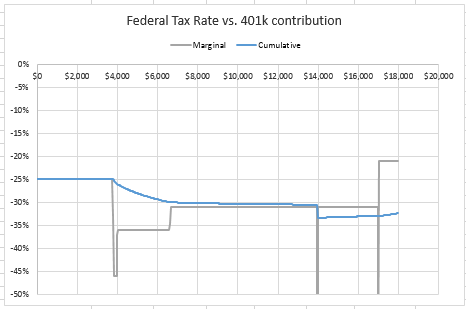

Op again, glad to see that this thread is gathering a lot of interest, hopefully many will read it and start their retirement planning early.

If you are way “over the hump” it makes no difference, but if you are going to be close to the hump, on either side, then early planning for retirement can be very helpful. A “very close friend” who happens to be a widow, is in this situation, has been doing Roth Conversions for the last 4 years at her 25% tax level. She will retire on survivor benefits at age 62, but will not start her annuity at that time. With just her age 62 Social Security plus her late husband’s small pension she will be in the 0% tax bracket. We can use her ages 62 to 70 to do as many Roth Conversions as she can at the 0%, 10%, 15% and 18.5% marginal brackets while her annuity payment grows by 9% per year. Then at age 69 or 70 she can start her annuity at a level that will place her just below the 46.25% bracket when she starts her own max SS at age 70. By that point all of her retirement savings will have been converted from TIRA to Roth so she will never go into The Hump.

There will be no MRD’s to be taxed at 46.25% since everything was converted at 18.5% and lower. She will have everything in Roth and can take it out tax free.

If you start in your mid 50’s, or earlier, to calculate what your personal retirement situation will be, you might be able to take steps to maximize your lifelong retirement income, but this takes early planning.

I’ve talked to my broker and it is amazing how many people, at any income and savings levels, call him at age 60 and say they want to retire in 2 years, or less, and ask what they can do. You need to start planning at least 5 to 10 years before retirement.