Sorry if this has been covered; I tried searching but couldn't find the answer to my question.

I am now working through my 91 yo father's estate, and one task is transferring his 403(b) at TIAA-CREF to his widow (a spousal transfer to a traditional IRA, which is much better than an inherited IRA for an 86 yo widow).

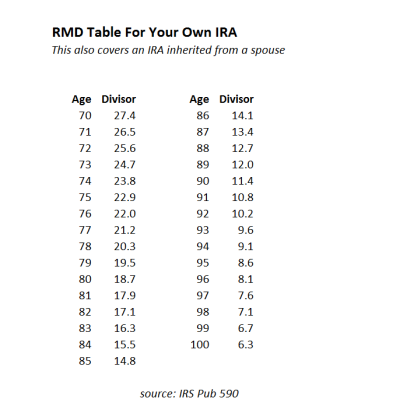

Anyway, as I was going through statements for the past three years, I noticed that his monthly RMD never changed: it was the same in 2012, 2013, 2014 and the first two months of 2015 (until we reported his death).

How often is the RMD supposed to be calculated, and the distribution amount adjusted? I've done a general online search, and for example, TRowePrice says the RMD is recalculated every year. That sure didn't happen.

If that is correct, then TIAA-CREF blew it. Now what do I do? Wait to see if the IRS notices? I gather the underpayment penalties are stiff.

I can't wait to get her funds out of TIAA-CREF and over to Vanguard, where the Keystone Cops aren't running the show!

I am now working through my 91 yo father's estate, and one task is transferring his 403(b) at TIAA-CREF to his widow (a spousal transfer to a traditional IRA, which is much better than an inherited IRA for an 86 yo widow).

Anyway, as I was going through statements for the past three years, I noticed that his monthly RMD never changed: it was the same in 2012, 2013, 2014 and the first two months of 2015 (until we reported his death).

How often is the RMD supposed to be calculated, and the distribution amount adjusted? I've done a general online search, and for example, TRowePrice says the RMD is recalculated every year. That sure didn't happen.

If that is correct, then TIAA-CREF blew it. Now what do I do? Wait to see if the IRS notices? I gather the underpayment penalties are stiff.

I can't wait to get her funds out of TIAA-CREF and over to Vanguard, where the Keystone Cops aren't running the show!