will answer questions in order asked

1) $6,500 I live on Long Island NY

2) SSDI $2500 Pension $2165 no cola

3) home repairs,immediate needs about $30,000

4) annuity fund thru my union is with NY LIFE invested in

2015 target date fund $500,000

custom retirement fund $500,000

earned about 4% last year I guess because of good market?

5) optimistically hoping for 30 years

|

|

|

|

|

06-22-2014, 07:47 PM

|

#26

|

|

Dryer sheet aficionado

Join Date: Aug 2011

Posts: 37

|

Quote:

Originally Posted by rothlev

Your AGI and taxable income will play a part in deciding how much of your IRA to withdraw. If your income is low now, make withdrawals from the IRA.

You have enough money to set up a low cost investment plan. You do not need an annuity.

|

what do you mean by a low cost investment plan?

|

|

|

|

|

06-22-2014, 07:49 PM

|

#27

|

|

Dryer sheet aficionado

Join Date: Aug 2011

Posts: 37

|

Quote:

Originally Posted by unno2002

In our area, $500k would get you six rental properties, that would pay around $800 per month each in rent before 10% mgt fees.

|

I live on Long Island NY, that,s my area

|

|

|

|

|

06-22-2014, 08:44 PM

|

#28

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,888

|

Quote:

Originally Posted by unno2002

In our area, $500k would get you six rental properties, that would pay around $800 per month each in rent before 10% mgt fees.

|

That might work out well for some, but it appears he is interested in passive income & retirement, not taking on a job as landlord (even with a property manager).

-ERD50

|

|

|

|

|

06-22-2014, 11:19 PM

|

#29

|

|

Full time employment: Posting here.

Join Date: Dec 2006

Posts: 881

|

Please don't take this personal. Listen to all of the replies.

It's pretty obvious you are a novice, a sheep, ready to be sheared!

Glad you asked for help.

RUN don't walk from this Financial Advisor.

Unless, you educate yourself, don't make any complicated financial

moves.

Just stick to CD's and savings accounts....

|

|

|

|

|

06-23-2014, 04:34 AM

|

#30

|

|

Recycles dryer sheets

Join Date: Sep 2006

Location: clearwater

Posts: 439

|

If I were you I would do a trustee to trustee transfer of your funds to Vanguard, with that amount they would help you pick out some appropriate conservative funds. Wellesley income, for example. Some people who do have nest eggs that are small , and will run the risk of running out of money need and are appropriate for annuities. that is not your situation.

|

|

|

|

|

06-23-2014, 06:46 AM

|

#31

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,363

|

You don't need a VA. Your monthly gap is $1,835 a month or $22k a year. After immediate needs, you have $1.27 million. That is only a 1.7% withdrawal rate which is plenty low.

If you want simple, put everything in a conservative, no-load balanced fund with a low expense ratio and enjoy your retirement. You can also set up an automatic sale/transfer from you taxable accounts for your gap to get the $6,500 a month rolling in and then adjust it for inflation as your living expenses increase.

Quote:

Originally Posted by lacawac

thanks for your reply,will answer questions in order asked

1) $6,500 I live on Long Island NY

2) SSDI $2500 Pension $2165 no cola

3) home repairs,immediate needs about $30,000

4) annuity fund thru my union is with NY LIFE invested in

2015 target date fund $500,000

custom retirement fund $500,000

earned about 4% last year I guess because of good market?

5) optimistically hoping for 30 years

|

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

06-23-2014, 06:49 AM

|

#32

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Nov 2010

Location: Sarasota, FL & Vermont

Posts: 36,363

|

Quote:

Originally Posted by Animorph

....and a VA is not something that will make a big difference to your net worth. ...

|

I disagree. I think a VA will cause the OPs net worth to decline compared to other alternatives by the amount of the embedded fees.

__________________

If something cannot endure laughter.... it cannot endure.

Patience is the art of concealing your impatience.

Slow and steady wins the race.

Retired Jan 2012 at age 56

|

|

|

|

|

06-23-2014, 07:29 AM

|

#33

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,888

|

Quote:

Originally Posted by lacawac

4) annuity fund thru my union is with NY LIFE invested in

2015 target date fund $500,000

custom retirement fund $500,000

earned about 4% last year I guess because of good market?

|

It's a little tough to understand exactly how that is invested (annuity fund? 'custom'?), but for reference, Vanguard's 2015 retirement fund was up about 10% last year, which was a good market.

https://personal.vanguard.com/us/fun...FundIntExt=INT

Now that's a balanced fund, 'the market' was up in the range of 30% in 2013.

http://finance.yahoo.com/q/pm?s=VFIAX+Performance

As a rough cut, I de-valued your pension by half to account for no COLA, but that still leaves you at ~ a 2.8% withdraw rate (WR), which is pretty conservative (you could enter those into FIRECalc to check). But that is also based on a 75/25 asset allocation, and low fee index funds.

If your investments have high fees (and I suspect they do), that could turn this WR from conservative to risky. An added 1% in fees takes 2.8% to 3.8% (1% going to fees).

-ERD50

|

|

|

|

|

06-23-2014, 12:01 PM

|

#34

|

|

Recycles dryer sheets

Join Date: Jul 2011

Posts: 57

|

Quote:

Originally Posted by lacawac

Recently visited a FP who advised me to purchase a $500,000.00 Jackson Variable Annuity,hold for about 5 years which would earn 5% then start to withdraw from it.

|

Some Google work on 'Jackson Variable Annuity commission

Independent Review of the Jackson National Perspective II Annuity

Here are a couple excerpts:

<<<Typically variable annuities pay a 6-7% commission to the agent/broker. Thats why the insurance company charges you a surrender charge or what this brochure calls a contingent deferred sales charge. if you dont stay in the annuity long enough for the company to make a profit, you pay a surrender charge.

A surrender charge is a way for the insurance company to recover the costs of the commission they pay and it decreases over time.>>>

$500,000 x 6% = $30K. The FP could be objective, but I suggest he is much more of a salesman looking for that commission.

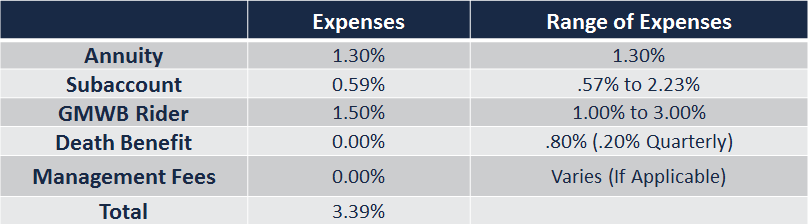

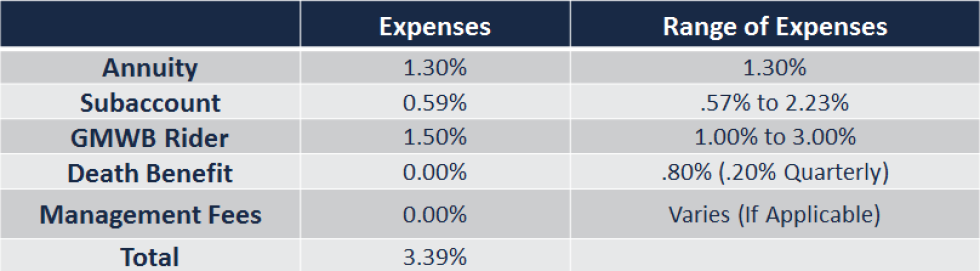

<<<The following is a list of the various expenses of the Jackson National Perspective II Annuity:>>>

There is a table which details the expense charges. For an S&P index type fund, which is the lowest expense charge, Jackson annual fees come out to 3.39%. If you were to hold an S&P index fund in Fidelity, the annual expense is 0.07%. (FUSVX, which rung up a 20% increase last year...)

<<<

This is a very complex annuity rider with a lot of moving parts so pay close attention.

This version of the Perspective II annuity has two components, the income base and the contract value. The income base is the amount that the income guarantee of the contract is based on. The contract value is the value of your subaccounts.

For the first 10 years of your contract the income base will be credited by the percentage that youve chosen. The fee associated with your annuity will vary based upon the percentage youd like your annuity to step up each year. Here are the expenses for the various income rider options:>>

Another table showing that these additional 'features' will add annual costs from 1% to 2.5%. They are looking to get into your returns somewhere from 4.5% to 6% every year. By the time you figure out that you have been had, you have either had 6 years of very low to negative return investing, or you are looking at surrender charges to get out of the annuity.

Surrender charges: There is a table in the link. 1st year- 7.5%, 2nd- 6.5%, 3rd- 5.5%, 4th- 5%, 5th- 4%, 6th- 2%.

These annuities are very confusing, lots of options and riders that make them a joy for the salesman to pitch. Whatever market fear a person might have, they can sell you a rider that only costs another 1 or 2% per year.

I have a second concern- it sounds like you made 4% last year on some of your investments, and thought it was a good year? It is possible that this union-based retirement is not in the best interests of the membership. I know there are some of those around. Just saying that I would be more interested in getting my money out of this under performing fund and into either Fidelity or Vanguard. There are many examples of simple 3 or 4 fund allotments that will do a good job of hands-off investment. There is no such thing as a guarantee in the market, but there is also no such thing as a guaranteed 5% return with no risk.

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

| Thread Tools |

|

|

| Display Modes |

Linear Mode Linear Mode

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|