Chuckanut

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

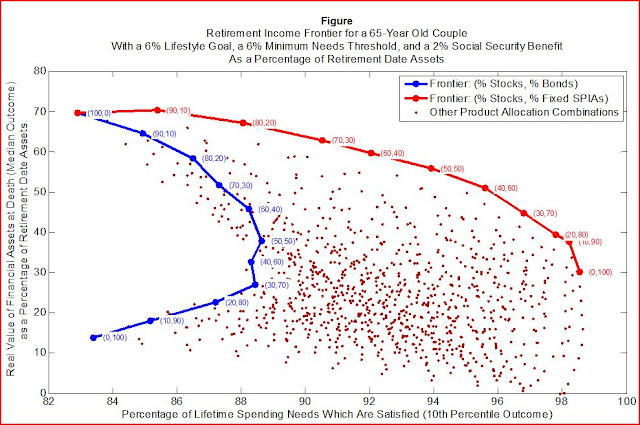

Here is an interesting article on how to best achieve retirement income goals for many people. Interestingly, the author finds that a combination of stocks and SPIAs works much better than stocks and bonds. Food for thought.

Retirement Researcher Blog: An Efficient Frontier for Retirement Income

Retirement Researcher Blog: An Efficient Frontier for Retirement Income