For some reason (probably the enabling legislation) the SDP limit is $10K. So assuming the calculator is correct you would indeed get the $68.21, but it would not compound to make additional interest. The only principal & interest that would compound would be the $10K.

The literature is using a non-standard explanation to make sure everyone understands that the maximum earned interest is $1000. While the 10% per annum is compounded quarterly, it results in a total of 10% annual percentage yield (APY). So instead of simple quarterly interest compounding at 2.5%, it actually compounds at 2.4113688% per quarter. If you plunked $10K into the SDP on 1 Jan and came back a year later, they'd hand you a check for $11K. For 120 days, well, you'd get at least a quarter's worth ($10K plus $231.14).

A credit union would be required to advertise their rates as "10% APY compounded quarterly" to use that same 2.4113688 quarterly percentage. If they intended to pay 2.5% per quarter (compounding both the principal and the accrued interest at 2.5% per quarter) then it would be a 10.38% APY. Simple? Yeah, sure.

I'm a bit skeptical about their comment "based on calendar year". To me that implies that if you deposit your SDP money anytime after a quarter begins (say between 2 Jan and 31 March) you don't get anything for that quarter-- only for the new quarter starting 1 April. But I could be overly cynical, although the Navy's bonus-pay system has given me the right to be that way.

Another reason I'm being cynical is because of that 90-day rule with its truncated month. They're saying that you may deploy for a period that's less than some number of full quarters, and they'll probably skip any interest payments until the start of the next quarter, so to

avoid bad publicity on the front page of Air Force Times be fair they'll continue to pay interest for up to a quarter after you leave the combat zone. Of course you have to leave the money on deposit with them for that extra quarter, so they still didn't pay you anything for holding your money for a quarter. And it's not really a full quarter, it's just two months unless your orders time it exactly right.

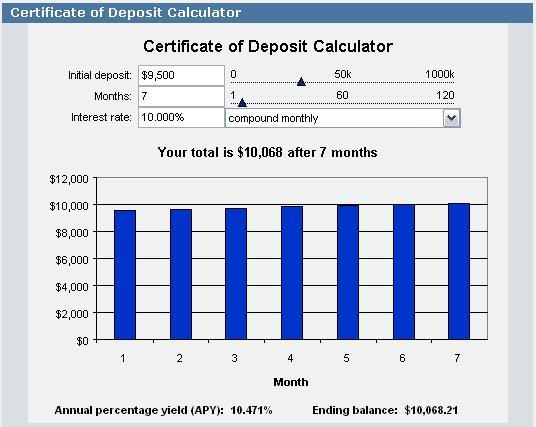

Your SDP calculator example shows that the money is compounding monthly for an APY of 10.471% (the advantage of compounding monthly vice quarterly). To make the calculator match the SDP verbiage you'd have to change that drop-down menu to "compounded quarterly", assuming it lets you do that. So you would probably get less than $10,068.21. A good bit less. And since it's taxable income, they'll probably withold some of that payment from you.

You want a SDP calculator that implements the program's verbiage correctly for the precise dates on your TDY orders. That's when they'll tell you what they mean by "calendar quarter" and "up to 90 days".

Quote:

Quote:

Originally Posted by Keyboard Ninja

I currently have $125 of my pay automatically alloted towards my savings account, and 15% of my base pay (E-3) towards the TSP fund. Does this mean I can only contribute up to my monthly take home pay?

|

Yes, the way they describe it, it sounds as if your SDP contribution would be limited to one month of take-home pay. Hardly the $10K limit they were referring to, except for flag officers.

I was under the impression that you could hand over a check for $10K from your brokerage account, but they way they seem to have set up the rules that doesn't appear to be the case.

So, like BK says, max out the TSP and the Roth before you "take advantage" of the SDP.

Linear Mode

Linear Mode