mickeyd

Give me a museum and I'll fill it. (Picasso) Give me a forum ...

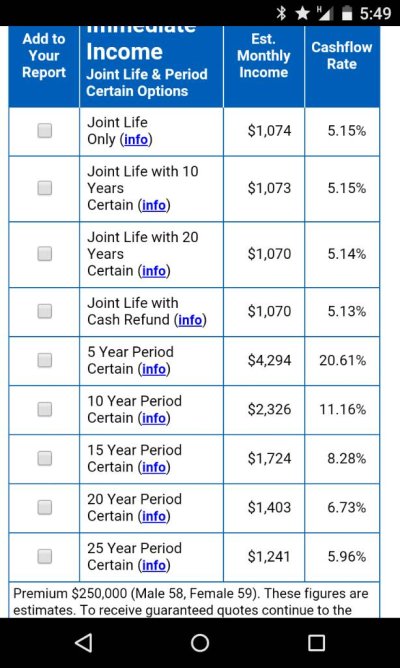

Critical look at annuities is explored by Edelman. I see many points that I agree with him on.

http://www.fa-mag.com/news/7-reasons-i-m-not-fond--of-annuities-24007.html?section=47When clients invest in a globally diversified portfolio consisting of low-cost ETFs and index funds, they maintain control over their money. They

can make investment changes anytime, and they can withdraw their money whenever they want. But when they put money into an annuity, they face higher costs and often severe restrictions, sometimes permanent ones.

No wonder the SEC, Finra and NASAA have issued so many investor alerts regarding the sales practices of annuity products.