aja8888

Moderator Emeritus

Born, you had me scared I was senile like Aja, thinking I was crazy it wasnt under par already, ha.

Born, you had me scared I was senile like Aja, thinking I was crazy it wasnt under par already, ha.

Born, you had me scared I was senile like Aja, thinking I was crazy it wasnt under par already, ha.

")

Hi, thank you all for the discussions, tips, and pointers. It has been a learning experience. For those who mainly want to buy and hold, have you considered the preferred ETFs especially in light of the recent drop and near recovery, it seems that the ETFs behaved as well as the individual preferreds...in the selloff and near recovery. There's that ~0.5% expense but can save time and effort in watching over a collection of say 15, 20+ individual stocks.

What say you? Thanks.

Hi, thank you all for the discussions, tips, and pointers. It has been a learning experience. For those who mainly want to buy and hold, have you considered the preferred ETFs especially in light of the recent drop and near recovery, it seems that the ETFs behaved as well as the individual preferreds...in the selloff and near recovery. There's that ~0.5% expense but can save time and effort in watching over a collection of say 15, 20+ individual stocks.

What say you? Thanks.

Thank you all. Yes, so I created a table tracking some individual preferreds and bought these: ni-b, pcg-a, pcg-d, sce-g, ms-e, kth, ppx, ipldp, chscm, chsco, sjij, gjh, ally-a, htlfp. Hard to get the really thinly traded however. Then I thought that's only 12 companies which is not that diversified. So should I look into buying another 10 or 20? That seems a lot of work. Maybe I'm just starting and this will become second nature.

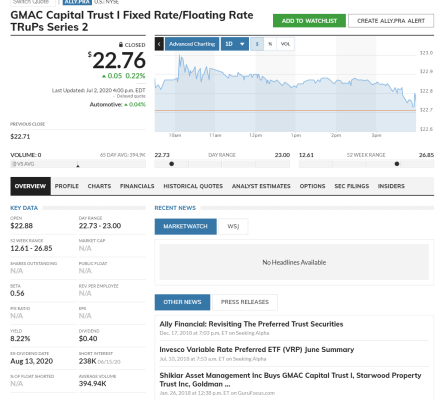

Mulligan, I'm looking at ALLY.PRA and have a couple questions.

First, Marketwatch shows the dividend at 40c/qtr... so that would be $1.60/yr.... but they show the yield at 8.22% at $22.76.

I get $1.60/$22.76 = 7.02%. Any idea where they are getting 8.22%?

Second, if the 3-month LIBOR goes negative would the negative LIBOR be used to set the dividend or would the negative LIBOR be floored at zero? I could paw through the offering documents but thought that you might know.

No one probably thought about that originally. Not sure US issues have any floor. But MBINO and MBINP have a zero floor. They are 6% and 7% coupon currently, then 3 mo Libor plus 4.569 and 4.065 respectively with 3mo Libor 0% floor, reset in 2024.PB, their math is just wrong. I checked a couple other sites and they mirrored your math. Unfortunately, if Libor goes negative they would subtract that from the adjustment part of the yield. This is why a few preferreds (especially many Canadian ones) have instituted “yield floors” or capping Libor or TBill at zero. But most of these old ones dont.

The prescribed Dodd-Frank Act capital actions include estimated Q1 2020 capital actions taken by the Company, and for quarters two through nine of

the test horizon, no issuance of regulatory capital other than assumed issuance of common stock for employee compensation or in connection with a

planned merger or acquisition; payments of common stock dividends equal to the quarterly average dollar amount paid by the Company from Q2 2019

through Q1 2020; payments on all other regulatory capital instruments equal to the stated dividend, interest, or principal due during the quarter; and no

capital redemptions or repurchases.

Thanks PB. I did do a web search before I posted but I didn't come across the actual stress test report. Skimming through it I found the following:

So it looks like they won't be required to cut the Preferred dividend. That's my good news of the day!

To the best of my knowledge, as long as a company pays a dividend on their common, even if 1 cent, they have to make the dividend payments on their preferred issues.

.jpg")

.jpg") ).

).You used the right words...gamble especially. Usually, you do prefs for divvy. THose are suspended. Now, buying back at $9 is a dangerous move and AHT could be headed to BK. I'd take what they give and bail. And they limit what they give. Take what you can get and try HMLP-A for a gamble...not "really" a gamble as all is contracted. But, contracts are fungible (didnt think they are SUPPOSED to be, I should let my lawyers know that! HaHa!

People thought the PCG preferred's that Muli posted months ago was risky. I did pretty well on those.  Sometimes an educated gamble is worth the risk. Sometimes it's not.

Sometimes an educated gamble is worth the risk. Sometimes it's not.