MikeWillRetire

Recycles dryer sheets

- Joined

- Apr 27, 2012

- Messages

- 216

24K household, 29 years.

about:

30% various taxes

50% saved

20% live on

I will not go to exact numbers

So I had this silly idea that I wanted to see how much I saved on avg every year since I started working (after college). I didn't want to over complicate it so I just divided my current savings+investments by the number of years (16) since my first real job. I came to $22k per year.

Of course, for the first 8 years of my career I thought as long as I fully funded my 401k I was 'all set' for 'a retirement'. The next few years I started saving in maximum overdrive until the big D happened which took more than a few things out of my life; some good and some bad

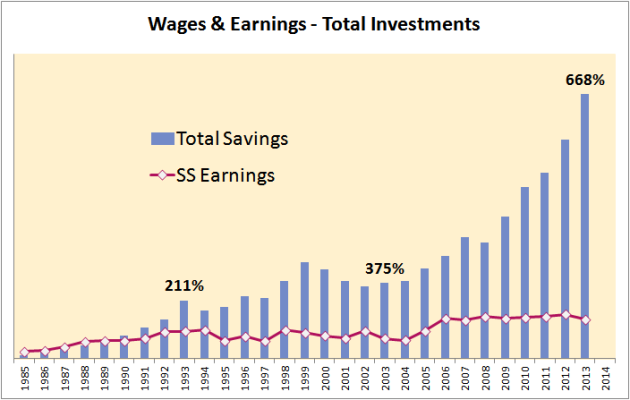

Not counting any 401k matching funds or 401k earnings (just my 401k contributions), and not counting the windfall from cashing out my company stock when I ERed in late 2008, I averaged about $42k in annual wage income from 1985-2008 and averaged $21k in savings and reinvested earnings from my taxable account's investments.

Not sure how useful doing this calculation would be, as my net worth doesn't just consist of money saved from my salary, but also profits from several houses sold and an inheritance.

I could do the math but the result wouldn't tell me, or anyone else, anything useful.