dixonge

Thinks s/he gets paid by the post

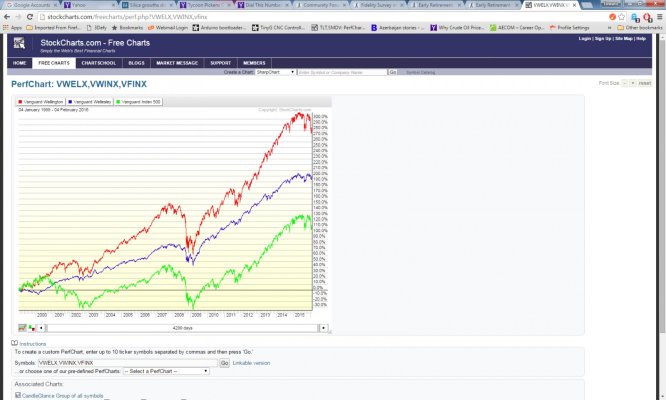

So after a big spreadsheet session yesterday I realized that we might actually start to accumulate some extra cash over the next decade or so, all from frugality and savings from pensions and SS. Rather than park that in a measly savings account, I would like to at least offset inflation, presuming that happens again. ")

Part of our strategy involves living in cheaper locales where the USD is not the legal tender. But I really hate the thought of cash building up and just sitting there doing not much of anything. On the other hand, I also hate the thought of cash disappearing. I've been researching CD's and bonds, and given the anemic yields it hardly seems worth the effort. Blue chip dividend yields look much better, but then I'm back in equities.

Are there other choices out there I may be overlooking?

Part of our strategy involves living in cheaper locales where the USD is not the legal tender. But I really hate the thought of cash building up and just sitting there doing not much of anything. On the other hand, I also hate the thought of cash disappearing. I've been researching CD's and bonds, and given the anemic yields it hardly seems worth the effort. Blue chip dividend yields look much better, but then I'm back in equities.

Are there other choices out there I may be overlooking?