gooddog

Recycles dryer sheets

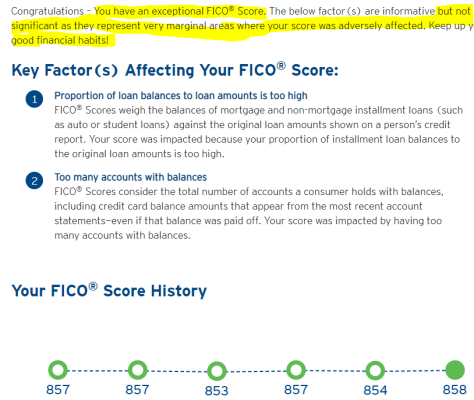

Run a HELOC against your house to show a 'mortgage'. At least my bank reports it as a mortgage to the credit companies. I borrowed the minimum allowed when opening it, paid it off over 6 months so it would count for credit purposes. Worked like a charm, and got a free appraisal out of it too. A note, when borrowing the minimum against the HELOC (say 5k), pay off 4.9k two days later, then make small payments for the next 6 months so you have almost no interest expense.