slowsaver

Recycles dryer sheets

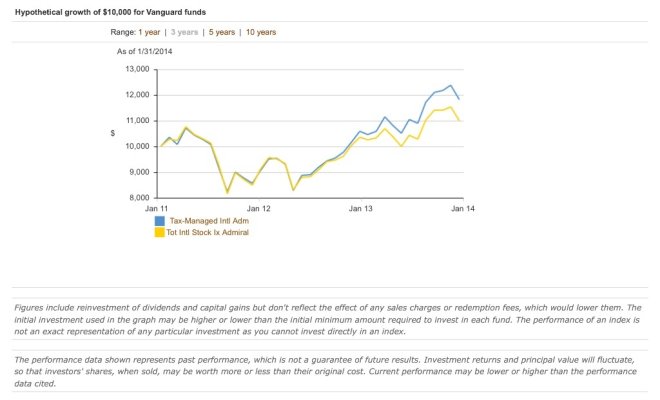

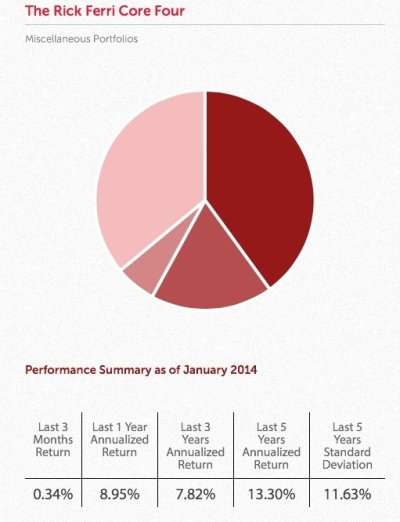

Does anybody have any thoughts (or links to articles) discussing Core-4 asset allocation? Here's a quick description: Lazy portfolios - Bogleheads

I can find plenty of articles describing what it is, but not many counter-arguments or analysis about how it's performed so-far, etc. Thanks!

I can find plenty of articles describing what it is, but not many counter-arguments or analysis about how it's performed so-far, etc. Thanks!

")