antmary

Full time employment: Posting here.

I am very relieved. I have a child with an eye injury from 10 years ago. Thankfully, she can't be denied treatment for a "preexisting condition."

samclem said:It looks like your policy might not meet the requirements of the new law (I think your deductible is too high, and you'd need to check to assure it includes all the required "preventative" services mandated by the legislation.) Anyway, if you insurance company raises your rates in order to include the new bells and whistles, the "good news" is that you'll be among those who save money by dropping your insurance and just paying the tax. Of course, you wouldn't have insurance then. But you can buy it the day you need it.

You're probably covered anyway unless PPACA voids EMTALA...Perhaps I should plan to game the system and drop health insurance on 1/1/2014, pay the penalty and then buy guaranteed issued insurance if I have a health event. I think the way it works that I would only be screwed if I had such an immediate health event that I couldn't get the time to buy the insurance (liek a heart attack requiring immediate surgery).

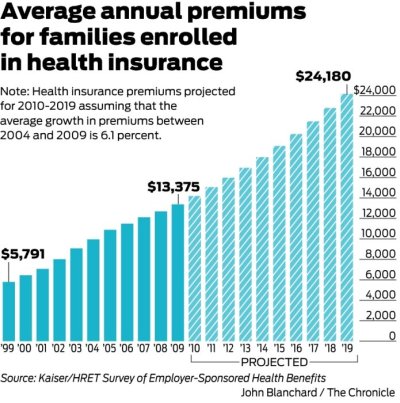

As I added above, you're paying $864/yr. That's totally unheard of based on everything I have ever read about HI for an unsubsidized plan even high deductible.To say you're an exception may be a gross understatement.I wish! I doubt I will ever have $700k in assets before I die let alone income! You missed a follow up post, Midpack. My premium is only $72 a month for a $5500 individual plan deductible through Anthem. $7 million max lifetime.

Midpack said:Congrats on your extreme wealth, using income as the measure. If your HI costs $7,000/yr (which is dirt cheap from what I've seen), your income would have to be more than $700,000/yr (at 1% penalty in 2014) for the "premium cost is actually cheaper." I must be missing something...

That's $864/yr. Anthem quoted DW (age 56) and I (57) $500-600 month for a high deductible plan and we're in relatively excellent health. Let's just say your plan is unheard of for an unsubsidized policy and leave it at that.

There's some uncertainty about how "sturdy" the grandfathering will be. From the Congressional Research Service:No, the plan was bought prior to the healthcare act being passed so I am exempted. It certainly seems that health insurance is a lot cheaper in MO, than other places. But it appears the reason has been the high rejection rate of applicants here. I THINK that anyone who has a policy purchased prior to the act it exempted from all of the provisions. For example I have a lifetime cap of $7 million and do not get a free preventive care physical either. I will gladly give those up if my plan stays exempted.

PPACA is silent on the question about whether changes to a plan or coverage would make it a new plan. It is not clear whether changes to covered benefits, cost-sharing requirements, actuarial value, or other plan features would be allowed under a grandfathered plan. Also, PPACA does not address instances when there are changes to the insurance carrier offering the plan (e.g., new corporate owner); it is not clear whether organizational changes would make grandfathered plans into new plans.

Ours is closer to $700/mo currently, for retiree (both) under my former employer plan.DH and I currently pay nearly $600 a month for health insurance and this is as a full retiree under the Virginia Retirement System. I can only hope this means we'll have a more affordable alternative but somehow doubt it.

Yep, in their rush to "scoop" the competition, as soon as they saw Roberts' opinion denying the use of the Commerce Clause as justification, they assumed that meant Roberts voting it down. They had no idea that he'd soon uphold it on other grounds.I suspect that everyone was focused on the commerce clause and item 2 above indicates that the individual mandate is not constitutional under the commerce clause and then the tax argument sneaked in the back door.

It would require an act of Congress to change the new laws. Right now under PPACA this is not allowed to the best of my knowledge.To prevent people from trying to game the new law by going without insurance, paying the penalty/tax, then buying coverage just when they get sick, could there be a law change which does somethign similar to what is done in the homeowners insurance market: I believe a homeowner has to buy insurance at least 30 days before he can collect on certain types of damage to prevent someone who is without insurance from seeing weather reports of a hurricane approaching and quickly buying a policy. This required lead time could be made longer in the health insurance area but the principle is the same.

I think this is unrealistic: What Congress is going to pass these measures? The legislators who opposed the present law have announced their intention to get it repealed (not to bandage up its deficiencies), and the legislators who voted for it are unlikely to do anything that would, in effect, deny people the ability to buy insurance.To prevent people from trying to game the new law by going without insurance, paying the penalty/tax, then buying coverage just when they get sick, could there be a law change which does somethign similar to what is done in the homeowners insurance market: I believe a homeowner has to buy insurance at least 30 days before he can collect on certain types of damage to prevent someone who is without insurance from seeing weather reports of a hurricane approaching and quickly buying a policy. This required lead time could be made longer in the health insurance area but the principle is the same.

I think this is unrealistic: What Congress is going to pass these measures? The legislators who opposed the present law have announced their intention to get it repealed (not to bandage up its deficiencies), and the legislators who voted for it are unlikely to do anything that would, in effect, deny people the ability to buy insurance.

Nope. It needed to be right from the start.

To prevent people from trying to game the new law by going without insurance, paying the penalty/tax, then buying coverage just when they get sick, could there be a law change which does somethign similar to what is done in the homeowners insurance market: I believe a homeowner has to buy insurance at least 30 days before he can collect on certain types of damage to prevent someone who is without insurance from seeing weather reports of a hurricane approaching and quickly buying a policy. This required lead time could be made longer in the health insurance area but the principle is the same.

Guess we need to move to MO. Seems odd that everyone else seems to be paying $500-700/mo for high deductible health insurance. What makes MO so different?Not unheard of, Midpack. Anyone in MO can get this provided they are healthy. Here is my plan copied right off ehealthinsurance. It is now $76. The healthcare act only raised it $4.

Midpack said:Guess we need to move to MO. Seems odd that everyone else seems to be paying $500-700/mo for high deductible health insurance. What makes MO so different?

")

I don't get it ($864/yrI looked at an earlier posted link in this thread and it appeared MO insurance companies were rejecting between 35%- 50% of applicants for the various plans. Maybe that was the reason. If I was one of those people, I wouldn't be too pleased. All I know was when I retired I had the option to stay on my group plan and pay the $500 monthly premium and $1k deductible or get on an individual plan. Several of my friends who retired at the same time all jumped on individual plans because they were so much cheaper. None of us got rejected so I don't know what the criteria for rejection was. I did notice the premiums vary from county to county, but there isn't a hospital within 20 miles of where I live so nearby quality care isn't the reason. Maybe its cheaper because they think I will die before I can get medical care.

), but good for you and your friends. It will cost DW and I approaching 10X what you're paying...Midpack said:I don't get it ($864/yr

I looked at an earlier posted link in this thread and it appeared MO insurance companies were rejecting between 35%- 50% of applicants for the various plans. Maybe that was the reason. If I was one of those people, I wouldn't be too pleased. All I know was when I retired I had the option to stay on my group plan and pay the $500 monthly premium and $1k deductible or get on an individual plan. Several of my friends who retired at the same time all jumped on individual plans because they were so much cheaper. None of us got rejected so I don't know what the criteria for rejection was. I did notice the premiums vary from county to county, but there isn't a hospital within 20 miles of where I live so nearby quality care isn't the reason. Maybe its cheaper because they think I will die before I can get medical care.

I just had a thought: Since SS income is generally included in the income calculation for determining the subsidy for health insurance, and since the premiums from age 62-64 will be the highest, wouldn't this potentially make a strong argument for waiting to take SS until you are Medicare-eligible? A significant portion of the SS you'd get from age 62-64 would be lost to the reduction in subsidy anyway so you might as well wait until 65* when you will be on Medicare and don't have to worry about private insurance matters any more -- or about the loss of the subsidy.

* -- Or whatever Medicare eligibility age younger folks are going to be moved to. And obviously this likely won't apply to those of you who are blessed enough to have (former) employer-subsidized health insurance in retirement.

I just had a thought: Since SS income is generally included in the income calculation for determining the subsidy for health insurance, and since the premiums from age 62-64 will be the highest, wouldn't this potentially make a strong argument for waiting to take SS until you are Medicare-eligible? A significant portion of the SS you'd get from age 62-64 would be lost to the reduction in subsidy anyway so you might as well wait until 65* when you will be on Medicare and don't have to worry about private insurance matters any more -- or about the loss of the subsidy.

* -- Or whatever Medicare eligibility age younger folks are going to be moved to. And obviously this likely won't apply to those of you who are blessed enough to have (former) employer-subsidized health insurance in retirement.

+2, great observation, though I am also planning to wait until I'm 70. All the more reason if this plays out as it appears.I just had a thought: Since SS income is generally included in the income calculation for determining the subsidy for health insurance, and since the premiums from age 62-64 will be the highest, wouldn't this potentially make a strong argument for waiting to take SS until you are Medicare-eligible? A significant portion of the SS you'd get from age 62-64 would be lost to the reduction in subsidy anyway so you might as well wait until 65* when you will be on Medicare and don't have to worry about private insurance matters any more -- or about the loss of the subsidy.

* -- Or whatever Medicare eligibility age younger folks are going to be moved to. And obviously this likely won't apply to those of you who are blessed enough to have (former) employer-subsidized health insurance in retirement.