|

|

04-09-2016, 05:44 AM

04-09-2016, 05:44 AM

|

#101

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Posts: 5,381

|

Quote: Quote:

Originally Posted by OrcasIslandBound

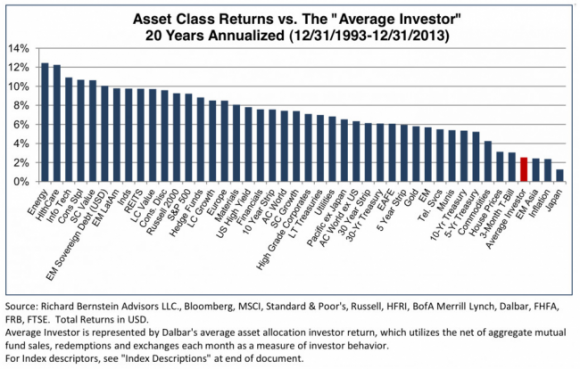

Why does the "average" investor earn just 2%? It is because they are market timers.

|

I think that's the implication. This is what it says at the bottom of the chart:

Quote:

|

Average investor is represented by Dalbars average asset allocation investor return, which utilizes the net of aggregate mutual fund sales, redemptions and exchanges each month as a measure of investor behavior

|

__________________

Retired early, traveling perpetually.

|

|

|

|

Join the #1 Early Retirement and Financial Independence Forum Today - It's Totally Free!

Are you planning to be financially independent as early as possible so you can live life on your own terms? Discuss successful investing strategies, asset allocation models, tax strategies and other related topics in our online forum community. Our members range from young folks just starting their journey to financial independence, military retirees and even multimillionaires. No matter where you fit in you'll find that Early-Retirement.org is a great community to join. Best of all it's totally FREE!

You are currently viewing our boards as a guest so you have limited access to our community. Please take the time to register and you will gain a lot of great new features including; the ability to participate in discussions, network with our members, see fewer ads, upload photographs, create a retirement blog, send private messages and so much, much more!

|

|

04-09-2016, 06:13 AM

|

#102

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Posts: 5,381

|

Quote:

Originally Posted by OrcasIslandBound

Why does the "average" investor earn just 2%? It is because they are market timers.

|

Here's more from Dalbar . . .

Quote:

In 30 years of monthly investor returns, DALBAR found that equity investors underperformed the S&P 500 to the greatest extent in October, 2008. In this month, equity investors lost 24.21% compared to an S&P loss of 16.80% for a net underperformance of 7.41 percentage points.

The next greatest underperformance occurred in March, 2000, when the S&P surged 9.78% but investors took home only 3.72% for an underperformance of 6.06%.

The underperformance results from bad investor decisions at critical points, the first in the face of severe market declines and the second when the equity market surged.

|

Having said that, Dalbar is a financial services research firm and seems to promote this research as showing the benefits a financial advisor can bring to individual investors.

__________________

Retired early, traveling perpetually.

|

|

|

|

|

04-09-2016, 06:28 AM

|

#103

|

|

Administrator

Join Date: Jan 2008

Location: Chicagoland

Posts: 40,726

|

Quote:

Originally Posted by OrcasIslandBound

Why does the "average" investor earn just 2%? It is because they are market timers.

|

Timing and performance chasing. Morningstar tracks and reports on this, and IIRC their view is that investors chase performance and buy into mutual funds after that have had periods of good performance.

|

|

|

|

|

04-09-2016, 08:47 AM

|

#104

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2008

Posts: 35,712

|

Quote:

|

... The next greatest underperformance occurred in March, 2000, when the S&P surged 9.78% but investors took home only 3.72% for an underperformance of 6.06%.

|

The date of March 2000 caught my eyes. This statement by itself is extremely misleading. I could have written similarly "bond investors completely missed out on the wonderful stock return".

The truth is that the S&P did surge from 1366 on 3/1/2000 to 1527 on 3/23/2003. That's 12% increase. But it gave it all up soon, and was back down in April, and continued to slide down to 800 in late 2002. In fact, it climbed back up to the old high in 2007, and crashed even harder in 2009, and only reclaimed the 1500 level again in Jan 2013. That's 13 years later. Surely, it paid a 2% dividend in that 13 years, but that is barely enough to cancel out inflation.

Meanwhile, a non-indexer like Wellesley turned $10K in 3/1/2000 to $27.2K on Jan 2013 with dividend reinvested. Cumulative inflation was 35% in that period, leaving it with a gain of 2X.

__________________

"Old age is the most unexpected of all things that happen to a man" -- Leon Trotsky (1879-1940)

"Those Who Can Make You Believe Absurdities Can Make You Commit Atrocities" - Voltaire (1694-1778)

|

|

|

|

|

04-09-2016, 08:56 AM

|

#105

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Posts: 5,381

|

Quote:

Originally Posted by NW-Bound

Meanwhile, a non-indexer like Wellesley turned $10K in 3/1/2000 to $27.2K on Jan 2013 with dividend reinvested. Cumulative inflation was 35% in that period, leaving it with a gain of 2X.

|

I don't think Dalbar's argument is about indexing. It's about the way individual investors are terrible at timing the market. They pile into stocks at the tail end of rallies and then bail out after the market crashes.

That kind of behavior will hurt performance regardless of what investment vehicle you choose.

__________________

Retired early, traveling perpetually.

|

|

|

|

|

04-09-2016, 09:04 AM

|

#106

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Jul 2008

Posts: 35,712

|

Of course I agree with the above. If one piles into a single stock or sector, he can make out like bandits and retire early, or has only SS to live on in his old age. There's a lot of luck involved when you are concentrated.

But if he is reasonably diversified, does not chase performance, bails out or piles in at the same time as the Jones, he will do OK whether he indexes or not. If he does not index, some years he will do better, some years he will do worse. I think people take indexing as godsend, something that guarantees they will make money. The last 15 years show it is not true.

Anyway, about the herd mentality, some writers have suggested that it should be easy to beat the market. How? If it is true that the average investor trails the market, why don't we just do the reverse of what he does?

__________________

"Old age is the most unexpected of all things that happen to a man" -- Leon Trotsky (1879-1940)

"Those Who Can Make You Believe Absurdities Can Make You Commit Atrocities" - Voltaire (1694-1778)

|

|

|

|

|

04-09-2016, 09:21 AM

|

#107

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,899

|

Quote:

Originally Posted by Senator

|

Thanks for that chart - it would be interesting to see how that looks over sliding 5 year periods. There's a 'periodic table' like chart that gets posted from time to time, it shows the different sector performance year by year.

But it pretty much confirms me feelings, I'm not very interested in trying to chase a sector. The performance of a simply S&P500 index seems likely to do as well as anything. So I'm not going to worry about which index I'm invested in, or have any concern whatsoever that there are so many of them.

-ERD50

|

|

|

|

|

04-09-2016, 09:49 AM

|

#108

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Posts: 5,381

|

Quote:

Originally Posted by NW-Bound

But if he is reasonably diversified, does not chase performance, bails out or piles in at the same time as the Jones, he will do OK whether he indexes or not.

|

I think most folks would agree with that although some may quibble over how one defines "doing OK."

It is possible to be in a fund that's pretty terrible. This large-cap Blackrock fund underperformed the S&P by 350bp per year over the last ten years.

Investors in that fund (they still have $1.6B under management) are up close to 40% over 10 years, so they can claim they did "OK." But had they stuck to a simple index they'd be up 95% - or more than 2x better off.

__________________

Retired early, traveling perpetually.

|

|

|

|

|

04-09-2016, 10:24 AM

|

#109

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Posts: 5,381

|

Quote:

Originally Posted by NW-Bound

Anyway, about the herd mentality, some writers have suggested that it should be easy to beat the market. How? If it is true that the average investor trails the market, why don't we just do the reverse of what he does?

|

I didn't think too deeply about the Dalbar report, and there isn't a way to get a copy for free to see the methodology, but you raise a good point.

If some class of investors systematically underperform the market, then another class (or classes) of investor must systematically outperform. Every single time an "individual investor" sells, someone else buys. And every time the II buys, someone else sells.

Now one way investors underperform is by paying fees. That Blackrock fund linked above charges 1.97%. That fee is going to systematically hurt performance. But that isn't what Dalbar's chart purports to show.

So my now revised opinion is that Dalbar's methodology probably doesn't yield the results they claim it does.

__________________

Retired early, traveling perpetually.

|

|

|

|

|

04-09-2016, 10:31 AM

|

#110

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2005

Location: Chicago

Posts: 13,186

|

Quote:

Originally Posted by DrRoy

This is right. Most of the discussion here is in regard to the S&P 500 index, which is by far the most used index target for ETF's and funds. The broad discussion also presumes buy and hold. Look at Senator's post yesterday with the chart. If one is using an array of narrow indexes, there is likely some trading going on as well, and overall return is likely to suffer over the long haul.

|

OK, but this seems to fly in the face of having a "diverse portfolio." I always thought it was wise to spread your investments over a range of asset classes beyond the S&P 500. You know, international, perhaps a bit of small and mid cap, etc.

So, ALL your equity investments are in a S&P 500 index such as SPY, VOO or similar?

__________________

"I wasn't born blue blood. I was born blue-collar." John Wort Hannam

|

|

|

|

|

04-09-2016, 10:36 AM

|

#111

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2006

Posts: 2,844

|

Quote:

Originally Posted by Gone4Good

I didn't think too deeply about the Dalbar report, and there isn't a way to get a copy for free to see the methodology, but you raise a good point.

If some class of investors systematically underperform the market, then another class (or classes) of investor must systematically outperform. Every single time an "individual investor" sells, someone else buys. And every time the II buys, someone else sells.

Now one way investors underperform is by paying fees. That Blackrock fund linked above charges 1.97%. That fee is going to systematically hurt performance. But that isn't what Dalbar's chart purports to show.

So my now revised opinion is that Dalbar's methodology probably doesn't yield the results they claim it does.

|

This statement is a common fallacy, one person underperforming the market does not create another person outperforming the market. Whenever a person buys an he will in grand total earn the market, only the person selling will either outperform or underperform the market depending on the relative value of what he holds in return for selling. The market continues to earn the market. This is why a great percentage of investors can earn less than the market, particularly as the market reaches all time highs, the lack of being in stocks when they are at a high make it unlikely to earn the market.

Fees are a rake, similar to the take in Vegas by poker tables and cause the overall return to be less than the market by design. As these fees have fallen over the years for index funds the market is easier to earn in an index fund but a decided disadvantage for a managed fund. Any other variance from the market is called “tracking error” for index funds but “performance” for managed funds.

The combination of cash balances and higher fees, when compared near tops of stock market will cause the average managed fund to underperform the index. Higher fees are the hardest hurdle to climb the underperformance due to cash balances is really just a reduced risk overall for managed funds.

|

|

|

|

|

04-09-2016, 10:41 AM

|

#112

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2005

Location: Chicago

Posts: 13,186

|

Quote:

Originally Posted by ERD50

Thanks for that chart - it would be interesting to see how that looks over sliding 5 year periods. There's a 'periodic table' like chart that gets posted from time to time, it shows the different sector performance year by year.

But it pretty much confirms me feelings, I'm not very interested in trying to chase a sector. The performance of a simply S&P500 index seems likely to do as well as anything. So I'm not going to worry about which index I'm invested in, or have any concern whatsoever that there are so many of them.

-ERD50

|

Could the advantage of having a diversified portfolio, as opposed to going 100% S&P 500, be less variation in performance over time. That is, while it may be true that, as you say, "a simply S&P500 index seems likely to do as well as anything" perhaps at any given point in time a diversified portfolio might exhibit less variability. For example, small caps are making hay while large caps are down a bit..... Perhaps during the withdrawal stage some equity diversification beyond domestic large caps would give you some flexibility.

Also, did you really literally mean what you said:

Quote:

|

So I'm not going to worry about which index I'm invested in, or have any concern whatsoever that there are so many of them.

|

For example, I have a fraction of one percent of my equities in an etf that follows an energy index right now and, wow, I'm gettin' burned. Ouch! You'd be OK 100% in that? Or did you mean you're not going to worry about which index you're invested in as long as it's the S&P500?

__________________

"I wasn't born blue blood. I was born blue-collar." John Wort Hannam

|

|

|

|

|

04-09-2016, 10:49 AM

|

#113

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2006

Posts: 2,844

|

Quote:

Originally Posted by Gone4Good

I think most folks would agree with that although some may quibble over how one defines "doing OK."

It is possible to be in a fund that's pretty terrible. This large-cap Blackrock fund underperformed the S&P by 350bp per year over the last ten years.

Investors in that fund (they still have $1.6B under management) are up close to 40% over 10 years, so they can claim they did "OK." But had they stuck to a simple index they'd be up 95% - or more than 2x better off. |

Most likely this is trapped 401K money where Blackrock is paying (or should I say defraying all company expenses) the company to let them manage their 401K funds, hence the astronomical 2% expense fees. Since many companies do not allow their employees any other choices this is what they are left with,

See this for what Blackrock fees do to a 401K

Forbes Welcome

|

|

|

|

|

04-09-2016, 11:00 AM

|

#114

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,899

|

Quote:

Originally Posted by youbet

Could the advantage of having a diversified portfolio, as opposed to going 100% S&P 500, be less variation in performance over time. That is, while it may be true that, as you say, "a simply S&P500 index seems likely to do as well as anything" perhaps at any given point in time a diversified portfolio might exhibit less variability. For example, small caps are making hay while large caps are down a bit..... Perhaps during the withdrawal stage some equity diversification beyond domestic large caps would give you some flexibility. ...

|

Yes, I suppose there could be some advantage in withdrawals if there is enough cyclic non-correlation across some sectors with similar long term results. It would be an interesting thing to investigate, though I'm guessing any advantage would be small. But still maybe some small, but not insignificant $'s in the long run? A 20 year re-balancing (after withdraws) study would be interesting!

Quote:

Originally Posted by youbet

Also, did you really literally mean what you said:

For example, I have a fraction of one percent of my equities in an etf that follows an energy index right now and, wow, I'm gettin' burned. Ouch! You'd be OK 100% in that? Or did you mean you're not going to worry about which index you're invested in as long as it's the S&P500?

|

Right, I really meant compared to the S&P500, or other broad based index. I'm personally not interested in sector plays.

-ERD50

|

|

|

|

|

04-09-2016, 11:00 AM

|

#115

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2007

Posts: 14,328

|

Quote:

Originally Posted by Running_Man

.............

See this for what Blackrock fees do to a 401K

Forbes Welcome |

Site won't let you in unless you turn off Adblock. Their loss.

|

|

|

|

|

04-09-2016, 11:04 AM

|

#116

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2006

Posts: 2,844

|

Finally, when people are looking at stock prices and calling the “average investor” as being a market timer, the biggest market timers and underperformers in the world are companies themselves that in total are the “market".

By definition at peaks in the market while they are going great guns, they are buying back stock at record levels, as stock prices fall companies are forced to stop buying and then in many cases issue equities at a market low. (sometimes this is referred to as re-capitalizing) This is what happened to most banks in 2007-2009.

Chevron one company alone bought 5 billion dollars in 2014 of it’s own shares back (should not they have just bought an index?) most at $120 a share an all time high --- in 2015 with the stock down 33% they halted all buybacks in a widely hailed “prudent” move to conserve cash.

|

|

|

|

|

04-09-2016, 11:27 AM

|

#117

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Mar 2005

Location: Chicago

Posts: 13,186

|

QQ

Quote:

Originally Posted by ERD50

Right, I really meant compared to the S&P500, or other broad based index. I'm personally not interested in sector plays.

|

OK. So I'll interpret that as " So I'm not going to worry about which index I'm invested in" as long as the index I'm invested in is exclusively the S&P500.

Sorry for the confusion. Your wording threw me off. You weren't going to worry about which index you're invested in. But the index has to be the S&P500 (by market weighting I presume since that's most common).

Well, as I've mentioned a number of times, my portfolio is dominated by a low cost, TSM fund I've held for many years. That fund is dominated by large caps and performs very similarly to the S&P500 but it does include a smidgen of mid and small caps so that it reflects the total domestic market instead of just the large caps. To see a comparison, just do a quick compare of VTI to VOO. Almost identical.

But, I also include an allocation of international, primarily developed but also just a bit of emerging. And once in a while I hold some QQQ, but not right now.

Maybe I need to dig in and see if this diversification is actually hurting my aggregate performance and I'd be better off just 100% VOO as you are. Although, I'm not likely to sell the TSM fund as the majority of its value is cap gains and I wouldn't want to face that tax right now.

__________________

"I wasn't born blue blood. I was born blue-collar." John Wort Hannam

|

|

|

|

|

04-09-2016, 11:29 AM

|

#118

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Posts: 5,381

|

Quote:

Originally Posted by Running_Man

This statement is a common fallacy, one person underperforming the market does not create another person outperforming the market. Whenever a person buys an he will in grand total earn the market, only the person selling will either outperform or underperform the market depending on the relative value of what he holds in return for selling.

|

It's not a fallacy. The reason you think so is that you're mixing and matching how you define the word "market."

"The person selling will either outperform or underperform the market depending on the relative value of what he holds in return for selling."

How can someone hold something that isn't part of the market? And where did he buy it from?

He bought it from a seller, who now owns less of that asset and more of something else instead. All of these assets together are "the market."

Now we can define "the market" narrowly or we can define it broadly but we have to define it consistently if we want to make any sense of anything.

What you seem to be doing is defining "the market" narrowly as equities but then also trying to add the results from owning other asset classes outside the equity universe. If you want to include the results from owning those other assets, that's fine. But then you also have to include them in your definition of the market. Once you do that, we're back to saying that one person can't outperform the market unless someone else underperforms that same market.

So what you've identified isn't a fallacy but an inconsistently applied definition of your market universe.

__________________

Retired early, traveling perpetually.

|

|

|

|

|

04-09-2016, 11:59 AM

|

#119

|

|

Give me a museum and I'll fill it. (Picasso)

Give me a forum ...

Join Date: Sep 2005

Location: Northern IL

Posts: 26,899

|

Quote:

Originally Posted by youbet

...

Sorry for the confusion. Your wording threw me off. You weren't going to worry about which index you're invested in. But the index has to be the S&P500 (by market weighting I presume since that's most common).

... To see a comparison, just do a quick compare of VTI to VOO. Almost identical.

....

Maybe I need to dig in and see if this diversification is actually hurting my aggregate performance and I'd be better off just 100% VOO. Although, I'm not likely to sell the TSM fund as the majority of its value is cap gains and I wouldn't want to face that tax right now.

|

My wording was confusing. I sort of mentally default to S&P500 as being representative of 'the market', it isn't really, but easy and close enough for my purposes.

It just looks like diversifying past the S&P500 , while technically the more correct view of 'the market', is just hitting diminishing returns in terms of having any real effect. No harm in trying, adding a few more funds to pick up those extra categories is near zero cost. And rotating withdraws to pull from the highest just may provide a very modest boost? I have not bothered (yet), but it may be my (small?) loss?

-ERD50

|

|

|

|

|

04-09-2016, 12:23 PM

|

#120

|

|

Thinks s/he gets paid by the post

Join Date: Sep 2006

Posts: 2,844

|

Quote:

Originally Posted by Gone4Good

It's not a fallacy. The reason you think so is that you're mixing and matching how you define the word "market."

"The person selling will either outperform or underperform the market depending on the relative value of what he holds in return for selling."

How can someone hold something that isn't part of the market?

If we define "market" narrowly to mean domestic equities, then when one person buys domestic equities another person sells domestic equities. Whatever returns happen or don't happen outside the domestic equity market isn't relevant when comparing returns within our defined market.

If we define "market" broadly to mean all investable assets, it's still true that when one person buys investable assets someone else will sell investable assets. And it's just as true that one person can't outperform the market for all investable assets unless someone else underperforms that same market.

What you seem to be doing is defining the "market" narrowly as equities but then also trying to add the results from owning other asset classes outside the equity universe. If you want to include the results from owning those other assets, that's fine. But then you also have to include them in your definition of the market. Once you do that, we're back to saying that one person can't outperform unless someone else underperforms.

So what you've identified isn't a fallacy but an inconsistently applied definition of your market universe.

|

Your implication that a market is in principle the Law of Conservation is simply not true, value of equities unlike energy can be created and or destroyed without being transferred, it happens all the time.

|

|

|

|

|

|

|

Currently Active Users Viewing This Thread: 1 (0 members and 1 guests)

|

|

|

Posting Rules

Posting Rules

|

You may not post new threads

You may not post replies

You may not post attachments

You may not edit your posts

HTML code is Off

|

|

|

|

» Recent Threads

» Recent Threads

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

» Quick Links

|

|

|

Linear Mode

Linear Mode