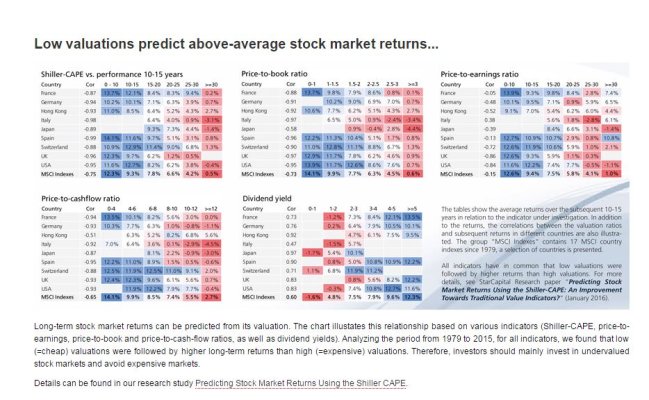

An interesting blog post by Meb Faber on CAPE ratios, cleverly titled "Don't Use the CAPE Ratio". What makes this article different is two things: the focus on other countries, and some good links, including one to Star Capital, which provides detailed CAPE ratio data for other countries.

Don't Use the CAPE Ratio | Meb Faber Research - Stock Market and Investing Blog

Don't Use the CAPE Ratio | Meb Faber Research - Stock Market and Investing Blog