Mulligan

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

- Joined

- May 3, 2009

- Messages

- 9,343

Preferred Stock Investing-The Good , The Bad and The In Between

Be glad too... It was basically an "uncallable bond". This means if they want to call it they have to pay you all the interest up to 2028 maturity "to make you whole on the purchase". So par plus interest next 12 years worth...which means they wont call unless it is of real importance to them. So in 2028, ( if still a viable company) they will pay me $1000 for each of the 3 bonds I bought at $960 or so ( forgot already, ha!). Plus get the note interest every six months until then.

Sent from my iPad using Tapatalk

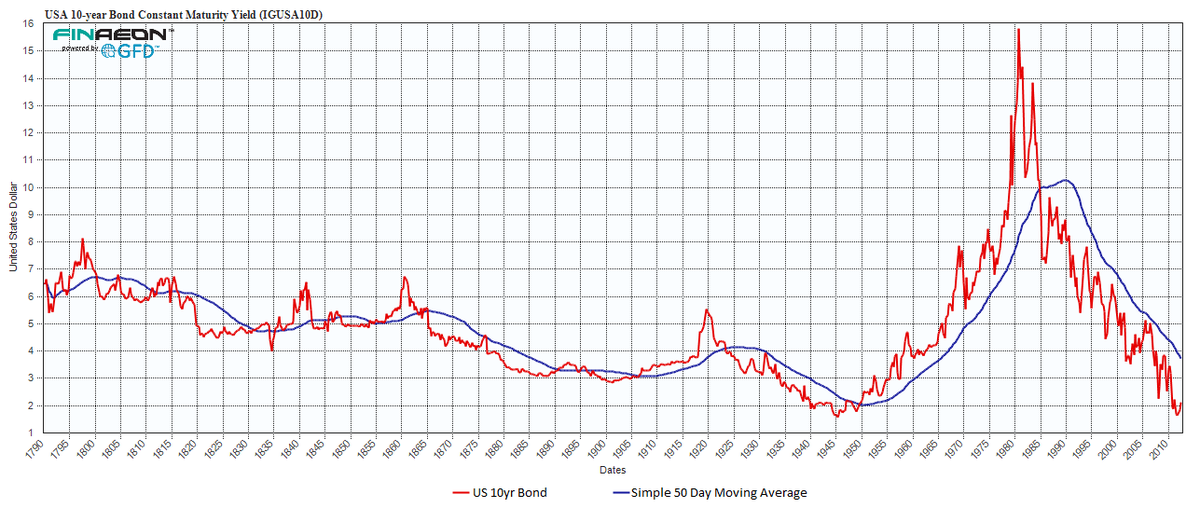

Hope you don't mind, but what does the bold line mean ?

Cincinnati Bell Tel Co Deb 6.3%28, Make Whole Call

Be glad too... It was basically an "uncallable bond". This means if they want to call it they have to pay you all the interest up to 2028 maturity "to make you whole on the purchase". So par plus interest next 12 years worth...which means they wont call unless it is of real importance to them. So in 2028, ( if still a viable company) they will pay me $1000 for each of the 3 bonds I bought at $960 or so ( forgot already, ha!). Plus get the note interest every six months until then.

Sent from my iPad using Tapatalk