https://www.schwab.com/learn/story/fixed-income-outlook

They say most of the damage to Bonds may be behind us

They say most of the damage to Bonds may be behind us

I expect that it is. Bond index funds have been rallying since mid October.https://www.schwab.com/learn/story/fixed-income-outlook

They say most of the damage to Bonds may be behind us

I expect that it is. Bond index funds have been rallying since mid October.

I expect that it is. Bond index funds have been rallying since mid October.

No, I don’t own that fund. Some others have posted mentioning that fund.In prior posts I read you have had VBTLX.

Please expand on the reasons if you still have/sold the Bond Index, it may help me/others understand this Bonds loss of historic proportions

For us, we bought VBTLX in our working years & have held since with no changes, except converting & replacing with VTI in our Roth Accounts.

Thanks

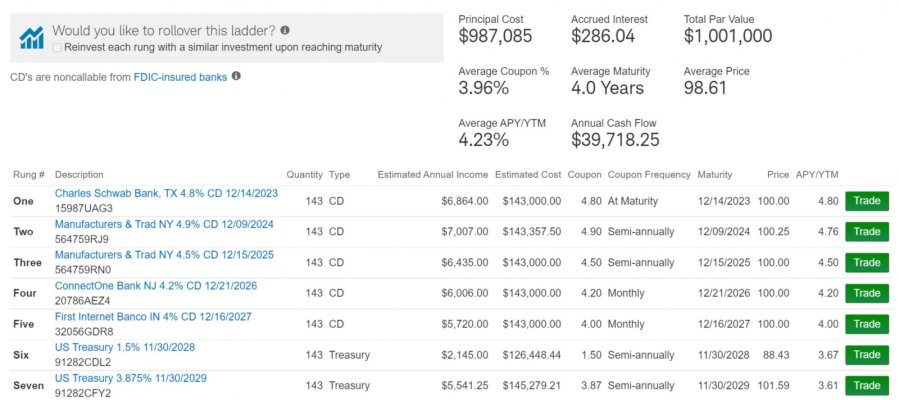

Different strokes……Like I said in a prior post, I'm skeptical that BND will outperform a 10-year CD/UST bond ladder over the next 10 years, and I prefer the control of a ladder. YMMV.

Is it not true that most of a Bond return is from the yield (dividend) it pays & not its price ?.

I'm in year 5 of an 8 year iShares ladder. It wasn't my best or worst decision.I've started to like what I am reading about bond ETFs like iShares iBonds and BulletShares that buy and hold bonds for target years to maturity. Seems a nice compromise between holding individual bonds to maturity with little risk on the downside (early call, default, etc.) and benefit of diversification and liquidity.

The December 2027 fund IBDS has an estimated yield of 2.75% but I see a 5 yr non callable CD from Medallion Bank yielding 3.9%.

The ticker is IBDS - iShare Dec 2027 Corporate fund.I'm not in the market to buy this fund, but was curious as to why the gap. It wasn't clear to me exactly which fund you referenced or the source of the "estimated yield". I looked at a couple of 2027 funds, but they beat the CD.

If you are willing to share ticker & yield source, I'd probably look into to satisfy my curiosity. Again, not so interested as to invest! Thanks

I've held Bullet shares in the past and they're ok. I've observed that the returns in the final year tend to be low because maturities occur fairly evenly over the year and are invested short term until the terminal distribution is made in December.I've started to like what I am reading about bond ETFs like iShares iBonds and BulletShares that buy and hold bonds for target years to maturity. Seems a nice compromise between holding individual bonds to maturity with little risk on the downside (early call, default, etc.) and benefit of diversification and liquidity.

My guess is that from what I've observed recently, high quality corporate bonds are yielding less than CDs or US treasuries for the 5-year. For example, right now on Schwab a 5-year CD is showing is 4.6% and a 4-year double a bond is 4.26%. That's likely part of it anyway.The ticker is IBDS - iShare Dec 2027 Corporate fund.

Estimated yield was from Fidelity.

The ticker is IBDS - iShare Dec 2027 Corporate fund.

Estimated yield was from Fidelity.

Heck, even if the proceeds from the sale of BND sits in a money market fund until rsker figures out what to do with it it will be better than staying with BND. My money market fund, SWVXX is yielding 3.8%.

I sold some BND & am buying SWVXX,

Yes small steps......... THANK YOU !!!!

All I saw on the Black rock site was the 30 day SEC yeild data.Thanks for the reply. I know some of these funds have quirks & thought I might learn something. I hadn't looked on Fidelity, but had gone to Blackrock site (provider of the etf) & it shows 5%. I would expect Fidelity just had stale data rather than flawed method. In any event, I wouldn't suggest you change your approach back to using this...I just wondered

That -13% loss occurred because rates were at near 0% before and now as you know even money markets are at 3.8%. In order to fully reverse your BND NAV loss, rates would have to go back down to near 0% again. While rates are down from the peak now with inflation finally slowing, which let the bond funds NAV recover a bit, near 0% rates, while possible, seem unlikely for the foreseeable future with The Fed still keeping a close eye on inflation.

If there is larger stock sell off and/or if a recession occurs there likely will be.We have about 30% of our AA in BND and we are staying put. What if there is a global flight to safety in 2023?

We have about 30% of our AA in BND and we are staying put. What if there is a global flight to safety in 2023?

The 13% loss is YTD isn't it? I'd think rkser should be more interested in the loss vs. his cost. Perhaps his average buy was earlier and his breakeven bar is set a bit lower.

Flights to safety usually means assets like cash or short term Treasuries, which have less credit risk than corporate bonds and less market risk than bond funds without maturity dates.

Related links:

"Bonds are less risky than bond funds. You can choose to hold your bond until it matures, receive interest, and receive your full principal back, as long as the issuing entity does not default. Bond funds carry greater market risk than bonds, which means they carry more interest rate risk, because they are fully exposed to the possibility of falling prices within their holdings. Equal and opposite, you can enjoy rising prices with a bond fund. With a bond, you won't receive an increase in value unless you sell your bond in the open market before it matures for a higher price than you paid for it." - https://www.thebalancemoney.com/what-is-the-difference-between-bonds-and-bond-funds-2466581

Understanding Flight to Quality - "For example, during a bear market, investors will often move their money out of equities and into government securities and money market funds." - https://www.investopedia.com/terms/f/flighttoquality.asp