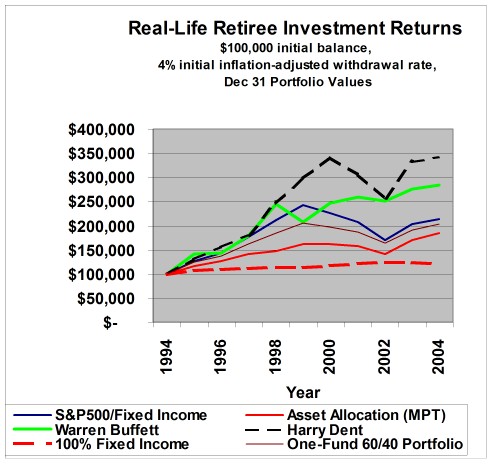

I roughly calculated a hypothetical scenario in which someone retired in Jan 2000 with 100% stock in s and p 500 (VFINX), with 4% inflation adjusted withdrawals. Most on this board will say that he must be a fool to do it. The outcome is not great, but probably not as bad as some might expect. In jan 05, that person still has 67.6% of the original amount, which is better than 50 to 80% drop some may expect from such an “undiversified” portfolio.

Assumptions: withdrawal is at the end of the year; first year’s expenses not figured in here, same as FIRECALC does.

Sources: yahoo finance for VFINX data and http://www.westegg.com/inflation/ for inflation data.

Date _____ Before VFINX adj Inflation adj ______ Money after shares of inflation

_________ withdrawal close withdrawal _______ withdrawal ______VFINX

January-00 $2,500,000.00 119.18 ___________ ______________20976.67

January-01 $2,479,023.33 118.18 $102,400.00 $2,376,623.33 20110.2 0.024

January-02 $1,989,300.89 98.92 $104,038.00 $1,885,262.89 19058.46 0.016

January-03 $1,450,158.24 76.09 $105,703.00 $1,344,455.24 17669.28 0.016

January-04 $1,806,506.82 102.24 $108,134.00 $1,698,372.82 16611.63 0.023

January-05 $1,801,863.26 108.47 $111,054.00 $1,690,809.26 15587.81 0.027

Assumptions: withdrawal is at the end of the year; first year’s expenses not figured in here, same as FIRECALC does.

Sources: yahoo finance for VFINX data and http://www.westegg.com/inflation/ for inflation data.

Date _____ Before VFINX adj Inflation adj ______ Money after shares of inflation

_________ withdrawal close withdrawal _______ withdrawal ______VFINX

January-00 $2,500,000.00 119.18 ___________ ______________20976.67

January-01 $2,479,023.33 118.18 $102,400.00 $2,376,623.33 20110.2 0.024

January-02 $1,989,300.89 98.92 $104,038.00 $1,885,262.89 19058.46 0.016

January-03 $1,450,158.24 76.09 $105,703.00 $1,344,455.24 17669.28 0.016

January-04 $1,806,506.82 102.24 $108,134.00 $1,698,372.82 16611.63 0.023

January-05 $1,801,863.26 108.47 $111,054.00 $1,690,809.26 15587.81 0.027

") . No more Singha beer for this bloke!

. No more Singha beer for this bloke!