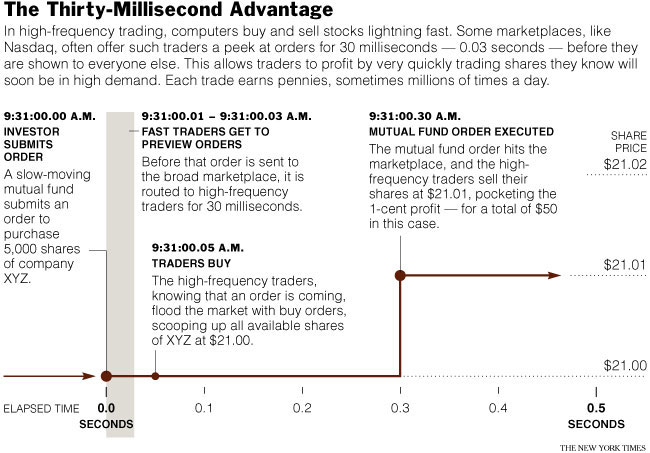

It looks like several legislators are working on a proposal to tax equity trades.

Here's more.

I assume the "0.25 tax" is really 0.25%. There's no indication in the article of whether mutual funds and ETFs would be included in such a atax.

Anyway, this is at the very early stages and it probably won't happen. But it's an indication of things to come. I expect taxation of non-wage income to become a new growth industry.

House Democrats are clashing over a draft bill that would tax financial transactions in an effort to raise $150 billion per year.

Democratic Reps. Carolyn Maloney (N.Y.), Mike McMahon (N.Y.) and Debbie Halvorson (Ill.) are circulating a letter opposed to the stock transaction tax idea. They're squaring off against the tax's main supporters, including Reps. Peter DeFazio (Ore.) and Ed Perlmutter (Colo.).

The 0.25 tax would be levied on stock, futures, derivatives and other transactions. The financial industry strongly opposes the tax and argues it would hurt the economy as it begins to recover.

Here's more.

I assume the "0.25 tax" is really 0.25%. There's no indication in the article of whether mutual funds and ETFs would be included in such a atax.

Anyway, this is at the very early stages and it probably won't happen. But it's an indication of things to come. I expect taxation of non-wage income to become a new growth industry.