Curious, for those who have been tracking your budget for many years, do you see increased spend that tracks with inflation?

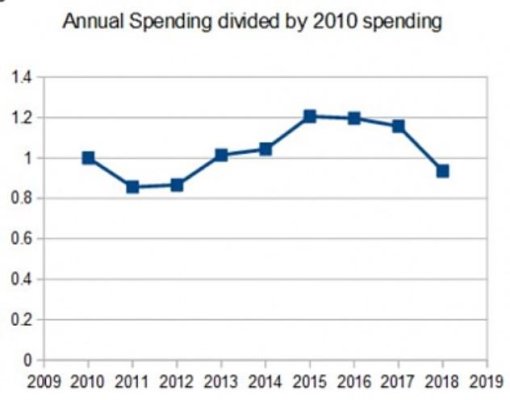

We’ve only been closely tracking for three years, but the majority of our expenses have not increased with inflation. We have a remarkably similar spend over the time period we’ve been tracking.

A big chunk of our spend is associated with our home (mortgage, property taxes and home services). Wondering if this is partly why we’re not seeing the increased.

We’ve only been closely tracking for three years, but the majority of our expenses have not increased with inflation. We have a remarkably similar spend over the time period we’ve been tracking.

A big chunk of our spend is associated with our home (mortgage, property taxes and home services). Wondering if this is partly why we’re not seeing the increased.