EvrClrx311

Full time employment: Posting here.

- Joined

- Feb 8, 2012

- Messages

- 648

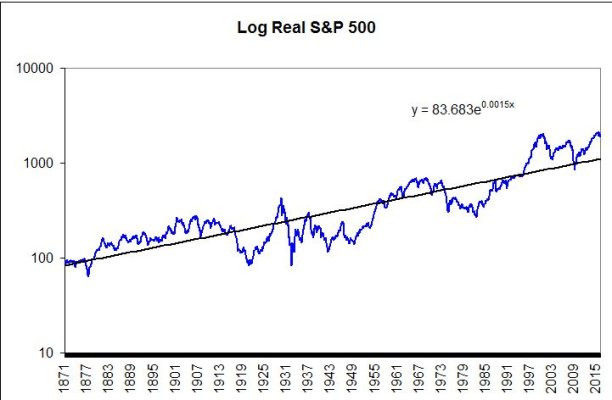

James O'Shaughnessy had a very good book (shares the title I used for this thread) that I was trying to dig up at home this weekend, about estimating ranges and how far from the long term trend we are... you know that 100 year linear line showing how the overall markets grow. You have to get outside the shorter term mindset to really appreciate it, because history does repeat and the long term tread has been fairly consistent on a macro level. Let me see if I can expand a bit backwards in time through my own research:

The things I'm most interested in are:

1) Where would the market sit today if we were straddling that long term 100+ year trend. Are we above or below it? When looking at the next 20 years, if we're below it then we're likely to have better than historical average returns moving forward, if we're above it then we're likely to have below average returns.

2) How far are we from the extremes... those times where the market peaked and hit rock bottoms. Projected forward, are we anywhere near one of them? What would the market have to be at today to be within one of those ranges?

Here goes...

Inflation adjusted Peaks and Troughs (source: MacroTrends)

Dow Jones 100 Year Historical Chart | MacroTrends...

Highs and Lows of the Dow the last 100 years that stand out:

(1915)Dec -- 2,276.88 <--- high

(1920)Dec ---- 877.21 <--- low

(1929)Jul -- 4,753.75 <--- high

(1932)May ---- 772.44 <--- low

(1937)Jan -- 3,099.01 <--- high

(1941)May -- 1,463.87 <--- low

(1966)Jan -- 7,315.35 <--- high

(1982)Jun -- 1,979.49 <--- low

(1999)Dec - 16,153.45 <--- high

(2009)Feb -- 7,875.17 <--- low

Sort of a crude start to this is to take the midway point of that first high/low cycle (1,577.05) and then also do the same at the other end (12,014.31). Then with some math we come up with the 90 year real return of the market... its trend upward. This is obviously crude, because maybe that high/low range didn't perfectly straddle the longer (200 year) average, however the further back you go the more accurate this will be. After all, we obviously got from there to now somehow, so that's a 100 year pressure... on the trend. If that makes sense.

$1,577.05 turns into $12,014.31 in 90 years with a 2.282% return. I'm guessing why this number is different from the often quoted 6-7% real return (real return being return after factoring out inflation) because it's missing the reinvestment of dividends in this MacroTrend chart. Beside the point however, it still gives us a baseline to do some math about where the DOW stands today within the ranges of deviation from the highs and lows in history. Because what we're after is taking this line and projecting it to the future...

Applying that 2.282% line to the above figures we see where the DOW would sit today if those peaks and lows were brought forward to today's time. Each of them straddling that long term line upwards for equities.

(1915)Dec -- 2,276.88 would be 22,236.20 today

(1920)Dec ---- 877.21 would be `7,652.93 today

(1929)Jul -- 4,753.75 would be 33,850.71 today

(1932)May ---- 772.44 would be `5,140.42 today

(1937)Jan -- 3,099.01 would be 18,423.01 today

(1942)May -- 1,463.87 would be `7,773.99 today

(1966)Jan -- 7,315.35 would be 22,604.54 today

(1982)Jun -- 1,979.49 would be `4,263.11 today

(1999)Dec - 16,153.45 would be 23,705.65 today

(2009)Feb -- 7,875.17 would be `9,222.62 today

We end up with an average high of 24,164.02 and and average low of 6,810.61... and average of it all being 15,487.31

Today's DOW is sitting about a thousand above that. So well within the middle range of where it could be historically, just a bit above it.

Getting to the Conclusion (assuming 3% inflation forward)...

10 years from now I'd expect the DOW to most likely be close to 25,912.97 with variances for extreme high and lows being 40,430.62 and 11,395.34 only if we are in one of those once a decade peaks of troughs about to head back up or down from it.

If we want to look at those 2026 figures in today dollars we are heading in the next decade for a 19,407.43 DOW with extreme edges being: 8,534.50 to 30,280.38

Please chime in if it appears I've missed something obvious")

-Eric

The things I'm most interested in are:

1) Where would the market sit today if we were straddling that long term 100+ year trend. Are we above or below it? When looking at the next 20 years, if we're below it then we're likely to have better than historical average returns moving forward, if we're above it then we're likely to have below average returns.

2) How far are we from the extremes... those times where the market peaked and hit rock bottoms. Projected forward, are we anywhere near one of them? What would the market have to be at today to be within one of those ranges?

Here goes...

Inflation adjusted Peaks and Troughs (source: MacroTrends)

Dow Jones 100 Year Historical Chart | MacroTrends...

Highs and Lows of the Dow the last 100 years that stand out:

(1915)Dec -- 2,276.88 <--- high

(1920)Dec ---- 877.21 <--- low

(1929)Jul -- 4,753.75 <--- high

(1932)May ---- 772.44 <--- low

(1937)Jan -- 3,099.01 <--- high

(1941)May -- 1,463.87 <--- low

(1966)Jan -- 7,315.35 <--- high

(1982)Jun -- 1,979.49 <--- low

(1999)Dec - 16,153.45 <--- high

(2009)Feb -- 7,875.17 <--- low

Sort of a crude start to this is to take the midway point of that first high/low cycle (1,577.05) and then also do the same at the other end (12,014.31). Then with some math we come up with the 90 year real return of the market... its trend upward. This is obviously crude, because maybe that high/low range didn't perfectly straddle the longer (200 year) average, however the further back you go the more accurate this will be. After all, we obviously got from there to now somehow, so that's a 100 year pressure... on the trend. If that makes sense.

$1,577.05 turns into $12,014.31 in 90 years with a 2.282% return. I'm guessing why this number is different from the often quoted 6-7% real return (real return being return after factoring out inflation) because it's missing the reinvestment of dividends in this MacroTrend chart. Beside the point however, it still gives us a baseline to do some math about where the DOW stands today within the ranges of deviation from the highs and lows in history. Because what we're after is taking this line and projecting it to the future...

Applying that 2.282% line to the above figures we see where the DOW would sit today if those peaks and lows were brought forward to today's time. Each of them straddling that long term line upwards for equities.

(1915)Dec -- 2,276.88 would be 22,236.20 today

(1920)Dec ---- 877.21 would be `7,652.93 today

(1929)Jul -- 4,753.75 would be 33,850.71 today

(1932)May ---- 772.44 would be `5,140.42 today

(1937)Jan -- 3,099.01 would be 18,423.01 today

(1942)May -- 1,463.87 would be `7,773.99 today

(1966)Jan -- 7,315.35 would be 22,604.54 today

(1982)Jun -- 1,979.49 would be `4,263.11 today

(1999)Dec - 16,153.45 would be 23,705.65 today

(2009)Feb -- 7,875.17 would be `9,222.62 today

We end up with an average high of 24,164.02 and and average low of 6,810.61... and average of it all being 15,487.31

Today's DOW is sitting about a thousand above that. So well within the middle range of where it could be historically, just a bit above it.

Getting to the Conclusion (assuming 3% inflation forward)...

10 years from now I'd expect the DOW to most likely be close to 25,912.97 with variances for extreme high and lows being 40,430.62 and 11,395.34 only if we are in one of those once a decade peaks of troughs about to head back up or down from it.

If we want to look at those 2026 figures in today dollars we are heading in the next decade for a 19,407.43 DOW with extreme edges being: 8,534.50 to 30,280.38

Please chime in if it appears I've missed something obvious

-Eric

Last edited: