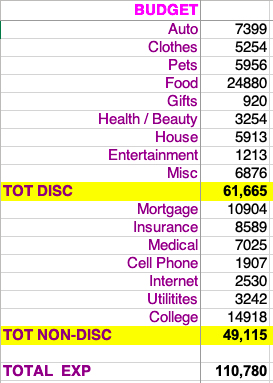

We spent $88,000 plus in 2020 being split about 50:50 between basic living expenses and discretionary spending. Still, we spent about $15,000 less in 2020 than 2019. In 2019 we had the moving expenses and related home improvement costs for our new home in Florida.

We are fortunate that we have been retired nearly 7 years, moved twice, and have not yet needed to tap into any IRA or 401K investments. Retired life has been good so far.

2021 should be a bit less expensive. Only planned major expense is to air condition the garage. We are hoping to spend under $85,000 in 2021.

Category|2020 Spend|Notes

Groceries|5,215.73|includes food, toiletries, cleaning products

Gasoline|606.35|lower than normal due to Covid

Utilities & HOA Fees|5,767.67|includes elec. cable & internet

Yard Maintenance|1,370.00|Includes mowing, bush trimming, fertilizing, etc

Medical/Dental|7,622.07|includes prescriptions, Medicare monthly fees, etc.

Clothes|1,769.23|

Miscellanous|4,975.19|mostly one time expenses that are un-catagorized

Insurance|2,458.00|house, cars, golf cart

Gifts|3,052.27|birthdays, Christmas, etc.

Property Tax|6,252.13|includes some bond interest fees

Car Repairs|1,129.69|

Home Repairs|3,064.90|

Total Basic Living Expenses|43,483.23|

Travel & Entertainment|8,597.80|Incledes eating out, and vacations

Home Improvements|19,752|New flooring, new crown moldings, etc.

Bond Payoff|16,564.77|Future property tax bill will be lowered as result

Total Discretionary Expenses|44,914.57

Total 2020 Spending|88,397.80