I finally found an inflation linked bond ETF in EUR, and likely will put both myself and DM in it shortly. It's all government (eurozone) issued, so similar to the US TIPS, but for us lowly Europeans. Expense ratio 0.25%. For the curious: IBCI is the ticker.

Before I pull that trigger, any experiences and/or insights to be had?

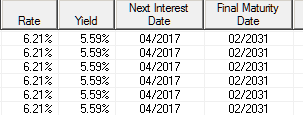

The average effective duration of the ETF is 8 years, but I figure if I hold them effectively infinity years (20+) the yield we'll get is the current YTM + inflation.

So if inflation goes up, no issue. And if interest rates go up initially the ETF would go down but catch up after a while since interest rates are higher.

Would especially be interested in what the inflation part of the TIPS has done the last few years in the US, any surprises (positive or negative)? Not looking for systemic (eurozone implosion) risks, we know about that")

Before I pull that trigger, any experiences and/or insights to be had?

The average effective duration of the ETF is 8 years, but I figure if I hold them effectively infinity years (20+) the yield we'll get is the current YTM + inflation.

So if inflation goes up, no issue. And if interest rates go up initially the ETF would go down but catch up after a while since interest rates are higher.

Would especially be interested in what the inflation part of the TIPS has done the last few years in the US, any surprises (positive or negative)? Not looking for systemic (eurozone implosion) risks, we know about that