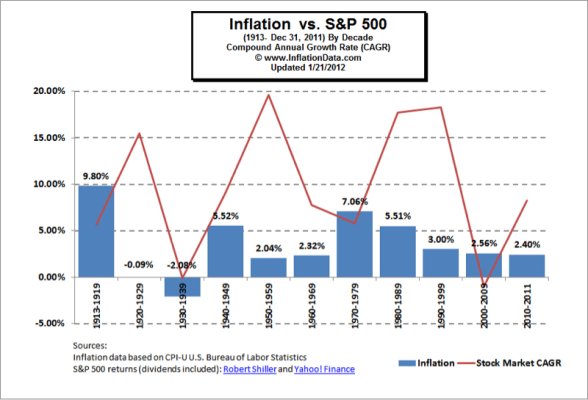

A good part of my post-retirement strategy includes upcoming inflation expectations over the next 40-50 years. I will be very concentrated in fixed income and the main risk is inflation. Also, inflation will push up nominal AGI which will push me into higher brackets. I do plan to invest small amounts into gold and TIPPS to hedge.

Looking at inflation swaps that trade in the financial markets, I pretty much derived

2013 2.10%

2014 2.30%

2015 2.60%

2016 2.70%

2017 2.80%

2018 3.00%

2019+ 3.00%

Any thoughts out there about your inflation expectations and what you are doing about this risk.

Looking at inflation swaps that trade in the financial markets, I pretty much derived

2013 2.10%

2014 2.30%

2015 2.60%

2016 2.70%

2017 2.80%

2018 3.00%

2019+ 3.00%

Any thoughts out there about your inflation expectations and what you are doing about this risk.

")