With a portfolio of 1,650,000 my input in FIREcalc was a retirement date some time before end of 2020 year - I will be 60. 42 year duration.

I need 75k in expenses figuring 87k before 13% total tax bill. One time lump sum withdrawal in 2021 of roughly 75k to payoff small mortgage balance. Secondary plan would be to split that lump sum withdrawal over 2 years 2021/22 to perhaps stem tax bite.

Taking SS me @70 43k/yr DW 21k/yr @62 figuring ( spousal support) half of what I am getting.

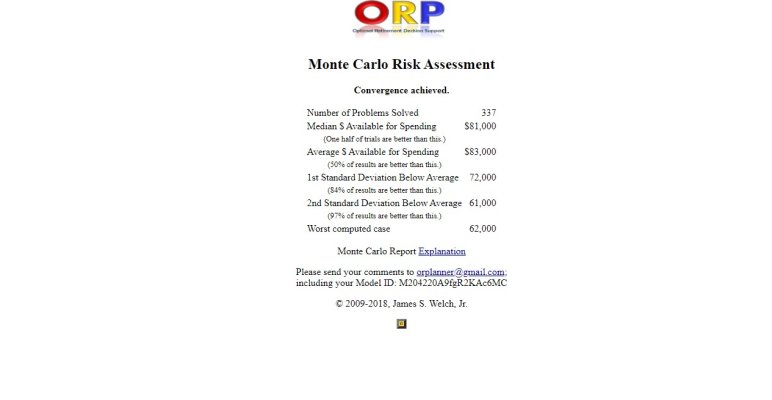

Results were 100%.

Seem right? Just a 2nd or extra 100 set of eyes

Thanks in advance.

I need 75k in expenses figuring 87k before 13% total tax bill. One time lump sum withdrawal in 2021 of roughly 75k to payoff small mortgage balance. Secondary plan would be to split that lump sum withdrawal over 2 years 2021/22 to perhaps stem tax bite.

Taking SS me @70 43k/yr DW 21k/yr @62 figuring ( spousal support) half of what I am getting.

Results were 100%.

Seem right? Just a 2nd or extra 100 set of eyes

Thanks in advance.