Backpacker

Recycles dryer sheets

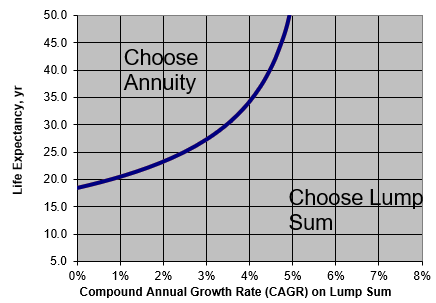

I am considering taking a lump sum from an old pension that has been sitting for 20+ years. At age 60 the lump sum offer is $55k, if I take the monthly pension at age 60, monthly amount is 248 a month. SPIA at immediatannuity.com says premium of $55k = 255 a month. So it appears that the $55k is a fair lump sum offer. (I'll be 58 this year so would need to make sure SPIA vs. lump is comparable.)

If I invest the $55k at 7% return and take monthly draws of $250; I would still have $143k left at age 90. I don't really think we'd need to take a draw off the investment at this point, so if it just sits and compounds until age 90 FV = $ 448k

My wife already has a pension that is meeting almost all our current expenses, it is 100% survivor and has a COLA feature.

I like the idea of some fixed income and some income from investment, and think that with DW pension (and SS at some point) we're fine. Feeling like I could take the market risk on the $55k and do as well or better than monthly pension.

Anyone care to review and question anything I have missed or let me know if I am off base?

If I invest the $55k at 7% return and take monthly draws of $250; I would still have $143k left at age 90. I don't really think we'd need to take a draw off the investment at this point, so if it just sits and compounds until age 90 FV = $ 448k

My wife already has a pension that is meeting almost all our current expenses, it is 100% survivor and has a COLA feature.

I like the idea of some fixed income and some income from investment, and think that with DW pension (and SS at some point) we're fine. Feeling like I could take the market risk on the $55k and do as well or better than monthly pension.

Anyone care to review and question anything I have missed or let me know if I am off base?