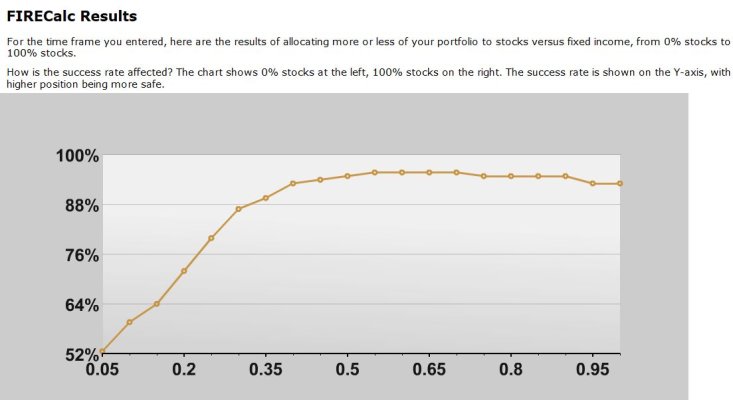

Some of these replies are very confusing. It would help to explicitly state whether you are using FIRECalc as most do, with the default of a historical report, or are you using the "

consistent growth of %, and an inflation rate of %" or "

portfolio with random performance", option?

Big, big difference. IMO, the historical is useful, the other two are maybe only 'interesting' - to some (not me).

Originally Posted by jabbahop View Post

....

One thing I have done that I think someone suggested on this forum is to test for “an even worst case” sequence of returns. What I do is to first change the number of years of retirement to something short - i use ten years. And then take the worst case portfolio balance RESULT of that worst 10 years sequence and run a new scenario for the remaining 25 years of planned retirement to see (and the worst sequence of returns AGAIN) and see what our chance of surviving is.

Good one. I'll try those scenarios.

I change a bunch of things. If you want to scare yourself:

Try consistent growth of 4% and inflation rate of 3%

Shave the SS 25%

Figure 70% of portfolio taxed at 12%

I do all sorts of manipulating to see worse case scenarios.

Rianne, your two statements are at odds with each other. If you are setting consistent growth/inflation rates, then the 10 year and 25 year sequences that

jabbahop mentions don't apply. There is no difference in splitting them up.

IMO, stringing the two sequences is really extreme - you get hit with the worst ever ten years apart. It just seems beyond anything realistic. Those worst case drops come after a run-up (bubble of sorts). If you are still down, another down period like that is just extremely far from likely.

However, there is value in that 10 year run (or a 5 year run). People often focus on the end result, and those mid years get crowded on the graph. But people should be aware that even with a conservative WR, a successful portfolio can take a deep dive in the first 5-10 years. And it succeeds even w/o cutting spending.

And you can play with that, and find that the oft-heard comment around here that "if my portfolio tanks, of course I'll just cut back some", really does very little, even with extreme cuts, done early (before you even know you are in deep trouble), and can last a long time before they have much effect.

To provide some perspective - if you have a conservative 3% WR, and your portfolio tanks 40%, a 1.5% drop in WR is a pretty minor thing. But unless you have a lot of discretionary budget, cutting half your spending will be painful. Heck, even with a large discretionary budget, cutting half your spending will be painful. You must be having fun with that budget, who wants to cut back in the early years, when we are best able to enjoy it? If you like to travel, or hike/camp, etc, that may not be so much fun in your later years.

I have an old thread on this, something about "scary dips" in the title?

-ERD50